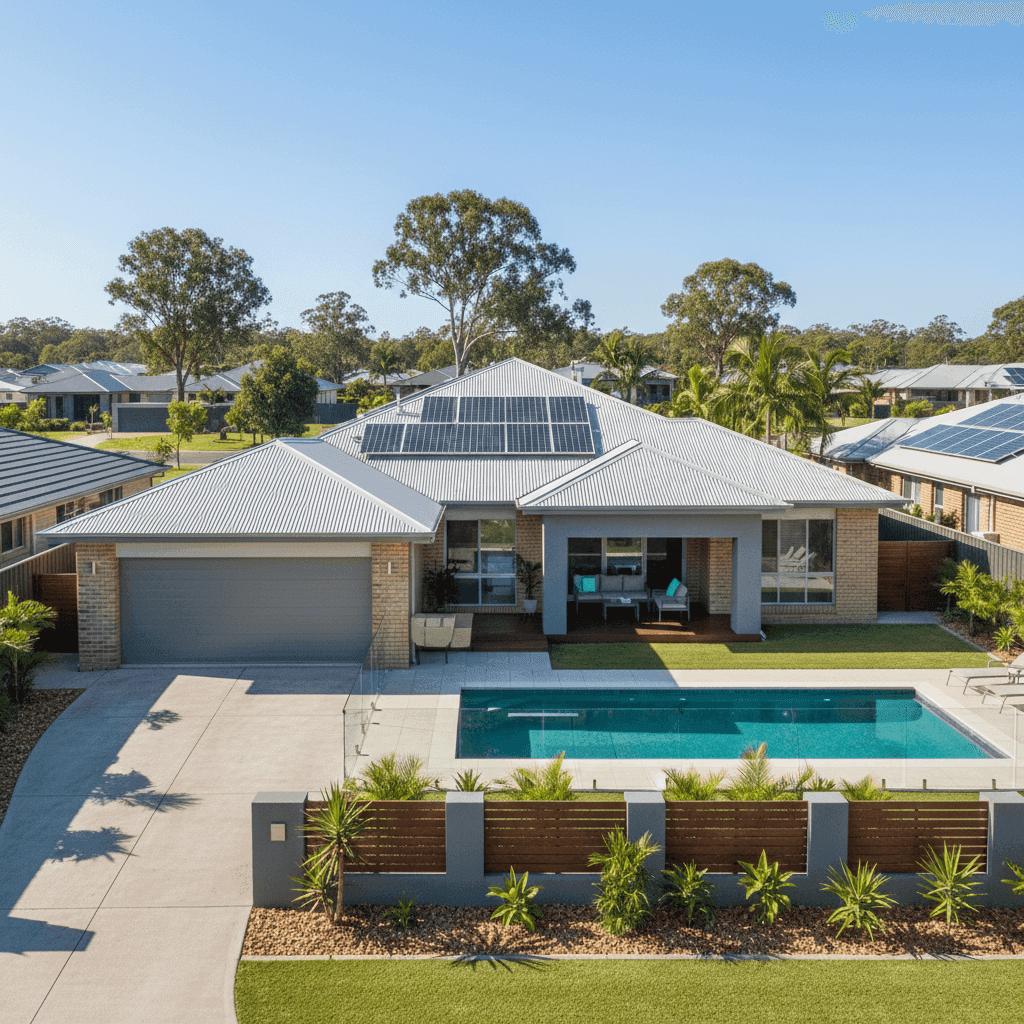

If you own a free standing home in Innes Park, QLD 4670, you're probably curious about what you should expect to pay for home and contents insurance — and whether the quotes you're seeing are reasonable. This analysis breaks down a real insurance quote for a four-bedroom, two-bathroom brick veneer home in Innes Park, built in 2022, and places it in context against local, state, and national benchmarks. Whether you're a new homeowner or reviewing your existing cover, read on to see how the numbers stack up.

---

Is This Quote Fair?

The quote in question comes in at $1,310 per year (or roughly $127/month) for combined home and contents cover, with a building sum insured of $695,000 and contents valued at $64,000. The building excess is $3,000 and the contents excess is $1,000.

Our price rating for this quote? Cheap — below average. That's genuinely good news.

To put it plainly: this premium sits well below what most comparable homeowners in the area are paying. Based on a sample of 72 quotes collected for the Innes Park postcode, the suburb average sits at $3,235/yr and the median at $3,013/yr. Even at the 25th percentile — meaning 75% of quotes are more expensive — the figure is $2,027/yr. This quote at $1,310/yr comes in below that lower quartile, meaning it's among the most competitive prices seen in the area.

