If you own a free standing home in Kingaroy, QLD 4610, you're probably aware that insurance costs in regional Queensland can vary wildly depending on your property's age, construction, and location. This article breaks down a real home and contents insurance quote for a 3-bedroom, 2-bathroom weatherboard home in Kingaroy — and puts that number into context using suburb, state, and national benchmarks. Whether you're shopping around for the first time or reviewing your current policy, this analysis will help you understand what you're paying and why.

---

Is This Quote Fair?

The annual premium for this property came in at $2,269 per year (or around $217 per month), covering a building sum insured of $559,000 and $30,000 in contents, with a $1,000 excess on both building and contents.

Our price rating for this quote is FAIR — around average. That assessment is based on how the premium stacks up against other quotes obtained for similar properties in the Kingaroy area. It's not the cheapest option on the market, but it's well within a reasonable range — and importantly, it's not an outlier in either direction.

For context, the suburb average premium in Kingaroy is $2,238 per year, meaning this quote sits just $31 above the local average — a negligible difference. The suburb median, however, is a little lower at $2,024 per year, which suggests there are cheaper options available if you're willing to shop around. The fact that this quote falls between the median and the average is a good sign — it means you're not being significantly overcharged, though there may be room to do better.

---

How Kingaroy Compares

One of the most striking findings when you zoom out is just how well Kingaroy performs relative to the broader Queensland market. Queensland homeowners pay some of the highest insurance premiums in the country, largely driven by cyclone exposure in coastal and far north regions. The QLD state average sits at $4,547 per year, and the state median is $3,931 — both dramatically higher than what Kingaroy residents typically pay.

At $2,269, this quote is roughly half the Queensland state average — a meaningful saving that reflects Kingaroy's inland location and lower exposure to the extreme weather events that push premiums sky-high in coastal Queensland.

Compared to national benchmarks, the picture is similarly favourable. The national average premium is $2,965 per year, and the national median is $2,716. Kingaroy's quote comes in well below both figures, making this a relatively affordable postcode by Australian standards.

It's also worth noting that the South Burnett LGA average of $5,273 per year is significantly higher than what this particular quote reflects. This LGA figure likely captures a broader mix of properties — including some in higher-risk rural areas — so individual results in Kingaroy township can differ considerably. You can explore localised data for this postcode on the Kingaroy suburb stats page.

The suburb's interquartile range tells an interesting story too: the 25th percentile sits at $1,545/yr and the 75th percentile at $3,012/yr, based on a sample of 120 quotes. This $1,467 spread shows there's meaningful variation in what insurers charge for similar properties here — which underscores the value of comparing multiple quotes rather than accepting the first offer.

---

Property Features That Affect Your Premium

Several characteristics of this property are worth understanding from an insurance perspective.

