Khancoban is a small alpine township in the Snowy Mountains region of New South Wales, nestled near the Victorian border and the Kosciuszko National Park. It's a scenic and relatively quiet community, but that doesn't mean home insurance is straightforward here. For owners of a free standing home in this area, understanding what drives your premium — and whether you're paying too much — can make a real difference to your household budget.

This article breaks down a recent home and contents insurance quote for a four-bedroom, two-bathroom free standing home in Khancoban, examines how it stacks up against local, state, and national benchmarks, and offers practical advice for homeowners looking to get better value from their cover.

---

Is This Quote Fair?

The annual premium on this quote comes in at $5,405 per year (or $518/month), covering a building sum insured of $646,000 and $50,000 in contents, with a $1,000 excess on both building and contents claims.

Our price rating for this quote is Expensive — Above Average.

To put that in context: the average premium for comparable quotes in the Khancoban suburb sits at just $2,546 per year, with a median of $2,498. This quote is more than double the local average, which is a significant gap worth investigating.

That said, it's important to note that the building sum insured of $646,000 is a key driver here. A higher insured value means a higher premium, almost without exception. If nearby properties are insured for less, that alone could explain much of the difference. Before assuming you're being overcharged, it's worth confirming your sum insured reflects the true rebuild cost of your home — not just what you paid for it or what it's currently worth on the market.

---

How Khancoban Compares

Here's how this quote measures up across different geographic benchmarks:

| Benchmark | Average Premium |

|---|---|

| Khancoban (suburb) | $2,546/yr |

| NSW (state) | $9,528/yr (avg) / $3,770/yr (median) |

| National | $5,347/yr (avg) / $2,764/yr (median) |

| Federation LGA | $7,789/yr |

| This quote | $5,405/yr |

A few things stand out from this data. The NSW state average of $9,528 is heavily skewed by high-value and high-risk properties — the median of $3,770 is a more reliable comparison point for most homeowners. Against that measure, this quote at $5,405 is notably above the state median.

Interestingly, this quote is very close to the national average of $5,347, suggesting it may be more in line with broader market pricing than local Khancoban comparisons would imply. The suburb sample size of just 14 quotes is relatively small, which can make local averages less reliable as a benchmark.

You can explore the full data for your area at CoverClub's Khancoban suburb stats page, or compare against the broader NSW state insurance data and national averages.

---

Property Features That Affect Your Premium

Several characteristics of this property have a direct bearing on the premium calculated:

