Innes Park is a relaxed coastal suburb sitting just south of Bundaberg in Queensland's Wide Bay region. It's a popular spot for families and sea-changers alike, with a mix of newer builds and established homes close to the beach. This article takes a close look at a real home and contents insurance quote for a four-bedroom, free-standing home in Innes Park (QLD 4670) — breaking down whether the price stacks up, how local conditions shape premiums, and what homeowners here can do to keep costs in check.

---

Is This Quote Fair?

The quote in question comes in at $2,164 per year (or about $212/month) for combined home and contents cover, with a building sum insured of $670,000 and contents valued at $65,000. Both the building and contents excess sit at $1,000.

Our price rating for this quote is FAIR — Around Average.

That assessment holds up well when you dig into the numbers. The suburb average premium for Innes Park is $3,124 per year, and the median sits at $2,726. This quote falls comfortably below both figures, landing closer to the 25th percentile of $2,104 — meaning it's cheaper than roughly 75% of quotes we've seen for this area. That's a solid result.

It's worth noting that "fair" doesn't mean you can't do better — it simply means the price is broadly in line with what's reasonable for the property type, location, and level of cover. Given the above-average fittings quality and a handful of features that typically push premiums up (more on those shortly), landing near the lower quartile is genuinely encouraging.

---

How Innes Park Compares

To put this quote in proper context, here's how Innes Park sits relative to broader benchmarks:

| Benchmark | Annual Premium |

|---|---|

| This Quote | $2,164 |

| Innes Park 25th Percentile | $2,104 |

| Innes Park Median | $2,726 |

| Innes Park Average | $3,124 |

| Innes Park 75th Percentile | $3,448 |

| QLD State Median | $3,903 |

| QLD State Average | $9,129 |

| National Median | $2,764 |

| National Average | $5,347 |

(Based on 77 quotes sampled for the Innes Park area.)

A few things stand out here. First, the Queensland state average of $9,129 is eye-wateringly high compared to both the national average and local Innes Park figures. This is largely a reflection of Queensland's exposure to extreme weather events — cyclones, floods, and storms — which drive up premiums significantly in higher-risk postcodes across the state. Innes Park, while coastal, is not classified as a cyclone risk area, which is a meaningful factor keeping local premiums more competitive.

Second, the national average of $5,347 is also well above what's being quoted here, again illustrating that Innes Park sits in a relatively favourable position compared to many parts of the country. The national median of $2,764 is the more useful comparison for a typical property — and this quote still comes in beneath it.

---

Property Features That Affect Your Premium

Every property has its own risk profile, and insurers price accordingly. Here's how the key features of this particular home influence what you'd expect to pay:

