If you own a free standing home in Jacobs Well, QLD 4208, you've probably wondered whether you're paying a fair price for home insurance — or whether there's a better deal waiting to be found. Jacobs Well is a quiet coastal community on the southern Gold Coast, known for its waterways, relaxed lifestyle, and proximity to Moreton Bay. It's a desirable place to live, but like many Queensland coastal suburbs, it comes with its own insurance considerations. This article breaks down a real home and contents insurance quote for a four-bedroom property in the area, and puts it in context against local, state, and national benchmarks.

---

Is This Quote Fair?

The quote in question comes in at $4,613 per year (or $453 per month) for a combined home and contents policy. The building is insured for $1,047,000 and contents for $199,000, with a building excess of $3,000 and a contents excess of $600.

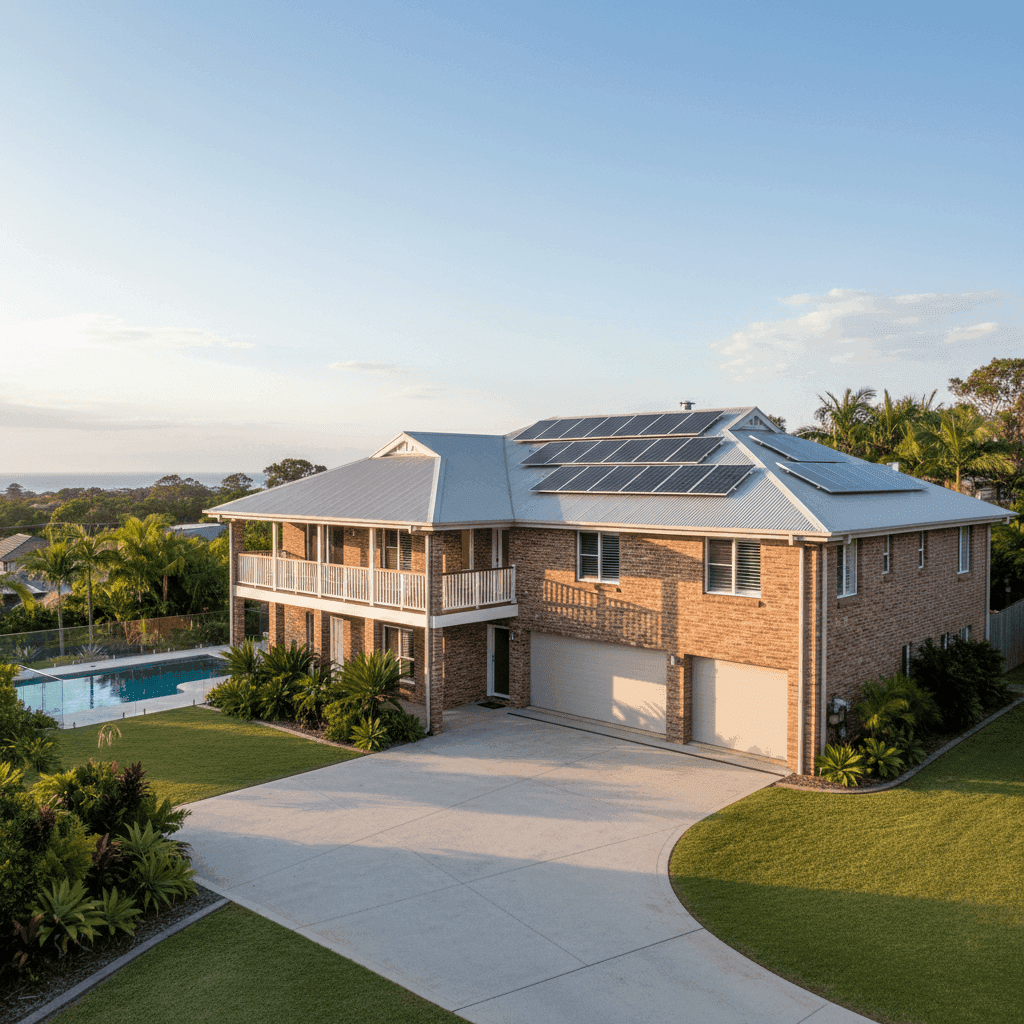

Our price rating for this quote is FAIR — Around Average. That means it's neither a standout bargain nor an obvious overpay. Given the size and value of the property — a 268 sqm, four-bedroom, four-bathroom home built in 2018 — a premium in this range is broadly reasonable.

It's worth noting that the building excess is set at $3,000, which is on the higher end. Opting for a higher excess is a common way to bring premiums down, so if this quote was structured with a lower excess, the annual cost could be noticeably higher. Homeowners should weigh up whether that $3,000 out-of-pocket threshold feels comfortable in the event of a claim.

