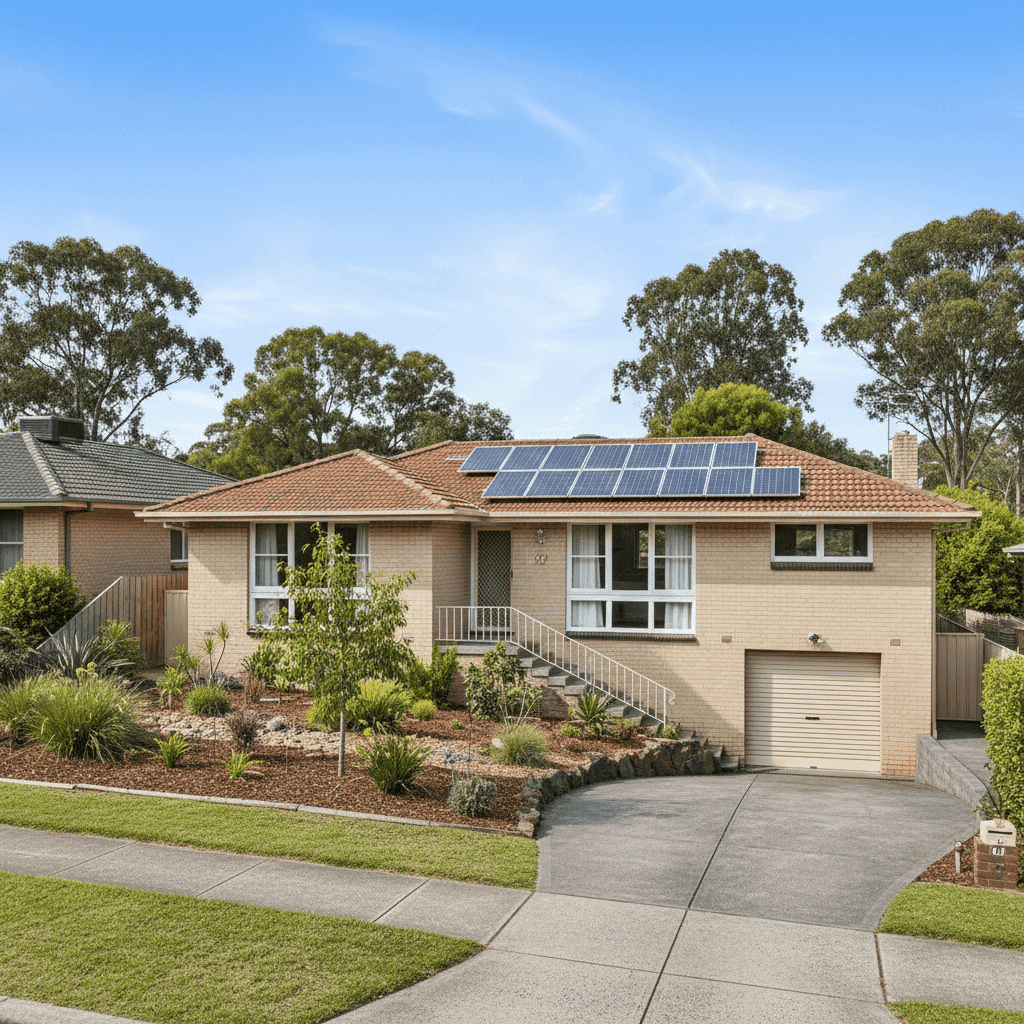

Jannali is a quiet, leafy suburb in Sydney's Sutherland Shire — known for its established streetscapes, generous block sizes, and a strong community feel. It's also home to plenty of solid, double-brick homes that have stood the test of time. If you own a free-standing home here and you're trying to make sense of your building insurance costs, this article breaks down a real quote for a 4-bedroom property in the area and puts it into context against local, state, and national benchmarks.

---

Is This Quote Fair?

The annual premium on this quote comes in at $2,059 per year (or $191/month) for building-only cover on a 4-bedroom, 2-bathroom free-standing home with a sum insured of $764,000 and a building excess of $4,000.

Our pricing engine has rated this quote as FAIR — Around Average. That's a reasonable outcome for a property of this type in Jannali, and here's why that rating makes sense when you look at the numbers.

The suburb average premium for Jannali (NSW 2226) sits at $1,723 per year, with a median of $1,302. At $2,059, this quote is above both the suburb average and median — but it's well within the upper half of the market. The 75th percentile for Jannali is $2,818, meaning roughly a quarter of quotes in the suburb come in higher than this one. So while you're not getting the cheapest deal on the street, you're also far from the most expensive.

