Kamerunga is a quiet, leafy suburb on the northern fringe of Cairns — the kind of place where older character homes sit among tropical greenery, close to the Barron River and the rainforest edge. It's a beautiful part of Queensland to call home, but insuring a property here comes with its own set of considerations. This article breaks down a real building insurance quote for a four-bedroom, two-bathroom free-standing home in Kamerunga, and puts that number in context so you can make a more informed decision about your own cover.

---

Is This Quote Fair?

The quote in question comes in at $9,946 per year (or $953 per month) for building-only cover on a 244 sqm home insured for $1,234,000, with a $1,000 building excess. Our price rating for this quote is Fair — Around Average.

That "fair" rating doesn't mean you're getting a bargain, but it does mean you're not being gouged either. Given the complexity of this property — its age, construction type, elevated position, and location in a declared cyclone risk area — a premium sitting near the average mark is a reasonable outcome. Insurers price risk carefully in Far North Queensland, and this quote appears to reflect that without significant padding.

That said, "fair" is a relative term, and it's always worth shopping around. A few hundred dollars difference in annual premium adds up quickly over the life of a mortgage.

---

How Kamerunga Compares

To understand whether this quote is genuinely competitive, it helps to look at the broader picture. Here's how the $9,946 annual premium stacks up:

| Benchmark | Premium |

|---|---|

| This quote | $9,946/yr |

| LGA (Cairns) average | $12,404/yr |

| QLD state average | $9,129/yr |

| QLD state median | $3,903/yr |

| National average | $5,347/yr |

| National median | $2,764/yr |

A few things stand out immediately. First, this quote sits below the Cairns LGA average of $12,404 — that's a meaningful gap of over $2,400 per year, suggesting this particular quote is performing well relative to what many Cairns homeowners are paying. You can explore Cairns and QLD-wide insurance data on the CoverClub QLD stats page.

Second, the premium is noticeably higher than both the national average ($5,347) and the national median ($2,764). This isn't surprising — Far North Queensland is one of the most expensive regions in Australia for home insurance, driven primarily by cyclone exposure and the elevated risk of storm and flood damage. Comparing a Kamerunga quote to a Sydney or Melbourne benchmark isn't especially useful; the risk profiles are simply different. For a broader perspective, you can view national home insurance statistics here.

There is no suburb-level comparison data available for Kamerunga at this stage, but as more quotes flow through, suburb-specific stats will be published here.

---

Property Features That Affect Your Premium

Several characteristics of this home have a direct bearing on what insurers charge. Understanding them helps you see why the premium lands where it does.

