If you own a free standing home in Koonoomoo, VIC 3644, you're likely no stranger to the task of finding the right home insurance at a price that makes sense. This quiet rural locality in the Berrigan LGA sits along the Murray River corridor in northern Victoria — a region with its own unique set of risks and property characteristics that insurers pay close attention to. In this article, we break down a real home and contents insurance quote for a 4-bedroom, 3-bathroom property in Koonoomoo, compare it against local, state, and national benchmarks, and offer practical tips to help you get the best value on your cover.

---

Is This Quote Fair?

The annual premium for this property came in at $3,441 per year (or $323/month), covering a building sum insured of $712,000 and $50,000 in contents. Our pricing analysis rates this quote as FAIR — around average.

To put that in context: the quote sits above both the Victorian state average ($3,000/yr) and the state median ($2,718/yr), but it remains well below the national average of $5,347/yr. For a property of this size and construction type — 214 sqm, elevated on stumps, with fibre cement cladding and a Colorbond roof — the premium reflects a reasonable but not particularly competitive rate.

The "fair" rating means you're not being overcharged significantly, but there's a realistic chance you could find a better deal by shopping around. Given that the building sum insured is a substantial $712,000, even a modest reduction in the premium rate could translate to meaningful annual savings.

---

How Koonoomoo Compares

Understanding where your premium sits relative to broader benchmarks is one of the most useful exercises a homeowner can do. Here's how this quote stacks up:

| Benchmark | Annual Premium |

|---|---|

| This Quote | $3,441 |

| VIC State Average | $3,000 |

| VIC State Median | $2,718 |

| National Average | $5,347 |

| National Median | $2,764 |

| Berrigan LGA Average | $1,601 |

A few things stand out here. First, the Berrigan LGA average of just $1,601/yr is strikingly lower than this quote — more than half the price. This gap is likely explained by differences in building size, sum insured, and construction features rather than location risk alone. Many properties in the LGA may be older, smaller, or insured for lower replacement values. That said, it's worth exploring whether local insurers or regional specialists price this area more competitively.

Second, compared to the national average of $5,347, this quote looks quite reasonable — a reflection of the fact that Victoria, and rural northern Victoria in particular, doesn't carry the cyclone, flood surge, or bushfire premium loading that drives costs up dramatically in parts of Queensland, Western Australia, and northern NSW.

You can explore more local pricing data on the Koonoomoo suburb stats page, the Victoria state overview, or the national home insurance statistics page.

---

Property Features That Affect Your Premium

Several characteristics of this property have a direct bearing on what insurers charge. Here's what's most relevant:

