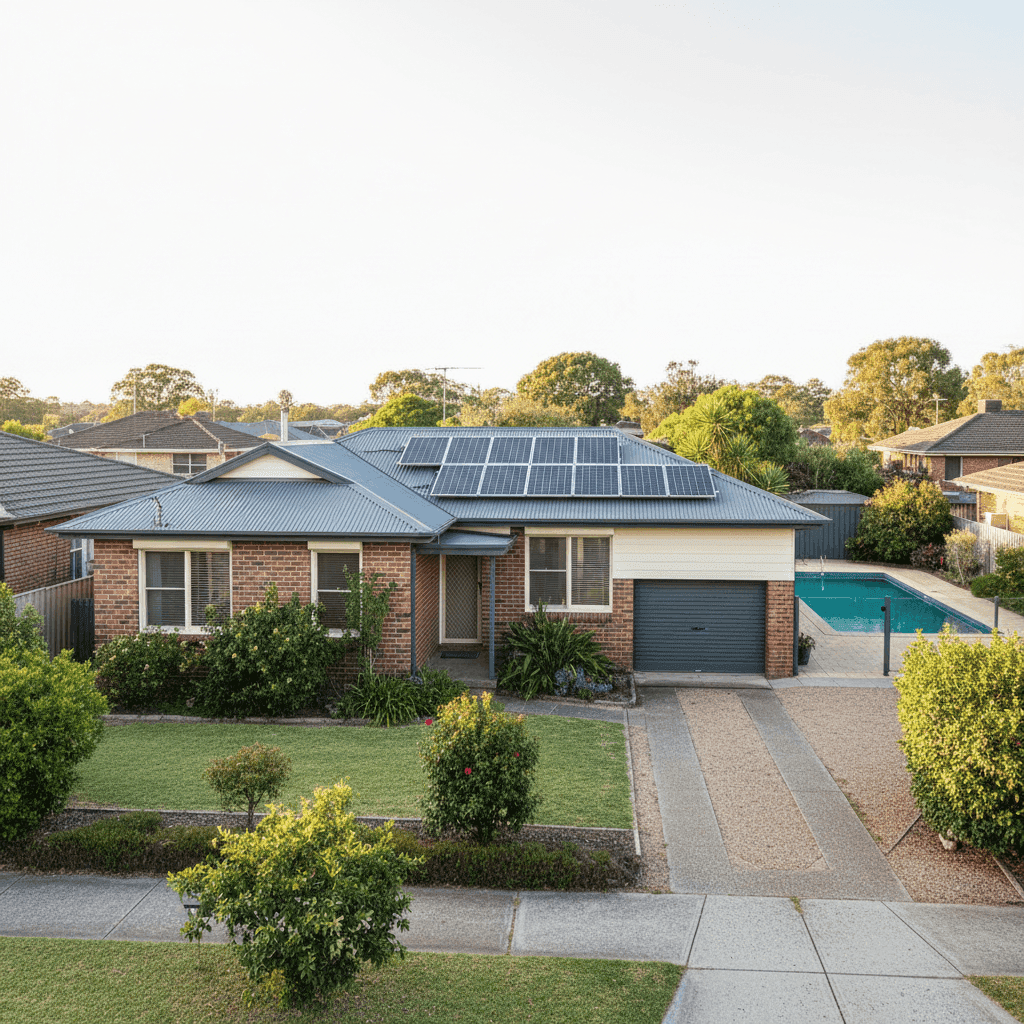

Kidman Park is a well-established suburb in Adelaide's inner-west, sitting within the City of Charles Sturt. Known for its leafy streets and solid post-war housing stock, it's the kind of neighbourhood where double brick homes from the 1960s are still going strong — and still need protecting. This article breaks down a real home and contents insurance quote for a four-bedroom free standing home in Kidman Park (SA 5025), rated Fair (Around Average), and helps you understand what's driving the premium and whether there's room to do better.

---

Is This Quote Fair?

The quote in question comes in at $3,171 per year (or $310/month) for combined home and contents cover, with a building sum insured of $361,000 and contents valued at $100,000. The building excess is set at $3,000, and the contents excess at $600.

Our price rating for this quote is Fair — Around Average, which means it's broadly in line with what similar properties in the area are paying, though it's not the sharpest price on the market.

To put that in perspective:

- The suburb average for Kidman Park is $2,434/yr, and the median sits at $1,983/yr — so this quote is notably above both figures.

- At the state level, the South Australian average is $1,933/yr and the median is $1,787/yr — again, this quote exceeds those benchmarks.

- However, zooming out to the national picture, the story shifts. The national average is $2,965/yr and the national median is $2,716/yr — meaning this quote is actually tracking above the national average too, though not dramatically so.

