Nestled in the heart of the Blue Mountains, Katoomba is one of the most scenic and sought-after addresses in New South Wales. But owning a free standing home here — particularly an older, character-filled property — comes with its own set of insurance considerations. This article breaks down a recent building insurance quote for a six-bedroom home in Katoomba (NSW 2780), examines how it stacks up against local, state, and national benchmarks, and offers practical guidance for homeowners in the area.

---

Is This Quote Fair?

The quote in question comes in at $1,987 per year (or $190 per month) for building-only cover, with a sum insured of $627,200 and a building excess of $5,000. Our analysis rates this as CHEAP — below the suburb average — which is genuinely good news for the homeowner.

To put that in context: the average home insurance premium across Katoomba sits at $2,381 per year, with a median of $2,520. This quote lands well below both figures, and even falls under the suburb's 25th percentile of $2,188 — meaning it's cheaper than at least 75% of comparable quotes gathered in the area. For a six-bedroom property with a relatively high sum insured, that's a strong result.

It's worth noting that a $5,000 building excess is on the higher side. Choosing a higher excess is a common way to reduce your annual premium, so part of the savings here may reflect that trade-off. If you ever need to make a claim, you'd be out of pocket for the first $5,000 — so it's important to make sure that's a figure you're comfortable with before locking in a policy.

---

How Katoomba Compares

Understanding where your premium sits relative to broader benchmarks can help you gauge whether you're getting a fair deal — or whether it's time to shop around.

| Benchmark | Annual Premium |

|---|---|

| This quote | $1,987 |

| Katoomba suburb average | $2,381 |

| Katoomba suburb median | $2,520 |

| Blue Mountains LGA average | $4,220 |

| NSW average | $9,528 |

| NSW median | $3,770 |

| National average | $5,347 |

| National median | $2,764 |

The numbers tell an interesting story. While this quote is comfortably below the Katoomba suburb average, it's also well under the NSW state average of $9,528 — though that figure is heavily skewed by high-risk and high-value properties across the state. Even against the national average of $5,347, this quote looks very competitive.

The Blue Mountains LGA average of $4,220 is particularly telling. Many properties in this region attract higher premiums due to bushfire exposure and the age of housing stock. The fact that this quote sits so far below that LGA average suggests the insurer has assessed this specific property favourably — likely influenced by its construction materials and other features.

> Note: The suburb sample size for Katoomba is 10 quotes, so these averages should be treated as indicative rather than definitive. More data points would give a sharper picture of the local market.

---

Property Features That Affect Your Premium

Several characteristics of this property are worth examining through an insurance lens:

