If you own a free standing home in Isabella Plains, ACT 2905, you're likely paying close attention to the cost of home and contents insurance — especially as premiums across Australia have been climbing in recent years. This article breaks down a real insurance quote for a five-bedroom brick veneer home in the suburb, benchmarks it against local, state, and national data, and offers practical tips to help you get the best value cover.

---

Is This Quote Fair?

The annual premium for this property came in at $1,730 per year (or roughly $166 per month), covering both building (sum insured: $736,000) and contents ($50,000), each with a $1,000 excess.

Our pricing engine rates this quote as FAIR — Around Average, which is a reasonable outcome for a well-established suburb in the ACT. To put that in context:

- The suburb average for Isabella Plains is $2,071/yr, and the median sits at $2,226/yr

- This quote lands below both figures, placing it in the lower half of the pricing range for the area

- The suburb's 25th percentile is $1,506/yr, meaning roughly 75% of comparable quotes are higher than this one

- The 75th percentile reaches $2,530/yr — so there's significant upside risk if you shop with the wrong insurer

In short, while this isn't the cheapest quote theoretically available in Isabella Plains, it's comfortably below average and represents solid value for the level of cover provided. The "Fair" rating reflects that there may be marginally cheaper options at the lower end of the market, but this quote is by no means overpriced.

---

How Isabella Plains Compares

Understanding where Isabella Plains sits within the broader insurance landscape helps put this quote in perspective. You can explore the full suburb breakdown on the Isabella Plains insurance stats page.

| Benchmark | Premium |

|---|---|

| This Quote | $1,730/yr |

| Isabella Plains Suburb Average | $2,071/yr |

| Isabella Plains Suburb Median | $2,226/yr |

| ACT State Average | $2,288/yr |

| ACT State Median | $2,186/yr |

| LGA (Unincorporated ACT) Average | $2,172/yr |

| National Average | $5,347/yr |

| National Median | $2,764/yr |

The ACT is one of the more affordable states for home insurance nationally, and Isabella Plains reflects that trend. The ACT state insurance stats show a state average of $2,288/yr — still well above this quote. When you zoom out to the national picture, the contrast is even more striking: the national average of $5,347/yr is more than three times this quote, largely driven by high-risk regions in Queensland and Western Australia facing cyclone, flood, and bushfire exposure.

For ACT homeowners, the absence of cyclone risk and the territory's relatively stable climate contribute to more moderate premiums. That said, bushfire risk in peri-urban Canberra and occasional hailstorms can still influence pricing, so it's worth ensuring your cover is genuinely adequate — not just cheap.

---

Property Features That Affect Your Premium

Several characteristics of this property play a meaningful role in how insurers price the risk:

