If you own a free standing home in Keilor East, VIC 3033, you've probably wondered whether you're paying a fair price for home and contents insurance — or quietly overpaying while your insurer pockets the difference. This article breaks down a real insurance quote for a four-bedroom property in the suburb, benchmarks it against local, state and national data, and offers practical tips to help you get better value on your cover.

---

Is This Quote Fair?

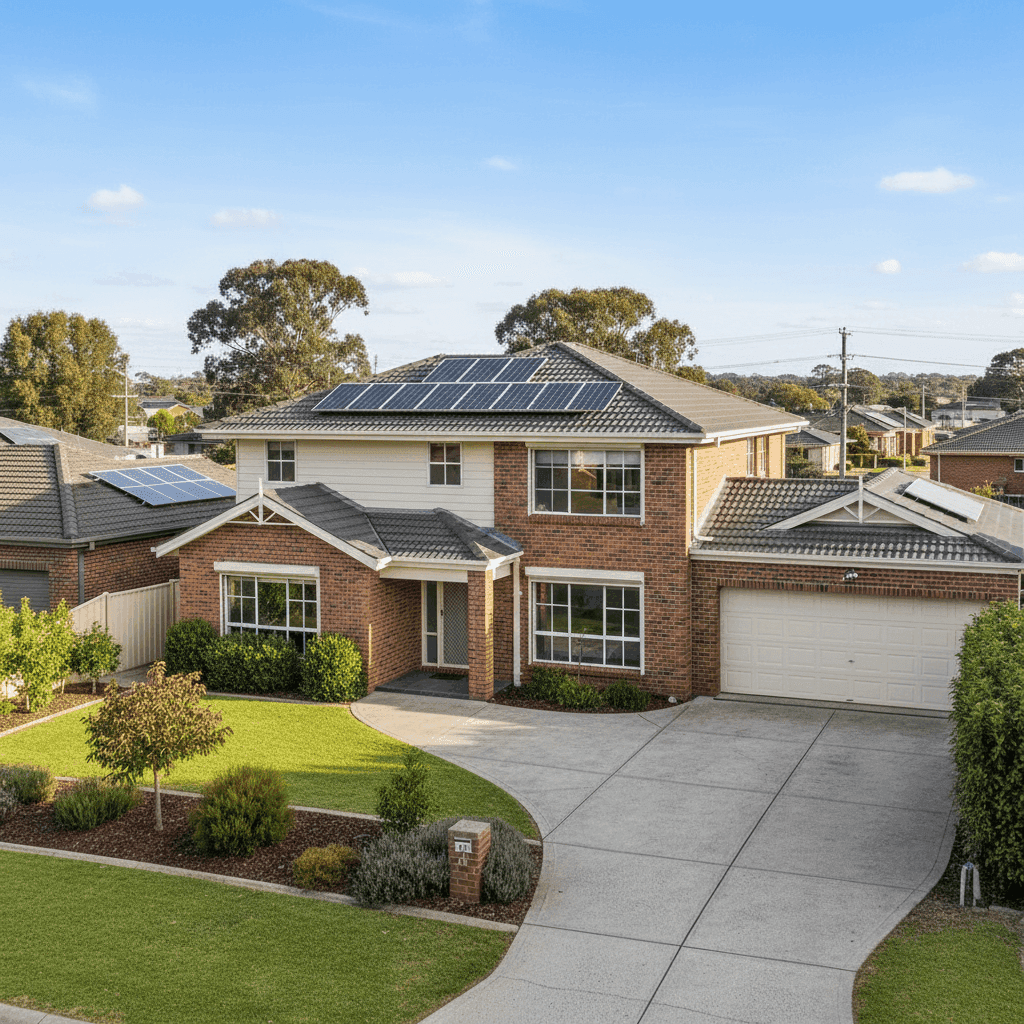

The quote in question comes in at $2,220 per year (or $210/month) for combined home and contents insurance, covering a building sum insured of $952,000 and contents valued at $249,000. Both the building and contents excess are set at $1,000.

Based on our pricing analysis, this quote is rated Expensive — above average for the area.

To put that in perspective: the average annual premium across the 31 quotes we've collected for Keilor East sits at $1,519/yr, with a median of $1,535/yr. That means this quote is running approximately $700 above the suburb average — a meaningful gap that's worth investigating before you renew.

