If you own a free standing home in Jewells, NSW 2280, you're likely paying close attention to rising insurance costs — and for good reason. This article breaks down a real home and contents insurance quote for a four-bedroom, two-bathroom brick veneer property in the suburb, compares it against local, state, and national benchmarks, and offers practical advice for keeping your premium in check.

---

Is This Quote Fair?

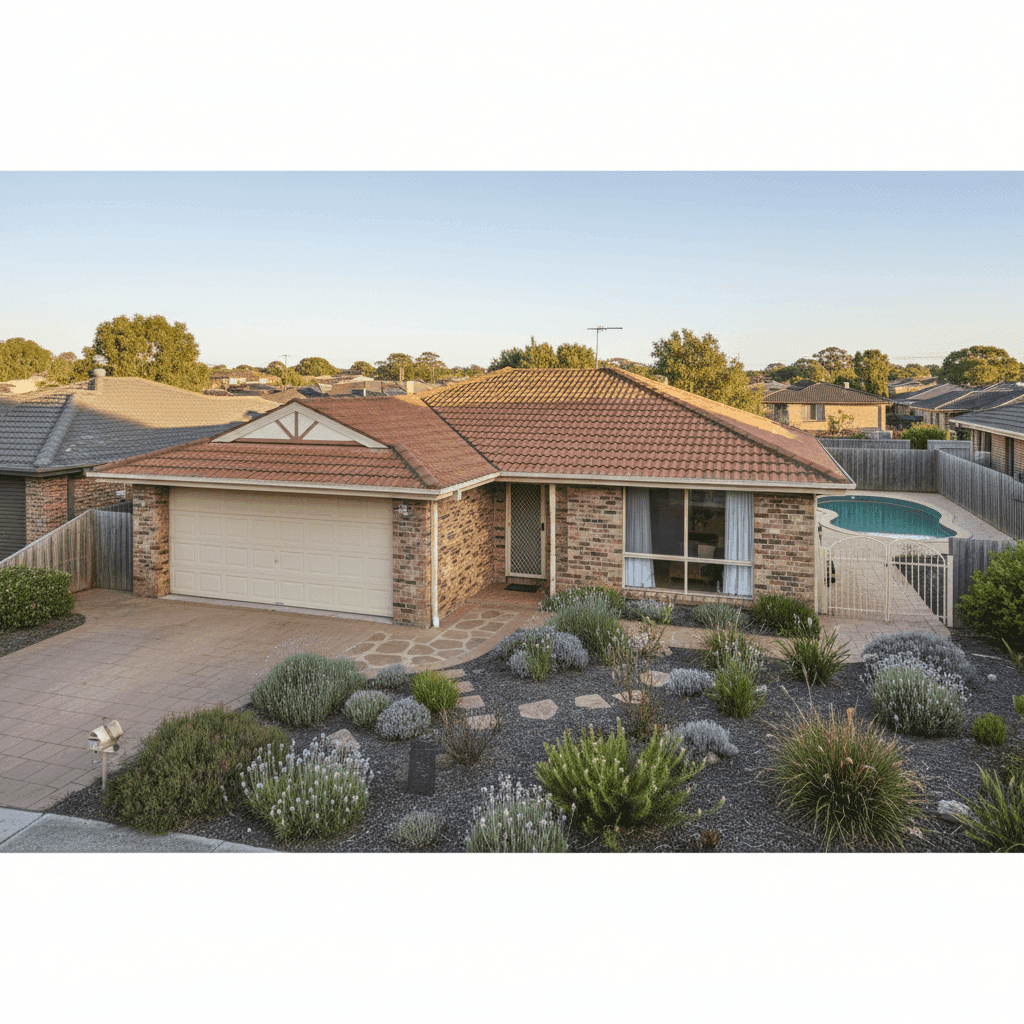

The quote in question comes in at $3,639 per year (or $349/month) for combined home and contents cover, with a building sum insured of $850,000 and contents valued at $95,000. Both the building and contents excess are set at $2,000.

Our price rating for this quote is Expensive — above average for the Jewells area.

To put that in context: the suburb average premium sits at $3,010/yr, and the median is even lower at $2,817/yr. This quote lands well above both figures, and also above the suburb's 75th percentile of $3,355/yr — meaning it's pricier than roughly three-quarters of comparable quotes we've seen in the postcode.

That said, "expensive" doesn't automatically mean "wrong." A higher building sum insured ($850,000 is on the upper end for this area), a swimming pool, and the age of the home all contribute legitimately to a higher premium. The key question is whether you're getting competitive value — and whether there's room to shop around.

