If you own a free standing home in Kendall, NSW 2439, you already know the appeal — a quiet Mid North Coast community nestled between the Manning Valley hinterland and the coast. But when it comes to home insurance, knowing whether you're paying a fair price can be tricky without the right data to benchmark against. This article breaks down a real home and contents insurance quote for a four-bedroom property in Kendall, examining what's driving the premium and how it stacks up against local, state, and national figures.

---

Is This Quote Fair?

The quote in question comes in at $2,607 per year (or $267/month) for combined home and contents cover, with a building sum insured of $904,000 and contents valued at $220,000. The building excess sits at $3,000, with a separate $1,000 excess for contents claims.

Our price rating for this quote is CHEAP — below average — and the numbers back that up convincingly.

The suburb average for Kendall is $6,053 per year, meaning this quote is paying less than half of what most comparable properties in the postcode are quoted. Even against the suburb's 25th percentile — the point at which 75% of quotes are more expensive — of $3,364/yr, this quote still comes in well under the mark. That's a meaningful saving by any measure.

For a property of this size and value, landing a premium this far below the local average is a strong result. Of course, premiums vary significantly depending on the insurer, the specific risk profile of the property, and the level of cover selected — but this quote represents genuine value.

---

How Kendall Compares

To put this quote in proper context, it helps to look at the broader pricing landscape.

| Benchmark | Premium |

|---|---|

| This Quote | $2,607/yr |

| Kendall Suburb Average | $6,053/yr |

| Kendall Suburb Median | $6,010/yr |

| Kendall 25th Percentile | $3,364/yr |

| Port Macquarie-Hastings LGA Average | $7,001/yr |

| NSW State Average | $9,528/yr |

| NSW State Median | $3,770/yr |

| National Average | $5,347/yr |

| National Median | $2,764/yr |

(Based on 23 quotes sampled for the Kendall postcode)

A few things stand out here. The NSW state average of $9,528/yr is notably high — driven in part by elevated premiums in flood-prone, bushfire-affected, and coastal regions across the state. The Port Macquarie-Hastings LGA average of $7,001/yr also reflects the elevated risk profile of properties in this coastal hinterland region.

Against the national average of $5,347/yr, this quote is still well below the mark. Even the national median of $2,764/yr — which is the midpoint across all Australian quotes in our database — is only marginally higher than what's been quoted here.

In short: this is a competitively priced policy in a market where premiums can run very high.

---

Property Features That Affect Your Premium

Several characteristics of this property influence how insurers assess and price the risk.