That said, context matters. The higher-than-average sum insured ($952,000 for the building alone) and above-average fittings quality will naturally push a premium upward compared to more modestly valued properties in the same postcode. A direct apples-to-apples comparison isn't always possible, but it's still worth shopping around.

---

How Keilor East Compares

One of the more encouraging findings here is that Keilor East is actually a relatively affordable suburb for home insurance when measured against broader benchmarks. Here's how the numbers stack up:

| Benchmark | Annual Premium |

|---|---|

| This Quote | $2,220 |

| Keilor East Suburb Average | $1,519 |

| Keilor East Suburb Median | $1,535 |

| Keilor East 25th Percentile | $1,299 |

| Keilor East 75th Percentile | $1,770 |

| LGA (Brimbank) Average | $1,707 |

| VIC State Average | $3,000 |

| VIC State Median | $2,718 |

| National Average | $5,347 |

| National Median | $2,764 |

You can explore the full local data on our Keilor East insurance stats page, or compare it against all of Victoria and national averages.

While this specific quote exceeds the suburb average, it comfortably sits below both the Victorian state average and the national median — which is a meaningful silver lining. Homeowners in parts of regional Victoria or higher-risk coastal and flood-prone areas often pay significantly more. Keilor East, as a well-established metropolitan suburb in Melbourne's north-west, benefits from relatively stable risk conditions.

---

Property Features That Affect Your Premium

Every insurer prices risk differently, but certain features of this property will be influencing the premium — in both directions.

Features That May Increase the Premium

- High sum insured: At $952,000 for the building, this is a substantial replacement value. Larger, more expensive homes cost more to rebuild, and insurers price accordingly.

- Above-average fittings quality: Premium fixtures, high-end flooring (timber and laminate), and quality fittings all increase the cost of a full rebuild or contents replacement. Insurers factor this into their calculations.

- Solar panels: While solar panels are a great investment for energy savings, they add to the replacement value of the property and can introduce additional risk factors (such as electrical faults), which may nudge premiums slightly higher.

- Ducted climate control: A full ducted HVAC system is an expensive item to repair or replace and is typically included in the building sum insured.

Features That May Help Keep Costs Down

- Brick veneer construction: Brick veneer is generally regarded as a durable and fire-resistant building material, which insurers tend to view favourably compared to timber-framed exteriors.

- Tiled roof: Like brick veneer, a tiled roof is considered lower risk than some alternatives (such as Colorbond or older materials), particularly for hail and fire events.

- Concrete slab foundation: Slab foundations are structurally sound and not prone to the same subsidence or movement risks as some older footing types.

- No pool: Pools introduce liability and maintenance risks. Not having one removes a common premium driver.

- Not in a cyclone risk zone: Properties in northern Australia face significantly higher premiums due to cyclone exposure. Being in metropolitan Melbourne means this risk is simply not a factor.

- Built in 2001: A home built in the early 2000s benefits from modern building codes without the age-related wear concerns that affect properties built decades earlier.

---

Tips for Homeowners in Keilor East

If you're looking to make sure you're getting the best value on your home insurance, here are four practical steps worth taking:

1. Review Your Sum Insured Annually

Building costs fluctuate with material and labour prices. It's worth checking that your sum insured accurately reflects what it would actually cost to rebuild your home today — not over-insuring (which wastes money) and not under-insuring (which leaves you exposed). Use a building cost calculator as a starting point.

2. Shop the Market at Renewal Time

Loyalty doesn't always pay in insurance. Insurers often reserve their best rates for new customers, meaning long-standing policyholders can quietly drift into above-average pricing. Comparing quotes at renewal — even just once a year — is one of the most effective ways to keep costs in check. Get a fresh quote at CoverClub to see what's available for your property.

3. Consider Your Excess Level

This quote carries a $1,000 excess on both building and contents. Opting for a higher voluntary excess can meaningfully reduce your annual premium. If you have an emergency fund and are unlikely to make small claims, a higher excess can be a smart trade-off.

4. Bundle Building and Contents — But Check the Maths

Combined home and contents policies (like this one) are often priced competitively, but that's not always the case. It's worth getting separate quotes for building-only and contents-only cover to confirm that bundling is actually delivering a saving for your specific situation.

---

Compare Your Quote with CoverClub

Whether you're reviewing an existing policy or shopping for cover on a new property, CoverClub makes it easy to benchmark your premium against real data from your suburb, state and across Australia. Our home insurance comparison tool lets you see where your quote sits — and whether there's a better deal out there. Don't just accept the renewal notice. Take five minutes to compare.