If you own a free standing home in Kin Kin, QLD 4571, you've probably noticed that home insurance premiums in Queensland can vary wildly depending on where you live and how your home is built. This article breaks down a real building insurance quote for a 3-bedroom, 2-bathroom weatherboard home in Kin Kin — and puts that number in context against suburb, state, and national benchmarks so you can judge whether you're getting a fair deal.

---

Is This Quote Fair?

The annual premium for this property came in at $2,475 per year (or about $237 per month), covering the building only with a sum insured of $500,000 and a building excess of $2,000.

Our price rating for this quote is CHEAP — below average for the area. That's genuinely good news for the homeowner. Based on 21 quotes collected for the Kin Kin suburb, the suburb average sits at $3,422/yr and the median at $3,273/yr. This quote comes in well below both figures — and even sits beneath the 25th percentile of $2,693/yr, meaning it's cheaper than at least 75% of comparable quotes in the area.

In practical terms, that's a saving of nearly $950/yr compared to the suburb average — or close to $80 per month. Over five years, that's potentially $4,750 back in your pocket. It's worth noting, however, that premiums can differ significantly between insurers, so it always pays to compare.

---

How Kin Kin Compares

To really appreciate this quote, it helps to zoom out and look at the broader picture.

| Benchmark | Premium |

|---|---|

| This quote | $2,475/yr |

| Kin Kin suburb average | $3,422/yr |

| Kin Kin suburb median | $3,273/yr |

| Kin Kin 25th percentile | $2,693/yr |

| Kin Kin 75th percentile | $4,178/yr |

| QLD state average | $9,129/yr |

| QLD state median | $3,903/yr |

| National average | $5,347/yr |

| National median | $2,764/yr |

| Noosa LGA average | $18,770/yr |

A few things stand out here. First, the Queensland state average of $9,129/yr is extraordinarily high — this reflects the enormous variability of insurance costs across the Sunshine State, where cyclone-prone coastal areas and flood-risk zones push averages up dramatically. Kin Kin, sitting in the hinterland behind the Sunshine Coast, benefits from not being classified as a cyclone risk area, which makes a meaningful difference to premiums.

Second, the Noosa LGA average of $18,770/yr is eye-watering — but this figure is heavily skewed by high-value coastal properties and elevated risk profiles in parts of the Noosa local government area. Kin Kin, while technically within the Noosa LGA, is an inland rural township and tends to attract more moderate premiums as a result.

Compared to the national average of $5,347/yr, this quote is less than half — a strong result for any homeowner.

---

Property Features That Affect Your Premium

Several characteristics of this property are worth discussing, as they directly influence what insurers charge.