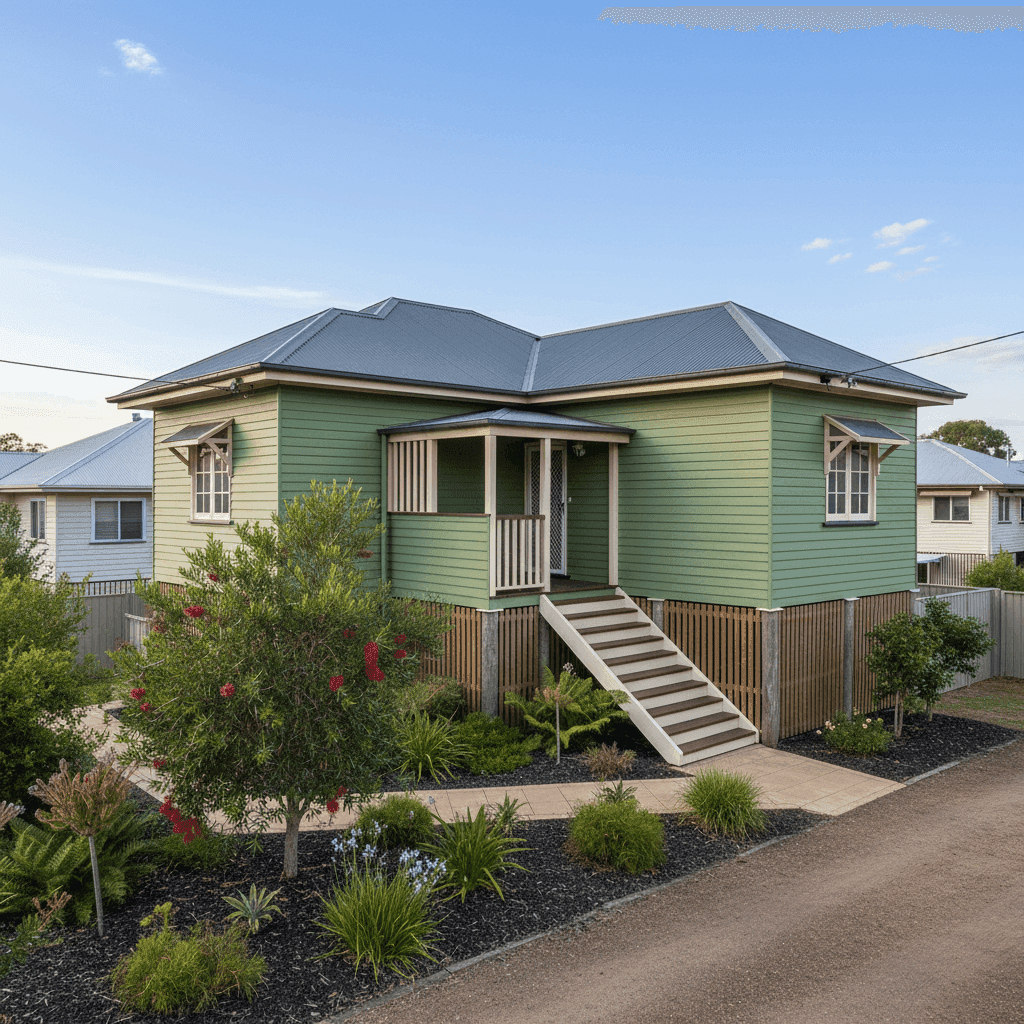

Weatherboard timber construction is one of the most significant rating factors. Timber-framed, weatherboard homes are generally considered higher risk by insurers than brick veneer or full brick properties, primarily due to fire susceptibility and the potential for moisture damage over time. A home built in 1988 will also attract scrutiny around the condition of its wiring, plumbing, and structural elements — older homes can carry higher replacement costs and a greater likelihood of claims.

The steel Colorbond roof is a positive feature. Colorbond is widely regarded as one of the more durable roofing materials in the Australian climate — resistant to corrosion, lightweight, and relatively low-maintenance. Insurers tend to view it favourably compared to older tile or fibrous cement roofing.

This home sits on stumps and is elevated by less than one metre — a classic Queensland construction style. While elevated homes can offer some protection against minor flooding, the subfloor space and timber stumps themselves can be a source of concern for insurers if not well-maintained. Timber stumps in particular may require inspection and replacement over time.

Timber and laminate flooring throughout the home adds to the replacement cost calculation, and the standard fittings quality keeps the sum insured at a reasonable level. At 139 sqm, this is a modest-sized home, and the $559,000 building sum insured reflects current construction costs rather than market value — an important distinction.

The absence of a pool, solar panels, and ducted climate control simplifies the risk profile and keeps the premium lower than it might otherwise be.

---

Tips for Homeowners in Kingaroy

1. Shop the market actively — the spread is wide. With a 25th-to-75th percentile range of over $1,400 in Kingaroy alone, there's clear evidence that different insurers price this postcode very differently. Getting at least three to four comparable quotes before renewing is one of the simplest ways to avoid overpaying.

2. Keep your timber and stumps in good condition. Insurers may ask about the condition of your subfloor structure, and some policies include exclusions for gradual deterioration. Having your stumps inspected periodically — and replacing any that are compromised — can protect both your home and your claim eligibility.

3. Review your building sum insured annually. Construction costs in regional Queensland have risen significantly in recent years. If your sum insured hasn't kept pace with current rebuild costs, you risk being underinsured in the event of a total loss. Use a building cost calculator or speak with a local builder to sense-check your coverage amount.

4. Consider your contents coverage carefully. At $30,000, the contents cover in this quote is on the lower end for a 3-bedroom, 2-bathroom home. Take stock of your furniture, appliances, clothing, and valuables — many households find they're underinsured on contents without realising it.

---

Ready to Compare?

Understanding your quote is the first step — but the real savings come from comparison. At CoverClub, we make it easy to see what multiple insurers would charge for your specific property, so you can make a confident, informed decision. Get a home insurance quote today and find out if you could be paying less for the same level of cover.