For a relatively new, well-constructed home with above-average fittings, a pool, and solar panels, landing a premium this low is a strong outcome. It's worth noting that the excess levels are on the higher side (particularly the $3,000 building excess), which does contribute to reducing the annual premium — a trade-off worth keeping in mind when comparing policies.

---

How Innes Park Compares

Understanding your quote in isolation only tells part of the story. Here's how Innes Park sits relative to broader benchmarks:

| Benchmark | Average Premium | Median Premium |

|---|---|---|

| Innes Park (4670) | $3,235/yr | $3,013/yr |

| Queensland | $4,547/yr | $3,931/yr |

| National | $2,965/yr | $2,716/yr |

A few things stand out here. First, Innes Park premiums are notably lower than the Queensland state average, which at $4,547/yr reflects the significant flood, storm, and cyclone exposure that drives up costs across much of regional Queensland. Second, Innes Park actually sits above the national average, which suggests that while the suburb isn't among the most expensive in the state, it does carry some elevated risk relative to the broader Australian market — likely due to its coastal proximity and Queensland's general weather volatility.

For a deeper look at how this suburb's insurance costs trend over time, visit the Innes Park insurance stats page. You can also explore Queensland-wide insurance data or compare against national averages to get the full picture.

---

Property Features That Affect Your Premium

Several characteristics of this property work in favour of a lower premium, while a couple introduce additional considerations for insurers.

New construction (2022): A home built just a few years ago benefits enormously from modern building codes. Queensland has progressively tightened its standards around wind resistance, waterproofing, and structural integrity — particularly post-2011. A 2022 build is likely to comply with the latest requirements, reducing the probability of major structural claims.

Brick veneer walls and Colorbond roof: Brick veneer is well-regarded by insurers for its fire resistance and durability. Paired with a steel Colorbond roof — which is lightweight, corrosion-resistant, and performs well in high-wind conditions — this combination is generally viewed favourably during underwriting. Colorbond in particular is a popular choice in coastal Queensland for its resistance to salt air.

Slab foundation: Concrete slab foundations are considered lower risk than elevated or timber stumped foundations, particularly when it comes to flooding and pest damage. This is a positive factor for insurers.

Pool: A swimming pool adds to the replacement cost of the property and introduces some liability considerations, which can nudge premiums upward slightly. Ensuring your building sum insured accounts for the pool's value is important.

Solar panels: Rooftop solar is increasingly common and most modern policies accommodate it, but it's worth confirming your policy explicitly covers the panels — both for damage to them and any damage they might cause to the roof during a storm event.

Above-average fittings: Higher-quality fixtures and finishes increase the cost to rebuild or repair, and insurers factor this into their assessment. It's one reason why getting the sum insured right matters — underinsuring a well-appointed home can leave you significantly out of pocket after a major claim.

Vinyl flooring: A practical, durable choice that's relatively inexpensive to replace compared to hardwood or stone — a minor but positive factor from an insurer's perspective.

---

Tips for Homeowners in Innes Park

1. Review your building sum insured regularly Construction costs in Queensland have risen sharply in recent years. A home built in 2022 at 214 sqm with above-average fittings could cost significantly more to rebuild today than it did at completion. Use a building cost calculator or speak with a quantity surveyor to make sure your $695,000 sum insured still reflects current rebuild costs — not just the original build price.

2. Confirm your solar panels and pool are explicitly covered Not all policies treat solar panels and pools the same way. Check your Product Disclosure Statement (PDS) to confirm that both are included under your building cover, and that the pool's full replacement value is captured in your sum insured.

3. Understand the implications of your excess A $3,000 building excess is relatively high and will directly affect smaller claims. If a storm causes $2,500 worth of roof damage, you'd be covering that entirely out of pocket. Consider whether a lower excess (at a slightly higher premium) better suits your financial situation and risk appetite.

4. Shop around at renewal time Even with a competitive premium today, loyalty doesn't always pay in insurance. Insurers regularly adjust their pricing models, and the market can shift significantly year to year. Using a comparison platform like CoverClub at renewal time takes only a few minutes and could save you hundreds — especially given how wide the spread is in Innes Park, where quotes range from around $2,000 to over $3,800.

---

Compare Your Own Quote

Whether you're insuring for the first time or your renewal notice has just arrived, it pays to see what else is out there. CoverClub makes it easy to compare home and contents insurance quotes tailored to your property and location. Get a quote today and find out if you're getting the best deal available — just like the homeowner in this analysis did.