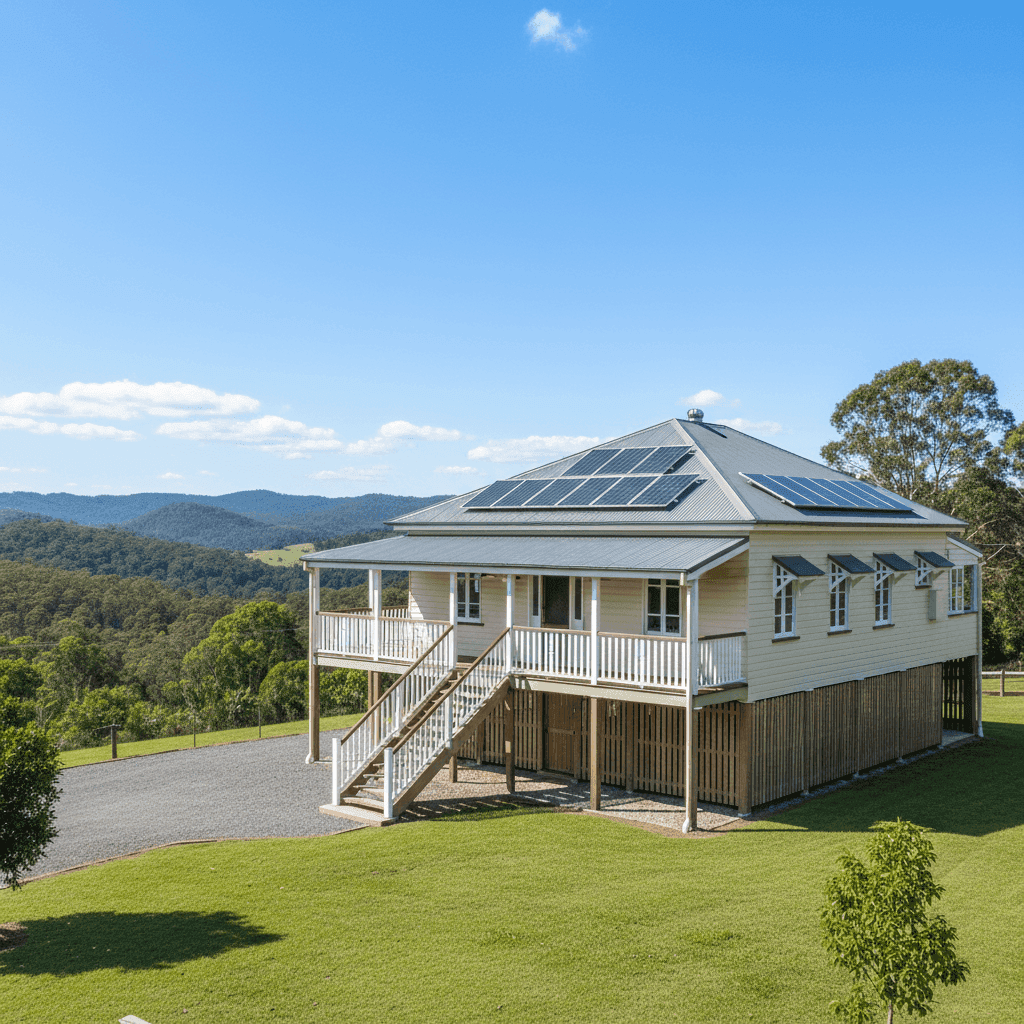

Weatherboard Timber Walls

Weatherboard timber construction is common in older Queensland homes and carries a slightly higher fire risk rating than brick veneer or double brick. Insurers factor this in, and it can nudge premiums upward compared to masonry homes. That said, well-maintained timber homes are widely insured across Australia, and the impact is generally modest.

Steel/Colorbond Roof

Colorbond steel roofing is viewed favourably by insurers. It's durable, resistant to fire, and performs well in high-wind events. This is likely contributing positively to the competitiveness of this quote.

Elevated on Stumps (at Least 1 Metre)

This is a significant feature. Homes elevated by at least a metre — classic Queenslander style — benefit from improved airflow and, critically, reduced flood exposure. Floodwater that might inundate a slab-on-ground home can pass beneath an elevated home without causing structural damage. Insurers recognise this, and it can meaningfully reduce premiums in areas with any flood history.

Construction Year: 1972

At over 50 years old, this home predates many modern building codes. Older homes can attract slightly higher premiums due to the potential for aged wiring, plumbing, and structural components. However, the 1972 construction year is also consistent with the classic elevated Queenslander style, which — as noted above — has real insurance advantages.

Solar Panels and Ducted Climate Control

The presence of solar panels adds some replacement value to the building and may slightly increase the sum insured required. Ducted climate control systems are similarly factored into building replacement costs. Both features are already accounted for under the $500,000 sum insured.

No Pool, No Cyclone Risk Zone

The absence of a pool removes a common source of liability and additional premium loading. And being outside a designated cyclone risk area is a major factor in keeping this premium competitive — many Queensland properties closer to the coast carry significant cyclone loading.

---

Tips for Homeowners in Kin Kin

1. Review your sum insured regularly Building costs have risen sharply in recent years. A $500,000 sum insured may be appropriate today, but it's worth reassessing annually to ensure it reflects current construction costs — especially for a 139 sqm home with timber construction and elevated stumps, which can be more expensive to rebuild than standard slab homes.

2. Document your solar panels and ducted systems Keep records (including serial numbers and installation receipts) for your solar panels and ducted climate control system. In the event of a claim, this documentation speeds up the process and ensures you're fully compensated.

3. Maintain your weatherboard cladding Timber weatherboard requires regular painting and maintenance to prevent rot and moisture ingress. Insurers may reduce or deny claims where damage results from lack of maintenance. A well-kept exterior also helps at renewal time.

4. Compare quotes at renewal — every year This quote is already below the suburb average, but insurance markets shift. Insurers re-price risk regularly, and the cheapest option this year may not be the best value next year. Using a comparison tool like CoverClub takes the legwork out of shopping around.

---

Get Your Own Quote

Whether you're a homeowner in Kin Kin or anywhere else in Australia, it's worth knowing how your current premium stacks up. CoverClub makes it easy to compare building and contents insurance quotes in one place — so you can see exactly where you stand.