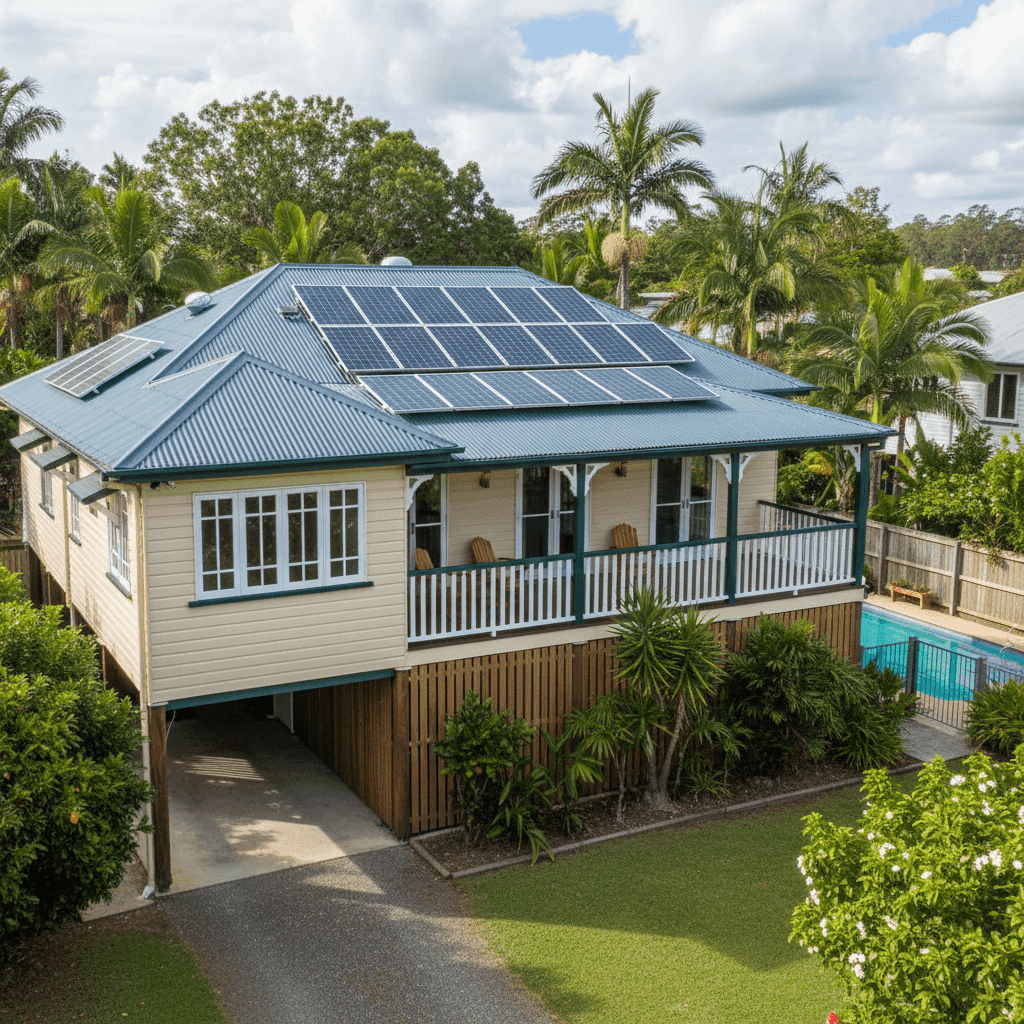

Age and construction (built 1953, weatherboard timber walls) Homes built in the 1950s carry additional risk in insurer eyes — older electrical wiring, ageing plumbing, and materials that may not meet modern building codes all contribute to higher claim likelihood. Weatherboard timber is also more susceptible to termite damage, moisture ingress, and fire spread than brick or concrete construction, which typically pushes premiums upward.

Roof type (steel/Colorbond) On the positive side, a Colorbond steel roof is generally well-regarded by insurers. It's durable, resistant to rot, and performs reasonably well in high-wind events compared to terracotta tiles. In a cyclone-prone region, this is a meaningful factor.

Foundation (stumps) and elevation (at least 1 metre) The home is built on stumps and elevated by at least one metre — classic Queenslander style. Elevation can actually work in your favour for flood risk, as water is less likely to enter the living areas during inundation events. However, elevated homes can be more exposed to wind uplift during severe storms, which insurers factor into their modelling.

Cyclone risk area This is arguably the single biggest driver of premiums in Kamerunga. Properties in declared cyclone risk zones attract a significant loading from most insurers. Cairns sits squarely in Tropical Cyclone territory, and the insurance industry has priced this risk accordingly — particularly following major weather events in recent years.

Additional features: pool, solar panels, ducted climate control Each of these adds to the replacement cost of the home and, by extension, the sum insured. A pool requires its own structural cover; solar panels (especially a full rooftop system) can be expensive to replace; and ducted climate control systems represent a significant capital item. With a sum insured of $1,234,000, these features are likely already captured — but it's worth confirming with your insurer that all are explicitly covered under the policy.

Above-average fittings The property is noted as having above-average fittings quality. This means kitchens, bathrooms, and fixtures are likely to be higher-spec than standard, which increases the cost to rebuild or repair — and justifies a higher sum insured.

---

Tips for Homeowners in Kamerunga

1. Review your sum insured annually Construction costs in Queensland have risen sharply over recent years. A sum insured that was accurate three years ago may now be insufficient to cover a full rebuild. Use a building cost calculator or ask a quantity surveyor to check your figure — being underinsured in a cyclone zone is a serious financial risk.

2. Ask about cyclone mitigation discounts Some insurers offer reduced premiums for homes that have undergone cyclone-proofing works — things like storm shutters, reinforced roof connections, or compliance with modern tie-down standards. Given the age of this home, there may be scope to invest in upgrades that pay back over time through lower premiums.

3. Compare quotes before renewal Loyalty doesn't always pay in insurance. The gap between the cheapest and most expensive quotes for a property like this can be thousands of dollars per year. Running a comparison through CoverClub takes only a few minutes and could surface a materially better deal.

4. Check what's excluded around storm and flood In Far North Queensland, the distinction between storm damage, flood damage, and cyclone damage matters enormously. Some policies define these events differently, and exclusions can catch homeowners off guard at claim time. Read the Product Disclosure Statement carefully — particularly the definitions section — before committing to a policy.

---

Ready to Compare?

Whether you're reviewing your current policy or shopping for the first time, comparing quotes is the smartest move you can make. Head to CoverClub to get building insurance quotes tailored to your Kamerunga property — it's free, fast, and could save you a significant amount each year.