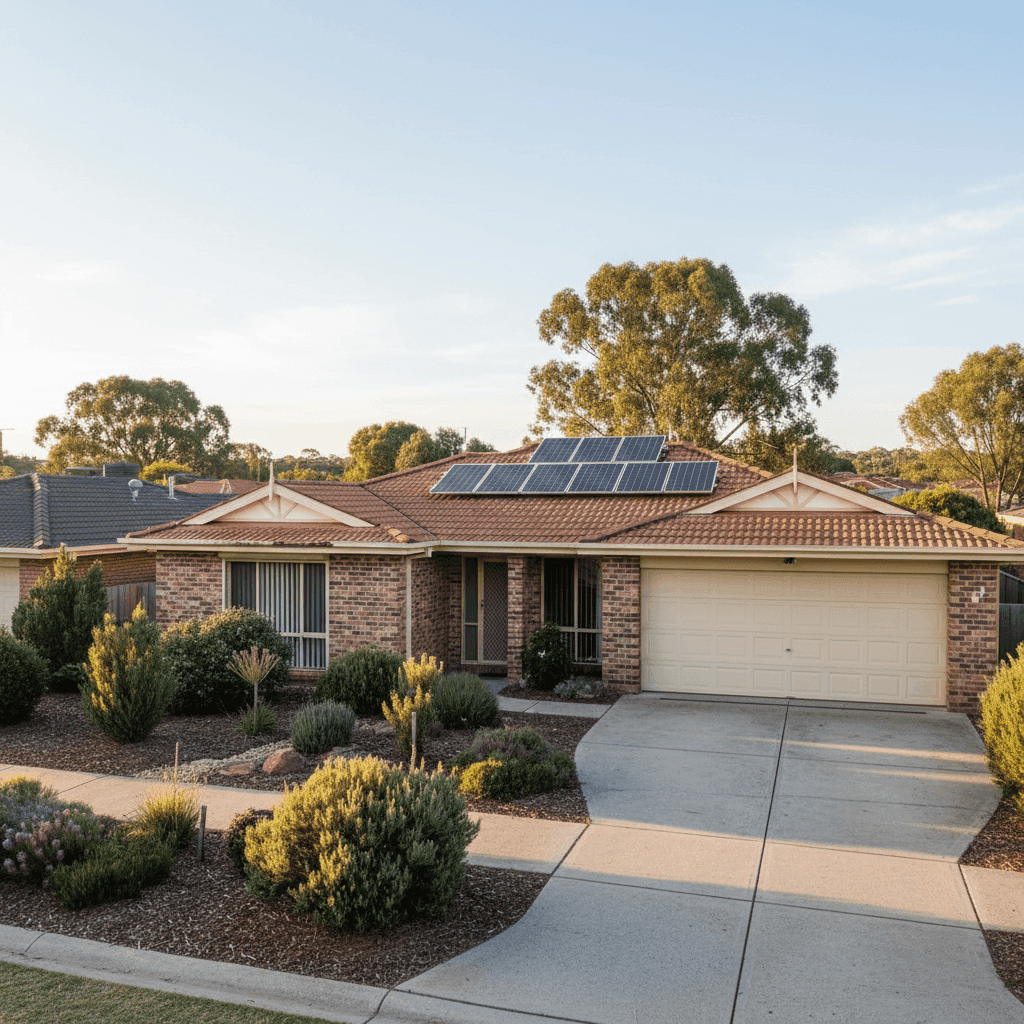

Brick Veneer Construction & Tiled Roof Brick veneer walls and a tiled roof are among the most insurer-friendly combinations in Australia. Both materials are considered durable, fire-resistant, and relatively inexpensive to repair compared to weatherboard or metal roofing alternatives. This likely contributes to keeping the premium on the lower end.

Slab Foundation & Tiled Flooring A concrete slab foundation is standard in the ACT and is generally viewed favourably by underwriters — there's no subfloor cavity to worry about, reducing the risk of certain types of damage. Tiled flooring throughout also signals lower susceptibility to water damage compared to timber or carpet-heavy homes.

Construction Year: 1985 At around 40 years old, this home sits in a middle ground for insurers. It's old enough that some building components (roofing, plumbing, electrical) may be approaching end-of-life, but it predates many modern construction standards. Keeping on top of maintenance is key to avoiding claim complications.

Solar Panels The presence of solar panels adds a modest layer of complexity for insurers. Panels need to be covered for damage (hail, storm, fire), and their replacement value should ideally be factored into your sum insured. It's worth confirming with your insurer that the solar system is explicitly included in your building cover.

Ducted Climate Control Ducted heating and cooling systems are a significant asset — and a significant liability if they fail or cause damage. Insurers factor in the replacement cost of these systems, which can run into the tens of thousands of dollars. Ensure your $736,000 sum insured adequately accounts for this.

No Pool The absence of a swimming pool removes one common source of liability and maintenance-related claims, which can modestly reduce your premium.

Property Size: 268 sqm At 268 square metres, this is a generously sized home. Building sum insured calculations should always be based on rebuild cost (not market value), and for a home of this size in the ACT, $736,000 appears to be a reasonable estimate — though it's worth periodically reviewing this figure against current construction costs, which have risen sharply in recent years.

---

Tips for Homeowners in Isabella Plains

1. Review Your Sum Insured Annually Construction costs in the ACT have increased considerably since the post-COVID building boom. If your sum insured hasn't been updated recently, you may be underinsured — meaning a total loss payout might not cover a full rebuild. Use a building cost calculator or speak to a quantity surveyor to sense-check your figure.

2. Confirm Solar Panel Coverage Ask your insurer directly: are the solar panels covered under the building policy, and up to what value? Some standard policies have sub-limits or exclusions for solar systems. If your system is worth $10,000–$20,000, you want that reflected in your cover.

3. Consider Raising Your Excess to Lower Your Premium With the current excess set at $1,000 for both building and contents, there may be room to increase this if you have sufficient savings to cover a higher out-of-pocket cost in the event of a claim. Some insurers will meaningfully reduce your annual premium in exchange for a higher excess — potentially saving you hundreds per year.

4. Shop the Market at Renewal Time Even a "Fair" rated quote can become uncompetitive over time as insurers adjust their pricing models. Make a habit of comparing quotes at least once a year, particularly as your home ages and your contents value changes. A few minutes of comparison shopping can easily save $300–$500 annually.

---

Compare Home Insurance Quotes in Isabella Plains

Whether you're reviewing your current policy or shopping for the first time, comparing multiple quotes is the single most effective way to ensure you're not overpaying. At CoverClub, we make it easy to benchmark your premium against real data from your suburb and state. Get a home insurance quote today and see how your current cover stacks up — you might be surprised at what's available.