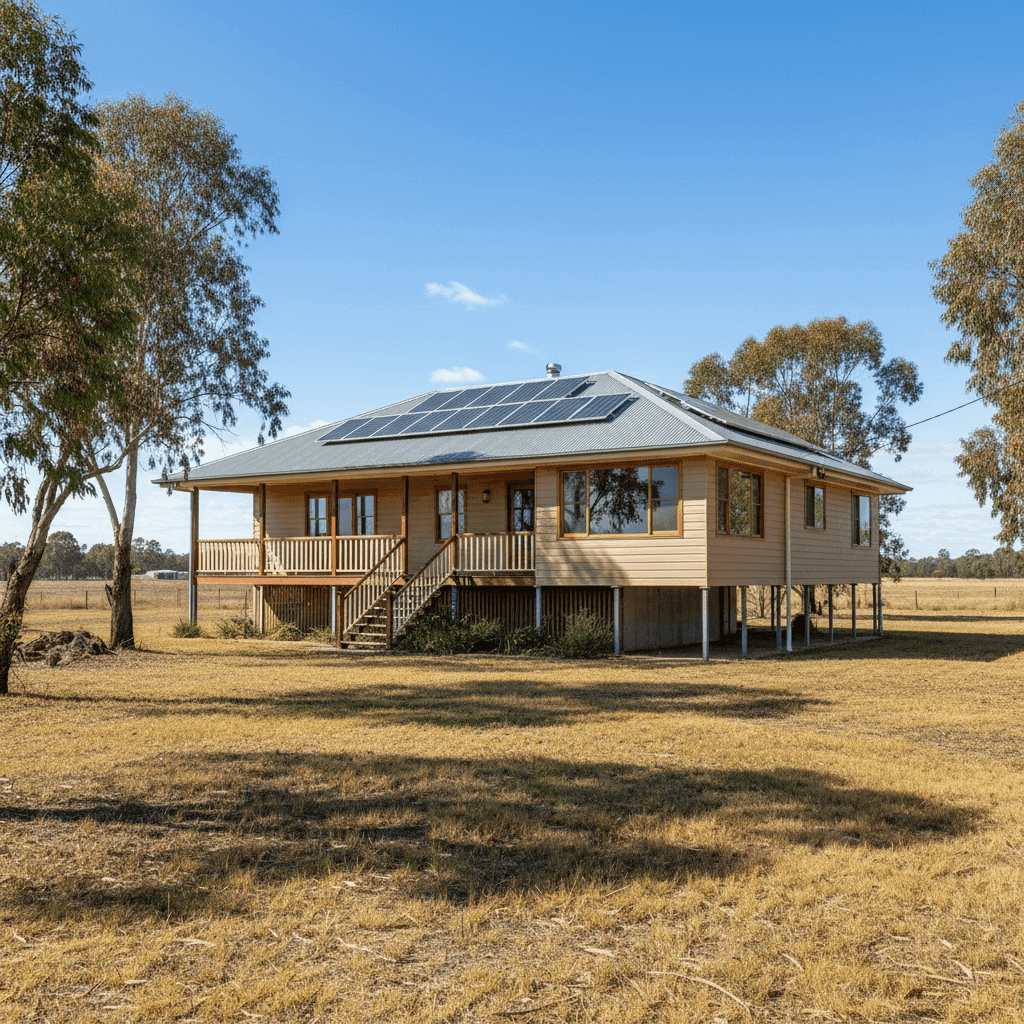

Elevated Foundation (Stumps)

This home is elevated by at least one metre on stumps — a construction style common in regional Victoria and Queensland. While this can offer some protection against surface water ingress, elevated homes can also be more expensive to repair after storm or wind events, as the sub-floor structure adds complexity. Insurers will factor this into their pricing.

Hardiplank / Hardiflex Cladding

The external walls are constructed from Hardiplank or Hardiflex — a fibre cement product that is durable, fire-resistant, and low-maintenance. From an insurance perspective, this is generally viewed favourably compared to timber weatherboard, as it carries lower fire and rot risk. It may contribute to a more competitive premium than older cladding materials.

Steel / Colorbond Roof

Colorbond steel roofing is widely regarded as one of the more insurer-friendly roof types in Australia. It's resistant to fire, lightweight, and performs well in high-wind conditions. This is a positive factor in premium calculations.

Solar Panels

The presence of solar panels adds modest replacement cost to the building sum insured and introduces some risk around electrical faults or storm damage. Most standard home insurance policies cover solar panels as part of the building, but it's worth confirming this with your insurer and ensuring the sum insured accounts for their replacement value.

Ducted Climate Control

Ducted heating and cooling systems are a significant fixed asset within the home. Damage to these systems — whether from storm, fire, or electrical surge — can be costly to repair or replace. Their inclusion is a reasonable justification for a higher sum insured and can influence premium calculations.

Building Size: 214 sqm

At 214 square metres, this is a comfortably sized family home. Larger homes cost more to rebuild, and the $712,000 sum insured reflects a realistic replacement cost for a property of this specification in regional Victoria. Underinsuring a home of this size would be a significant financial risk.

---

Tips for Homeowners in Koonoomoo

1. Review Your Sum Insured Annually

Building costs in regional Victoria have risen considerably in recent years. Make sure your $712,000 sum insured keeps pace with actual rebuild costs — including labour, materials, and any site-specific factors like the elevated stump foundation. An underinsured home can leave you significantly out of pocket after a major claim.

2. Compare Quotes Beyond Your Current Insurer

This quote is rated "fair," which means the market may have better options. Use a comparison tool like CoverClub to see how multiple insurers price your specific property. Even a 10–15% saving on a $3,441 premium is worth pursuing.

3. Ask About Bundling Discounts

Some insurers offer discounts when you hold both home and contents policies with them — which this quote already does. If you also hold car insurance or landlord cover elsewhere, check whether consolidating policies with one provider unlocks further savings.

4. Check Flood and Water Damage Definitions Carefully

Koonoomoo sits in the Murray River region, where seasonal flooding and high water tables can be a consideration. Make sure your policy clearly defines what's covered under "flood," "storm surge," and "water damage" — these terms have distinct meanings in insurance contracts, and gaps in cover can be costly.

---

Ready to Compare?

Whether you're renewing your existing policy or shopping for cover on a new property, it pays to compare. Get a home insurance quote at CoverClub and see how your premium stacks up against the broader market. With real data from properties across Victoria and Australia, CoverClub helps you make a more informed decision — not just go with whatever arrives in your renewal notice.