If you own a free standing home in Kilsyth, VIC 3137, you've probably wondered whether you're paying a fair price for your home and contents insurance — or whether you could be doing better. This article breaks down a real insurance quote for a four-bedroom, two-bathroom brick veneer home in Kilsyth, and puts it in context against suburb, state, and national benchmarks to help you make a more informed decision.

---

Is This Quote Fair?

The quote in question comes in at $2,462 per year (or $236/month) for combined home and contents cover, with a building sum insured of $760,000 and contents valued at $190,000. Both the building and contents excess sit at $1,000.

Our price rating for this quote is EXPENSIVE — above average for the Kilsyth area.

To understand why, it helps to look at what other homeowners in the same suburb are paying. Based on data from 30 quotes collected in Kilsyth, the suburb average premium is $1,448/yr and the median sits at $1,462/yr. That means this quote is running approximately 70% above the local average — a significant gap that's worth investigating before renewing.

It's worth noting that the suburb's 75th percentile sits at $1,855/yr, meaning even among the pricier end of local quotes, this one still stands out. Only a small proportion of Kilsyth homeowners are paying at this level.

---

How Kilsyth Compares

Zooming out to a broader view, the picture becomes more nuanced.

| Benchmark | Premium |

|---|---|

| This quote | $2,462/yr |

| Kilsyth suburb average | $1,448/yr |

| Kilsyth suburb median | $1,462/yr |

| Maroondah LGA average | $2,133/yr |

| VIC state average | $3,000/yr |

| VIC state median | $2,718/yr |

| National average | $5,347/yr |

| National median | $2,764/yr |

When you look at Victoria-wide insurance data, this quote actually sits below the state average of $3,000/yr and under the state median of $2,718/yr. Compared to national benchmarks, it's considerably cheaper than both the national average ($5,347/yr) and the national median ($2,764/yr).

So what's going on? The answer largely comes down to what's being insured and for how much. A $760,000 building sum insured is a substantial coverage amount, and adding $190,000 in contents cover naturally pushes the premium higher than what a lower-sum policy would cost. Many cheaper quotes in the suburb may be covering smaller homes, lower rebuild costs, or contents-only policies — which makes direct comparisons tricky.

The Maroondah LGA average of $2,133/yr provides perhaps the most relevant regional comparison, and this quote sits about 15% above that figure — elevated, but not dramatically so once the higher sum insured is factored in.