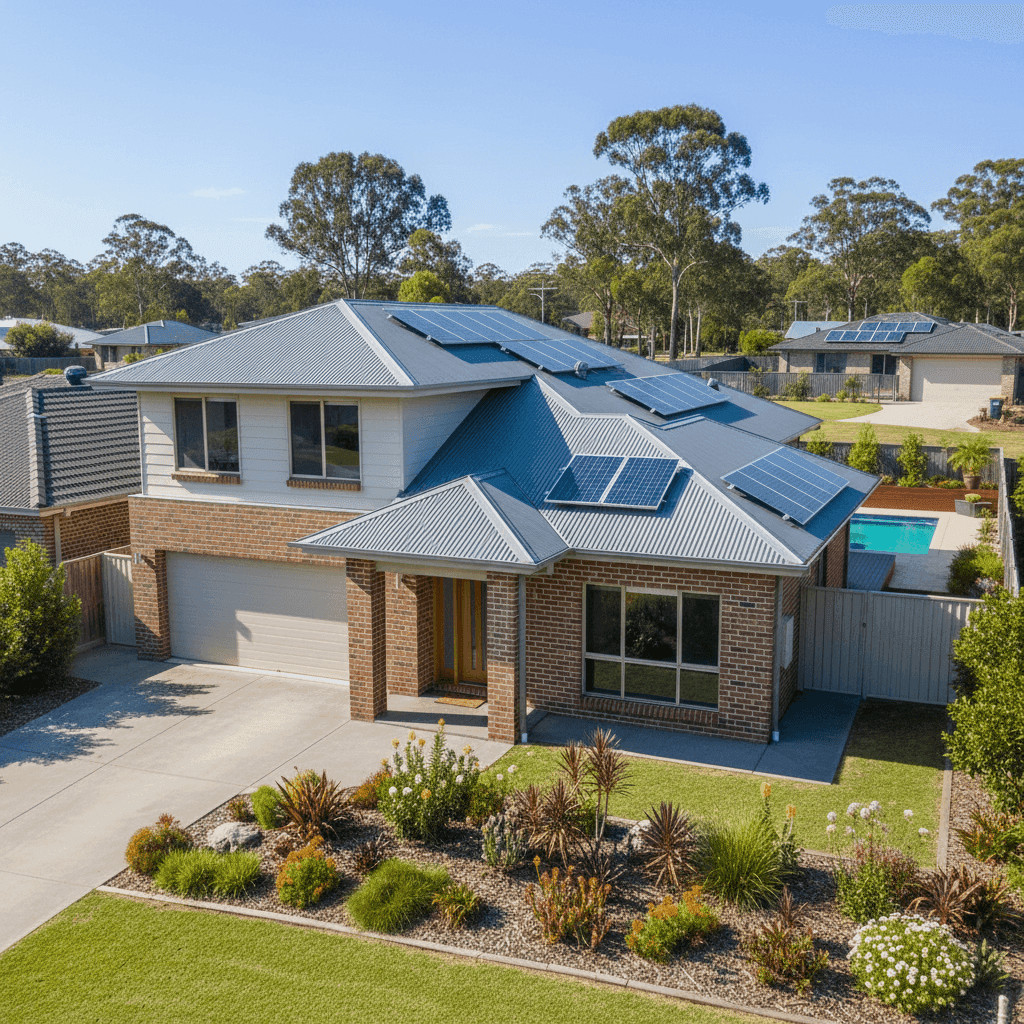

Brick Veneer Walls & Colorbond Roof

Brick veneer is one of the most common wall types in Australian homes and is generally viewed favourably by insurers. It offers solid fire resistance and structural durability. Paired with a steel Colorbond roof — which is lightweight, corrosion-resistant, and performs well in high-wind conditions — this combination tends to attract more competitive premiums than, say, timber weatherboard or fibrous cement cladding.

Slab Foundation

A concrete slab foundation is considered low-risk from an insurer's perspective. Unlike homes on stumps or piers, slab homes have no underfloor cavity, which reduces the risk of pest damage, moisture ingress, and certain types of structural movement claims.

Built in 1986

At around 38–39 years old, this home sits in an age bracket where insurers may start to factor in the potential for ageing systems — plumbing, wiring, and roofing materials — to contribute to claims. That said, a well-maintained home of this era with modern materials (like the Colorbond roof) can still attract solid pricing.

Swimming Pool

The presence of a pool adds a layer of liability risk and increases the overall replacement cost of the property. Insurers typically account for the pool in the building sum insured, and some may apply specific conditions around pool fencing compliance.

Solar Panels

Solar panels are increasingly common on Australian homes, and most insurers now include them as part of the building cover — but it's worth confirming this with your insurer. Panels can be damaged by hail, storms, or falling debris, and the cost to replace a full system can be significant. Ensuring your sum insured of $904,000 accounts for the replacement value of your solar installation is important.

268 sqm Building Size

At 268 square metres, this is a generously sized family home. Building sum insured calculations should reflect the full cost of rebuilding at current construction rates — not the market value of the property. With construction costs having risen sharply in recent years across regional NSW, it's worth reviewing your sum insured regularly to avoid being underinsured.

---

Tips for Homeowners in Kendall

1. Review Your Sum Insured Annually

Construction costs in regional NSW have climbed significantly over the past few years. A sum insured set even two or three years ago may no longer reflect the true cost to rebuild your home. Use a building cost calculator or speak with a local builder to sense-check your coverage.

2. Confirm Solar Panels Are Covered

Ask your insurer explicitly whether your solar panel system — including inverters and mounting hardware — is included under your building policy. Some policies cover it automatically; others require it to be listed separately. Given the cost of a full residential system, this is not a detail to overlook.

3. Shop Around at Renewal

Even if your current premium is competitive, it pays to compare at each renewal. Insurers regularly re-price risk, and a policy that was cheap this year may not be next year. Platforms like CoverClub make it easy to benchmark your renewal quote against the market.

4. Check Your Pool Compliance

If you have a swimming pool, ensure your pool fencing meets current NSW regulations. Non-compliant pool fencing can affect liability claims and, in some cases, your insurer's willingness to pay out. The NSW Government's pool register is a good starting point for checking your obligations.

---

Compare Your Own Quote

Whether you're renewing your policy or shopping for the first time, comparing quotes is the single most effective way to avoid overpaying. CoverClub aggregates real premium data from across Australia so you can see exactly where your quote sits relative to your suburb, your state, and the national market.

Get a home insurance quote and compare it instantly →

You can also explore detailed pricing stats for Kendall and the 2439 postcode, or browse NSW home insurance data and national benchmarks to get the full picture.