---

How Jacobs Well Compares

To understand whether $4,613 is truly competitive, it helps to look at what others in the area — and across the country — are paying.

According to data from CoverClub's Jacobs Well suburb stats, based on 82 quotes in the 4208 postcode:

| Benchmark | Annual Premium |

|---|---|

| Suburb average | $6,769 |

| Suburb median | $4,222 |

| Suburb 25th percentile | $2,707 |

| Suburb 75th percentile | $8,746 |

At $4,613, this quote sits just above the suburb median of $4,222 — meaning roughly half of comparable quotes in the area come in lower, and half come in higher. It's well below the suburb average of $6,769, which is skewed upward by some significantly higher-priced policies in the mix.

Zooming out to the state level, Queensland's average home insurance premium sits at $4,547 per year, with a median of $3,931. This quote is almost exactly in line with the QLD average — a reasonable result for a large, well-appointed home in a coastal Gold Coast suburb.

The national average tells a different story: Australians pay $2,965 per year on average, with a national median of $2,716. The gap between Jacobs Well and the national figures reflects the elevated risk profile of coastal Queensland properties, where flood, storm surge, and severe weather events are more prevalent than in many other parts of the country.

Within the Gold Coast LGA specifically, the average premium is $5,494 — so this quote is actually tracking below the broader local government area average, which is a positive sign.

---

Property Features That Affect Your Premium

Several characteristics of this property influence how insurers price the risk — both positively and negatively.

Elevated foundation (+): The home is elevated by at least one metre, which is a meaningful advantage in flood-prone coastal Queensland. Insurers generally view elevated homes more favourably because they're less susceptible to inundation from storm surge or localised flooding. This feature likely contributes to a more competitive premium than a slab-on-ground equivalent in the same area.

Construction quality (+): Brick veneer external walls and a steel/Colorbond roof are considered durable, low-maintenance materials by most insurers. Colorbond roofing in particular is well-regarded for its resistance to wind and fire, and is a common choice across coastal Queensland builds.

Newer build (+): Constructed in 2018, this is a relatively modern home. Newer properties tend to attract lower premiums because they meet current building codes, are less likely to have ageing infrastructure issues, and typically have better structural integrity.

Pool and solar panels (neutral to slight ↑): The presence of a swimming pool adds some liability exposure — pools are a factor in public liability claims — and may nudge the premium slightly upward. Solar panels on the roof can also add modest complexity to a claim (replacement costs, potential roof damage during installation or storms), though the impact on premiums is generally minor.

Timber/laminate flooring (↑): Timber and laminate floors can be more costly to repair or replace after water damage compared to tiles, which may be reflected in the contents and building sum insured calculations.

High sum insured: At $1,047,000 for the building and $199,000 for contents, this is a substantial total insured value. The building figure is appropriate for a 268 sqm home with quality finishes in coastal Queensland, where construction costs remain elevated. Underinsuring to save on premiums is a risk not worth taking — always ensure your sum insured reflects the true cost to rebuild.

---

Tips for Homeowners in Jacobs Well

1. Review your sum insured annually. Construction costs have risen sharply in recent years. The $1,047,000 building sum insured on this policy may be accurate today, but it's worth reassessing each year at renewal. Use a building cost calculator or speak with a local builder to get a realistic rebuild estimate — being underinsured at claim time can be financially devastating.

2. Consider your excess carefully. The $3,000 building excess on this policy is high. While it reduces the annual premium, it means you'll need to cover the first $3,000 of any building claim yourself. If a lower excess option is available, run the numbers to see whether the premium difference justifies the added out-of-pocket risk.

3. Ask about flood cover specifically. Jacobs Well's proximity to waterways and tidal areas means flood is a genuine consideration. Not all home insurance policies include flood cover as standard — some offer it as an optional add-on, and definitions vary between insurers. Make sure your policy explicitly covers flood (not just storm damage) and understand what triggers a flood event under your policy's terms.

4. Compare quotes at renewal — every year. The wide spread of premiums in the 4208 postcode (from $2,707 at the 25th percentile to $8,746 at the 75th) shows just how much prices can vary for similar properties. Loyalty doesn't always pay in insurance. Shopping around at each renewal is one of the simplest ways to avoid overpaying.

---

Ready to Compare?

Whether you're reviewing your existing policy or looking for cover for the first time, comparing quotes is the smartest first step. Get a home insurance quote at CoverClub and see how your premium stacks up against what others in Jacobs Well and across Queensland are paying. It only takes a few minutes, and the savings can be well worth it.