It's worth noting that the suburb sample size is relatively small (5 quotes), so the local averages should be interpreted with some caution. That said, the quote is clearly sitting in the upper half of the local range — the 75th percentile for Kidman Park is $4,249/yr, so there's still meaningful headroom above this price before it becomes genuinely expensive.

For a deeper look at pricing trends in the area, visit the Kidman Park insurance stats page.

---

How Kidman Park Compares

Understanding where Kidman Park sits relative to broader benchmarks is useful context for any homeowner reviewing their policy.

| Benchmark | Average Premium | Median Premium |

|---|---|---|

| Kidman Park (SA 5025) | $2,434/yr | $1,983/yr |

| Charles Sturt LGA | $1,825/yr | — |

| South Australia | $1,933/yr | $1,787/yr |

| National | $2,965/yr | $2,716/yr |

Interestingly, Kidman Park's average premium is slightly higher than the broader Charles Sturt LGA average of $1,825/yr and the South Australian state average — suggesting that specific property characteristics or insurer pricing for this postcode may push costs up a little. At the same time, Kidman Park premiums are broadly lower than the national average, which reflects South Australia's generally more affordable insurance environment compared to states like Queensland or New South Wales.

You can explore South Australian home insurance statistics and national benchmarks to see how the broader market is moving.

---

Property Features That Affect Your Premium

Several characteristics of this particular property have a meaningful influence on what insurers charge. Here's how each one plays a role:

Double Brick Construction

Double brick is generally viewed favourably by insurers. It's durable, fire-resistant, and holds up well over time — all factors that reduce the likelihood of a major claim. This construction type is common in Adelaide's older suburbs and can work in your favour when negotiating premiums.

Steel/Colorbond Roof

Colorbond roofing is another positive signal for insurers. It's lightweight, resistant to corrosion and bushfire embers, and requires less maintenance than older tile or terracotta roofs. This should help moderate the roofing component of your premium.

Built in 1968

The age of the home is a double-edged sword. A well-maintained 1968 build in double brick is structurally sound, but older homes can carry higher risk around plumbing, electrical wiring, and other systems that may not have been updated. Insurers often factor in the age of a property when calculating replacement costs and risk profiles.

Slab Foundation

Concrete slab foundations are standard and generally unproblematic from an insurance perspective, particularly in the relatively stable soils of Adelaide's inner-west.

Swimming Pool

A pool adds to the insured value of the property and introduces additional liability considerations. Most insurers will factor the pool into the building sum insured and may assess public liability exposure — particularly relevant if you have visitors or tenants.

Solar Panels

Solar panels are increasingly common on Australian homes, but they do add to the replacement cost of the building and can be a point of contention in claims (e.g., storm or hail damage). Ensure your policy explicitly covers solar panels as part of the building sum insured — some policies require you to list them separately.

No Ducted Climate Control

The absence of ducted air conditioning slightly reduces the complexity and replacement cost of the home's mechanical systems, which can modestly reduce premiums compared to properties with full ducted systems.

139 sqm Building Size

At 139 sqm, this is a moderately sized four-bedroom home. The building sum insured of $361,000 works out to roughly $2,597/sqm — a reasonable figure for double brick construction in Adelaide, though it's always worth having your sum insured independently verified to avoid underinsurance.

---

Tips for Homeowners in Kidman Park

1. Review your sum insured annually Construction costs have risen significantly in recent years. A building sum insured set a few years ago may no longer reflect the true cost of rebuilding your home. Use an independent building cost calculator or speak with a quantity surveyor to make sure you're not underinsured — especially with a double brick home, which can be more expensive to rebuild than a brick veneer equivalent.

2. Consider adjusting your excess This quote carries a relatively high building excess of $3,000. Raising your excess is one of the most straightforward ways to reduce your annual premium — but make sure it's an amount you could genuinely afford to pay out of pocket in the event of a claim. The contents excess of $600 is more modest and reasonable for most households.

3. Check your solar panel and pool coverage Given this property has both solar panels and a swimming pool, it's worth reading the fine print carefully. Confirm that both are explicitly covered under your policy, understand any sub-limits that apply, and check whether pool equipment (pumps, filters, heating) is included in the building or contents section.

4. Shop around at renewal time A "Fair" rating means this quote isn't the cheapest available — and loyalty doesn't always pay with home insurance. Insurers frequently offer better pricing to new customers than to existing ones. Set a reminder to compare quotes at least 30 days before your renewal date to give yourself time to switch if a better deal is available.

---

Compare Your Options at CoverClub

Whether you're reviewing an existing policy or shopping for cover on a new property, comparing quotes is the single most effective way to make sure you're not overpaying. Get a home insurance quote at CoverClub and see how your premium stacks up against the market — it takes just a few minutes and could save you hundreds of dollars a year.