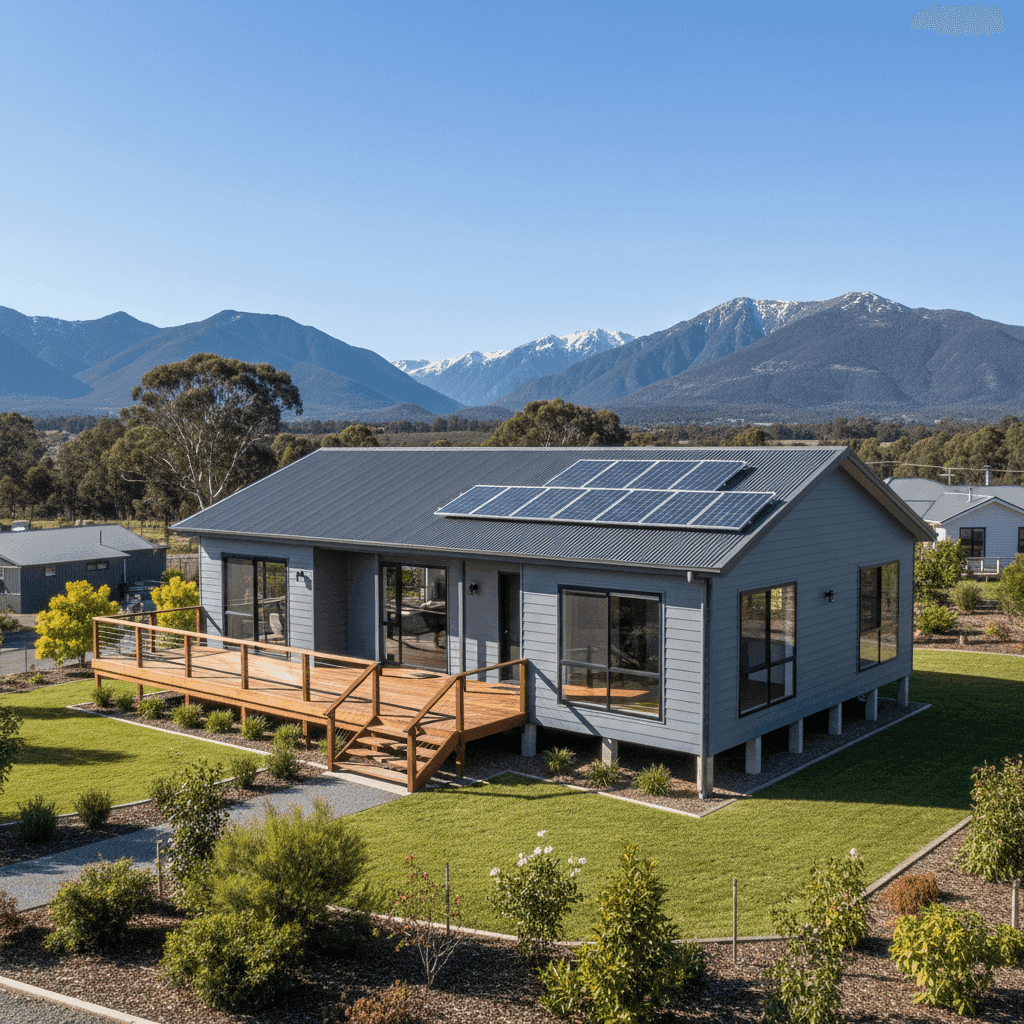

Hardiplank/Hardiflex Cladding

The external walls are constructed with Hardiplank (also known as Hardiflex) — a fibre cement product that is generally well-regarded by insurers. It's more resistant to fire and rot than timber weatherboards, which can work in your favour when it comes to risk assessment.

Steel/Colorbond Roof

A Colorbond steel roof is considered a low-risk roofing material by most Australian insurers. It's durable, fire-resistant, and performs well in harsh weather conditions — all factors that can positively influence your premium compared to, say, older tile or iron roofing.

Stump Foundation & Elevated Construction

The home sits on stumps and is elevated by less than one metre. While this style of construction is common in regional and alpine areas, some insurers factor in the elevated nature of the build when assessing structural risk. It can also affect vulnerability to certain weather events, though at less than a metre of elevation the impact is generally modest.

Solar Panels

This property has solar panels installed. Solar systems add to the replacement value of the home and can slightly increase premiums, but they're a worthwhile feature that many insurers now accommodate as standard.

Ducted Climate Control

Ducted climate control systems are a significant fixed asset in the home. They contribute to the overall rebuild and replacement cost, which is appropriately reflected in the building sum insured.

Building Size & Age

At 214 square metres and built in 2009, this is a reasonably modern, mid-to-large sized home. The construction year means it was built under more recent building codes, which can be a positive factor for insurers assessing structural integrity.

Vinyl Flooring

Vinyl flooring is a practical, cost-effective choice that is generally neutral in terms of insurance risk. It doesn't significantly inflate the contents or building replacement cost the way hardwood or high-end finishes might.

---

Tips for Homeowners in Khancoban

1. Review Your Sum Insured Carefully

At $646,000, the building sum insured is the single biggest lever on your premium. Make sure this figure reflects the actual cost to rebuild your home from scratch — including materials, labour, and any site-specific challenges like alpine access. Overinsuring inflates your premium unnecessarily, while underinsuring leaves you exposed. Consider using a building cost calculator or consulting a quantity surveyor.

2. Shop Around — Especially in a Small Market

With only 14 quotes in the local sample, the Khancoban insurance market is thin. That means there's likely significant variation between insurers, and the difference between the cheapest and most expensive policy could be substantial. Comparing quotes through CoverClub is a fast way to see what's available for your specific property.

3. Consider Adjusting Your Excess

This policy carries a $1,000 excess on both building and contents. Opting for a higher excess — say, $2,000 or $2,500 — can meaningfully reduce your annual premium. Just make sure the excess is an amount you could comfortably cover if you needed to make a claim.

4. Bundle Contents Thoughtfully

The $50,000 contents sum insured is on the lower end for a four-bedroom home. Before adjusting, do a proper contents stocktake — furniture, appliances, electronics, clothing, and valuables all add up quickly. Getting the contents figure right means you're neither overpaying nor underinsured after a loss.

---

Compare Your Options with CoverClub

Whether this quote feels right or leaves you wondering if there's a better deal out there, the smartest move is to compare. CoverClub makes it easy to get multiple home and contents insurance quotes for your Khancoban property in minutes — so you can make a confident, informed decision. Start your comparison here and find out what the market is really offering for your home.