---

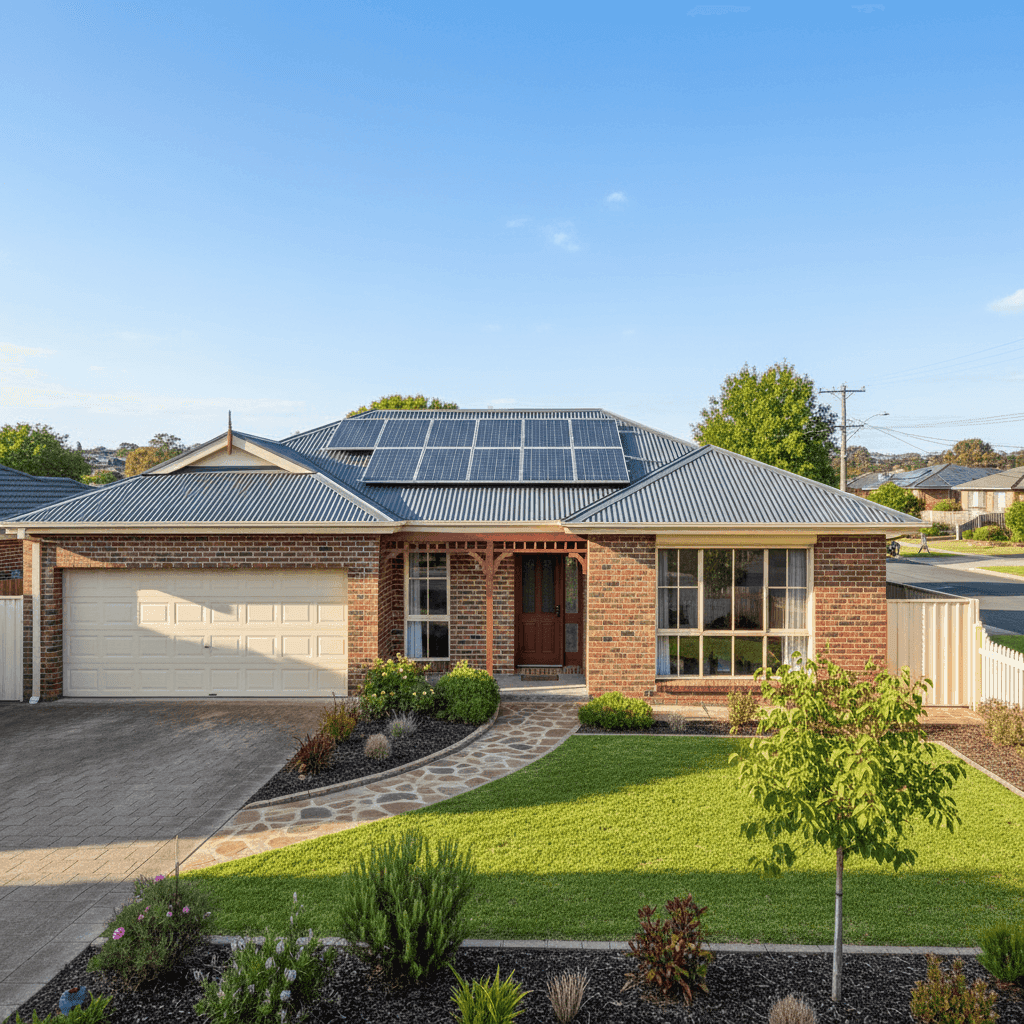

Property Features That Affect Your Premium

Several characteristics of this property will have influenced the final premium. Here's how they play out:

Brick veneer construction is generally viewed favourably by insurers. It offers solid fire resistance and durability compared to weatherboard or lightweight cladding, which can help moderate premiums.

Steel/Colorbond roofing is another positive signal — it's durable, low-maintenance, and performs well in high-wind and ember-attack scenarios. Insurers tend to price this material more favourably than older terracotta tiles or corrugated iron.

Stump foundations (also known as timber stumps or pier footings) are common in older Victorian homes. While they offer some flexibility and ventilation benefits, they can attract slightly higher premiums due to the potential for movement, rot, or pest damage over time. This home was built in 1988, so the stumps are now approaching 40 years old — worth having inspected if that hasn't been done recently.

Solar panels are an increasingly common feature but do add to the insured value of the property. Some insurers include solar panels under the building policy automatically, while others may treat them as an optional extra. It's important to confirm your policy explicitly covers solar panels for damage from storms, hail, or fire.

Ducted climate control is another higher-value fixture that contributes to the overall rebuild cost and therefore the recommended sum insured. At 153 sqm, the building size is modest, but the combination of quality fittings and installed systems like ducted HVAC can push the replacement value higher than the floor area alone might suggest.

---

Tips for Homeowners in Kilsyth

1. Review your sum insured carefully A $760,000 building sum insured is substantial for a 153 sqm home, even accounting for quality fittings and current construction costs. Use an independent building cost calculator to verify whether this figure is accurate — being over-insured means you're paying more in premiums than you need to, while being under-insured can leave you exposed after a claim.

2. Shop around at renewal time The gap between this quote and the suburb average suggests meaningful savings may be available elsewhere. Insurers use different pricing models, and loyalty doesn't always pay — in fact, long-term customers are sometimes charged more than new ones. Comparing quotes annually is one of the simplest ways to keep costs in check.

3. Check your stump foundations Given the home's age, it's worth arranging a professional inspection of the subfloor and stumps. If they're in good condition (or have been replaced with concrete stumps), this could support a lower risk assessment with some insurers. Proactive maintenance also protects you from claim complications down the track.

4. Confirm solar panel coverage With solar panels on the roof, double-check your policy wording to ensure they're explicitly covered — including for accidental damage, storm damage, and theft of inverter equipment. Not all standard home policies include solar as a default, and the cost of replacing a full system can run into the tens of thousands.

---

Compare Your Options with CoverClub

Whether you're renewing soon or just curious about what else is out there, CoverClub makes it easy to see how your current premium stacks up. Get a home insurance quote today and compare options tailored to your property in Kilsyth. You can also explore local insurance data for postcode 3137 to see exactly what your neighbours are paying.