---

How Jewells Compares

Understanding where Jewells sits in the broader insurance landscape is useful context for any homeowner. Here's a snapshot:

| Benchmark | Premium |

|---|---|

| This quote | $3,639/yr |

| Jewells suburb average | $3,010/yr |

| Jewells suburb median | $2,817/yr |

| NSW state average | $9,528/yr |

| NSW state median | $3,770/yr |

| National average | $5,347/yr |

| National median | $2,764/yr |

| Lake Macquarie LGA average | $11,064/yr |

Note: State and LGA averages are heavily skewed by high-risk properties (flood zones, bushfire-prone areas, coastal exposure), which is why medians are often a more useful comparison.

Relative to the NSW state median of $3,770/yr, this quote is actually slightly below — which is encouraging. And compared to the national average of $5,347/yr, Jewells homeowners are generally faring reasonably well.

The Lake Macquarie LGA average of $11,064/yr looks alarming at first glance, but this figure is pulled upward by higher-risk properties across the broader council area. Jewells itself sits at a more moderate risk profile, as reflected in the suburb-level data.

The bottom line: this quote is above average within Jewells, but not out of step with broader NSW and national trends — particularly given the property's features.

---

Property Features That Affect Your Premium

Several characteristics of this property have a direct bearing on what insurers charge. Here's how each one plays into the pricing:

Brick Veneer Walls & Tiled Roof

Brick veneer construction with a tiled roof is one of the more insurer-friendly combinations in Australia. Both materials are considered durable and fire-resistant, which generally attracts lower premiums compared to weatherboard cladding or metal roofing. This works in the homeowner's favour.

Stump Foundation

The property sits on stumps — a common foundation type for homes built in the Hunter region during the mid-20th century. While stumps can be associated with subsidence or pest risk over time, they're a well-understood construction type for insurers. Maintaining the stumps in good condition is important for both structural integrity and insurability.

Timber & Laminate Flooring

Timber and laminate floors are a factor insurers consider under contents and building cover. Timber flooring can be expensive to repair or replace after water damage or fire, which may nudge premiums slightly higher compared to homes with tile or concrete floors throughout.

Swimming Pool

A pool adds value to the property but also adds risk — and cost. Pools increase liability exposure and can contribute to water-related claims. Most insurers will factor a pool into the premium calculation, so it's worth confirming exactly what your policy covers in relation to pool equipment, fencing, and liability.

1980 Construction

Homes built around 1980 are now over 40 years old. Older properties can carry higher risk of electrical, plumbing, or structural issues, which insurers account for in their pricing. It's worth ensuring your building sum insured reflects current rebuild costs, not just the market value of the home.

Building Sum Insured: $850,000

This is a significant sum insured for a 139 sqm home. While it may seem high relative to the floor area, rebuild costs in Australia have risen sharply in recent years due to labour shortages and material price increases. Getting a quantity surveyor's assessment or using an online rebuild cost calculator can help confirm whether this figure is accurate — over-insuring inflates your premium unnecessarily, while under-insuring leaves you exposed.

---

Tips for Homeowners in Jewells

1. Review Your Building Sum Insured

As noted above, $850,000 for a 139 sqm home is worth scrutinising. Use a building replacement cost estimator to make sure you're not over-insured. Even a modest reduction in your sum insured — if justified — could meaningfully lower your annual premium.

2. Compare at Least Three Quotes

This quote is rated above average for Jewells. With the suburb median sitting at $2,817/yr, there's a reasonable chance a comparable level of cover is available at a lower price point. Get a fresh quote at CoverClub to see what other insurers are offering for your specific property.

3. Consider Your Excess Level

Both the building and contents excess are set at $2,000. Opting for a higher excess — say, $2,500 or $3,000 — can reduce your annual premium noticeably. Just make sure you're comfortable covering that amount out of pocket in the event of a claim.

4. Bundle and Ask About Discounts

Many insurers offer discounts when you combine home and contents cover (which this policy already does), but additional savings may be available for loyalty, security systems, or claim-free history. It's always worth calling your insurer directly to ask what discounts apply to your policy.

---

Ready to Find a Better Deal?

Whether you're renewing your existing policy or shopping for the first time, comparing quotes is the single most effective way to make sure you're not overpaying. At CoverClub, we make it easy to benchmark your premium against real data from your suburb and beyond. Start comparing home insurance quotes now and see how much you could save on your Jewells property.

For more suburb-specific data, visit the Jewells insurance stats page or explore NSW-wide home insurance trends.