It's worth noting that suburb-level data here is based on a sample of 13 quotes, so it's a useful guide rather than a definitive benchmark. As more data flows in, these figures will become increasingly precise.

---

How Jannali Compares

One of the most striking things about this quote is how it stacks up against broader benchmarks — and the picture is quite favourable for Jannali homeowners.

| Benchmark | Average | Median |

|---|---|---|

| Jannali (NSW 2226) | $1,723/yr | $1,302/yr |

| New South Wales | $9,528/yr | $3,770/yr |

| National | $5,347/yr | $2,764/yr |

The NSW state average of $9,528 per year is dramatically higher than what Jannali homeowners are typically paying — though that figure is heavily influenced by high-risk regional areas, flood-prone zones, and cyclone-affected regions in the north of the state. The national average of $5,347 tells a similar story.

Even comparing medians, Jannali's $1,302 sits comfortably below the national median of $2,764 and the NSW median of $3,770. This suggests that Jannali is, on balance, a relatively low-risk suburb from an insurance perspective — and that's reflected in the premiums locals are generally paying.

Interestingly, the LGA-level average for Sutherland Shire is recorded at $23,423 — an outlier figure that's almost certainly skewed by a small number of very high-value or high-risk properties in the dataset. It's not a meaningful benchmark for a standard residential property in Jannali.

---

Property Features That Affect Your Premium

Several characteristics of this property work in favour of a competitive premium, while a couple of others are worth understanding.

Double Brick Walls Double brick construction is one of the most desirable building types from an insurance standpoint. It offers excellent structural integrity, strong fire resistance, and good protection against storm damage. Insurers generally view double brick homes favourably, and it's likely contributing to a more competitive rate here.

Tiled Roof Terracotta or concrete tiles are a durable and widely accepted roofing material. They perform well in most weather conditions and are considered a lower-risk roofing type compared to, say, older corrugated iron or flat membrane roofs. This is another positive factor for this property.

Stump Foundation Homes built on stumps — particularly common in older Australian properties like this 1972 build — can be more susceptible to movement, subsidence, and pest damage over time. Insurers may factor this in when assessing risk, particularly if the stumps are original timber rather than restumped concrete or steel. It's worth ensuring your policy covers the foundation adequately.

Timber/Laminate Flooring Timber and laminate floors are attractive but can be costly to repair or replace following water damage or impact events. This is worth keeping in mind when reviewing your sum insured and policy inclusions.

Solar Panels This property has solar panels installed, which adds to the replacement value of the home. It's important to confirm that your solar system is explicitly included in your building sum insured — many homeowners overlook this, and underinsurance can be a real issue if panels are damaged in a storm or hail event.

Construction Year: 1972 At over 50 years old, this home may have original wiring, plumbing, or structural elements that could increase the cost of repairs. Some insurers apply age-related loadings for older homes, so it's worth shopping around to find a policy that assesses the property on its actual condition rather than just its age.

Sum Insured: $764,000 For a 214 sqm home in Jannali, this sum insured is substantial. Make sure this figure reflects the full cost to rebuild — including demolition, professional fees, and the current cost of materials and labour in the Sydney market, which has risen significantly in recent years.

---

Tips for Homeowners in Jannali

1. Review your sum insured annually Building costs in Sydney have increased considerably over the past few years. A sum insured that was accurate two or three years ago may now leave you underinsured. Use a building cost calculator or speak with a quantity surveyor to make sure your coverage keeps pace with current rebuild costs.

2. Confirm solar panels are covered If your solar system isn't explicitly listed in your policy schedule, ask your insurer to clarify. Some policies cover panels as part of the building; others may require a separate endorsement. Given the cost of a quality solar installation, this is not a detail to leave to chance.

3. Get the stumps inspected If your home still has its original 1972 timber stumps, it may be worth having them professionally inspected. Restumping can be a significant expense, and knowing the condition of your foundation not only protects your home but also ensures your insurer has accurate information about the property.

4. Compare quotes before renewing A "fair" rating means this quote is competitive — but it doesn't mean it's the best available. Premiums can vary significantly between insurers for the same property. Taking 15 minutes to compare quotes at renewal time could save you hundreds of dollars a year.

---

Compare Home Insurance Quotes in Jannali

Whether you're reviewing your current policy or shopping for cover on a new property, CoverClub makes it easy to compare building insurance quotes tailored to your home. See how your premium stacks up against others in Jannali and across NSW 2226, and get a personalised quote in minutes. Don't just accept your renewal — make sure you're getting the right cover at the right price.