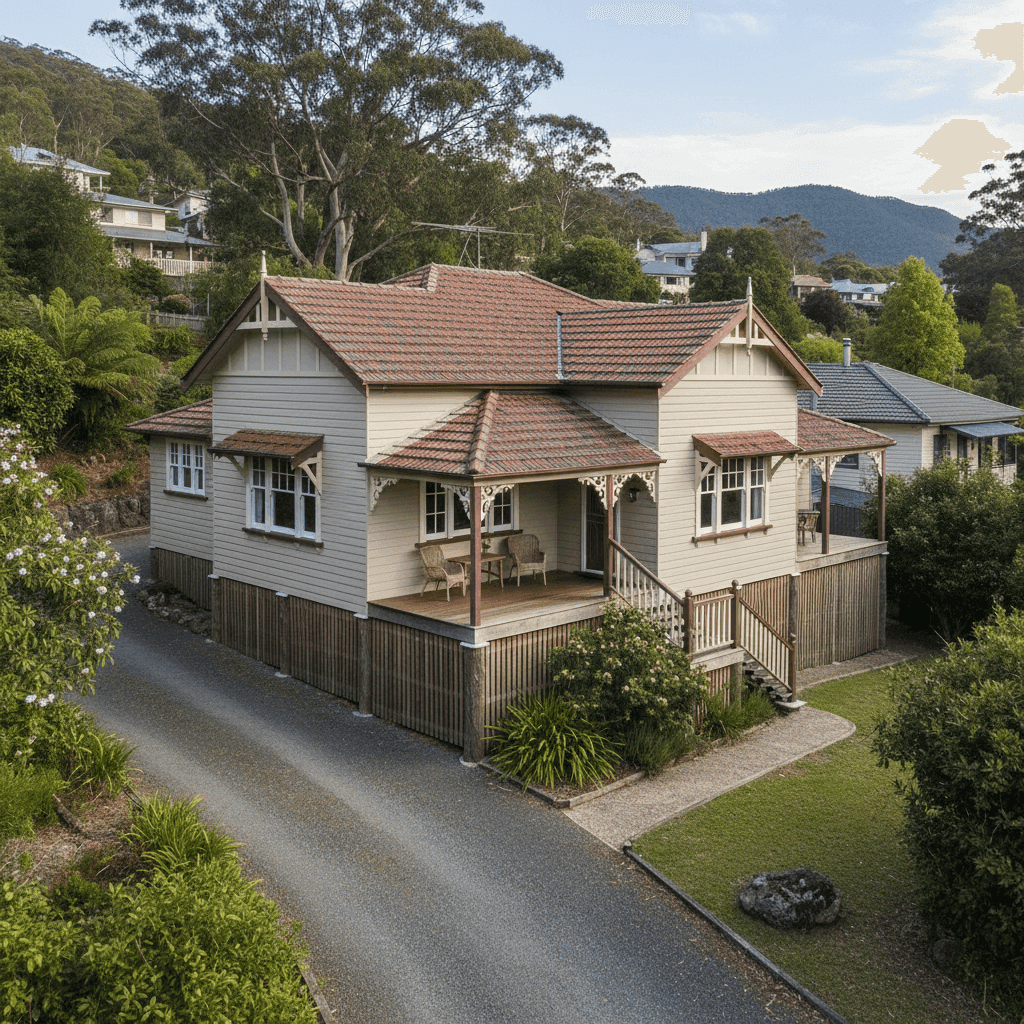

Construction Year (1980)

A home built in 1980 sits in an interesting middle ground — old enough to carry some age-related risk, but built after many of the more problematic construction eras. Insurers will factor in the likelihood of ageing infrastructure such as plumbing, wiring, and roofing materials when calculating risk.

Hardiplank / Hardiflex External Walls

Fibre cement cladding like Hardiplank and Hardiflex is generally viewed positively by insurers. It's non-combustible, durable, and resistant to rot and pests — all factors that can reduce perceived risk compared to weatherboard or timber-clad homes. In a bushfire-prone region like the Blue Mountains, this is particularly relevant.

Tiled Roof

Terracotta or concrete tile roofing is considered a low-risk roofing type by most Australian insurers. Tiles are fire-resistant, long-lasting, and less susceptible to storm damage than some alternatives — all of which can contribute to a more favourable premium.

Elevated Foundation (Stumps, At Least 1m)

This property sits elevated on stumps by at least one metre. While a raised foundation can improve ventilation and reduce moisture issues, it may also introduce some complexity around underfloor access and structural vulnerability in storm or flood events. Insurers assess this differently depending on the provider.

Ducted Climate Control

The presence of ducted climate control is a notable inclusion — it adds to the overall replacement value of the home and is factored into the sum insured. Ensuring this system is adequately covered within your building sum insured is important.

Six Bedrooms, 139 sqm

The combination of six bedrooms within a 139 sqm footprint suggests a compact but well-utilised layout — perhaps a heritage-era home with smaller room sizes. The sum insured of $627,200 should be regularly reviewed to ensure it accurately reflects current rebuilding costs, particularly given ongoing construction cost inflation across Australia.

---

Tips for Homeowners in Katoomba

1. Review your sum insured annually Construction costs have risen significantly in recent years. A sum insured that was adequate two or three years ago may no longer cover the full cost of rebuilding your home. Use a building cost calculator or speak with a quantity surveyor to make sure you're not underinsured.

2. Understand your bushfire risk The Blue Mountains is one of Australia's most bushfire-prone regions. Check your property's Bushfire Attack Level (BAL) rating through the NSW Rural Fire Service, and make sure your policy covers bushfire damage. Some insurers in high-risk zones apply significant loadings — or may decline cover altogether.

3. Consider your excess carefully A $5,000 building excess reduces your annual premium but means a larger out-of-pocket cost if you claim. If you have the financial buffer to absorb a $5,000 expense, this can be a smart strategy. If not, it may be worth comparing quotes with a lower excess to find a balance that suits your situation.

4. Don't set and forget Insurance is not a once-a-decade decision. Comparing quotes at renewal — even if you're happy with your current insurer — is one of the simplest ways to avoid paying more than you need to. Market conditions shift, and so do insurers' appetites for different property types.

---

Compare Your Own Quote

Whether you're a first-time buyer in the Blue Mountains or a long-time Katoomba local, getting a second opinion on your home insurance never hurts. CoverClub makes it easy to compare building and contents insurance quotes side by side, so you can see exactly how your premium stacks up.