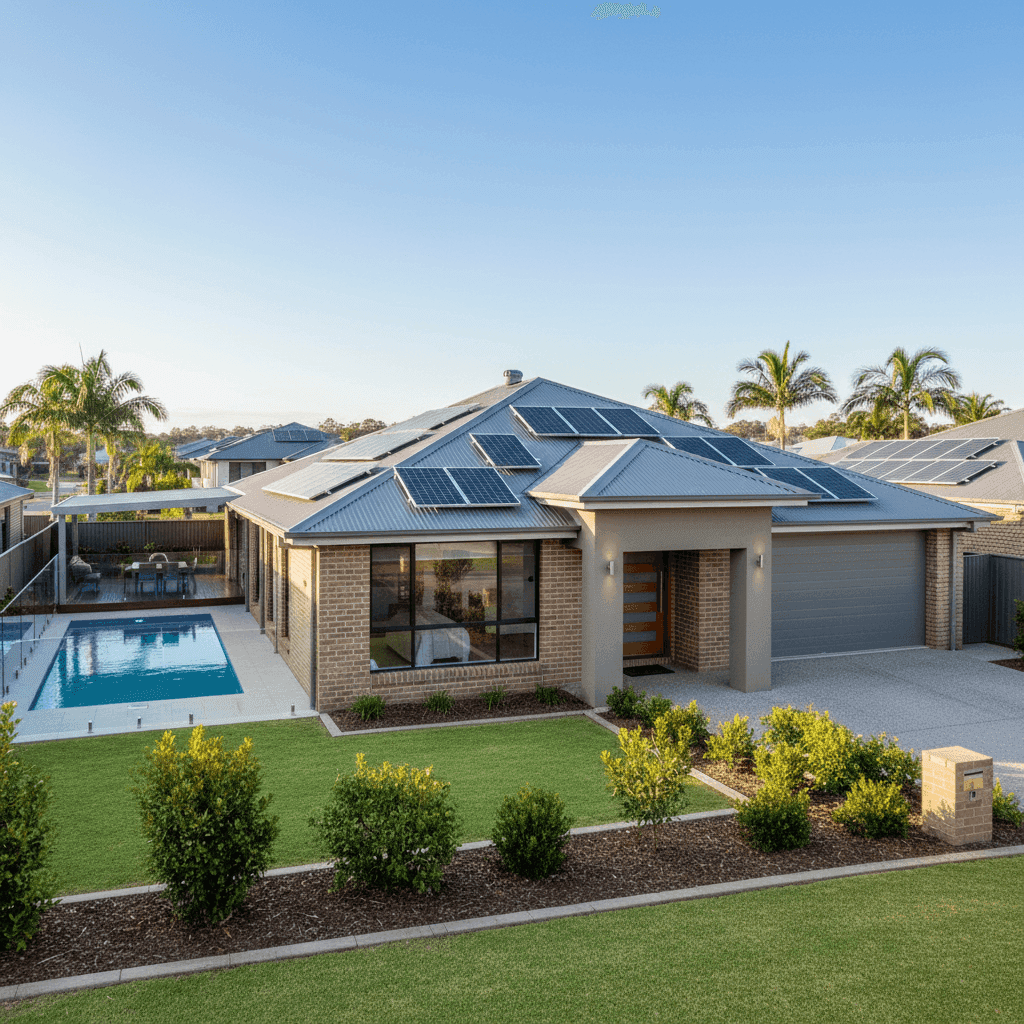

Brick Veneer Walls & Colorbond Roof Brick veneer is well-regarded by insurers for its durability and fire resistance. Combined with a steel Colorbond roof — one of the most resilient roofing materials available in Australia — this home presents a lower risk of structural damage from storms and fire than older or timber-framed alternatives. Both features work in the homeowner's favour at premium time.

New Build (2022) A home constructed in 2022 benefits from modern building codes, which in Queensland have been progressively strengthened to improve resilience against weather events. Newer homes typically attract lower premiums than older stock, as there's less likelihood of ageing infrastructure, outdated wiring, or deteriorating materials causing a claim.

Slab Foundation & Vinyl Flooring A concrete slab foundation is the standard for modern Queensland homes and is generally viewed positively by insurers. Vinyl flooring is practical, durable, and relatively inexpensive to replace — which can help keep contents and building replacement costs manageable.

Swimming Pool Pools add value to a property but also introduce liability considerations. Most home insurance policies include public liability cover, which is particularly relevant when a pool is present. It's worth checking your policy's liability limits and any specific conditions around pool fencing compliance.

Solar Panels Solar panels are now a standard feature on many Queensland homes, but they do add to the overall insured value of the building. They can also be a target for storm or hail damage. Ensure your building sum insured accounts for the replacement cost of your solar system — underinsurance is a common issue here.

Ducted Climate Control Ducted air conditioning is a significant fixed asset and forms part of the building's insured value. Like solar, it's important to factor this into your sum insured calculation to avoid being caught short at claim time.

Above-Average Fittings Quality Higher-quality fixtures and fittings — think stone benchtops, premium appliances, and quality cabinetry — increase the cost to rebuild or repair. This is reflected in the $670,000 building sum insured, which is appropriate for a 214 sqm home of this standard.

---

Tips for Homeowners in Innes Park

1. Review Your Sum Insured Annually Building costs in Queensland have risen sharply in recent years. A sum insured that was adequate when you first took out your policy may no longer cover a full rebuild — especially with above-average fittings and extras like solar and ducted air conditioning. Use a building cost calculator each year to sense-check your figure.

2. Check Your Pool Compliance Queensland has strict pool fencing laws, and non-compliance can affect your ability to make a liability claim. Ensure your pool barrier meets current Queensland Development Code requirements and keep documentation handy.

3. Don't Overlook Contents Cover At $65,000, the contents value here is modest for a four-bedroom home with above-average fittings. Do a room-by-room inventory to make sure your electronics, furniture, clothing, and valuables are adequately covered. It's easy to underestimate — especially when you factor in outdoor furniture, tools, and sporting equipment.

4. Compare Before You Renew Loyalty doesn't always pay in the insurance market. Premiums can shift significantly between insurers for the same property. Using a comparison platform like CoverClub before your renewal date takes only a few minutes and could save you hundreds of dollars a year.

---

Ready to See What You Could Pay?

Whether you're a first-time buyer in Innes Park or reviewing your existing cover, it pays to know where your premium sits relative to the market. CoverClub makes it easy to compare home and contents insurance quotes tailored to your property — so you can make a confident, informed decision. Get a quote today and see how your premium stacks up.