If you own a free standing home in Kooralbyn, QLD 4285, you're likely no stranger to the challenge of finding affordable home insurance. Nestled in the Scenic Rim region of South East Queensland, Kooralbyn is a semi-rural community that comes with its own unique set of risk factors — and those factors can have a significant impact on what you pay to protect your home. This article breaks down a real home and contents insurance quote for a 3-bedroom, 2-bathroom property in the area, and puts it in context against suburb, state, and national benchmarks.

---

Is This Quote Fair?

The quote in question sits at $4,071 per year (or $390/month), covering both building (insured for $647,000) and contents (insured for $199,000), each with a $1,000 excess.

Our price rating for this quote is Expensive — Above Average. That's not a label we assign lightly. Based on a sample of 34 quotes collected for the Kooralbyn area, the suburb average annual premium sits at $2,447, and the median is even lower at $2,242. This quote comes in at roughly 66% above the suburb average and nearly 82% above the median — a meaningful gap that warrants a closer look.

To be fair, the sum insured here is substantial. A building replacement value of $647,000 and contents coverage of $199,000 together represent a significant total insured amount, which will naturally push premiums higher than quotes with lower coverage limits. Still, even accounting for that, the premium is sitting above the 75th percentile for the suburb (which is $3,136/yr), meaning it's pricier than at least three-quarters of comparable quotes in the area.

If you're paying this rate, it's worth shopping around. You may be able to find equivalent coverage at a more competitive price point.

---

How Kooralbyn Compares

To understand whether this quote is genuinely high or simply reflective of broader market conditions, it helps to zoom out.

| Benchmark | Average Premium | Median Premium |

|---|---|---|

| Kooralbyn (4285) | $2,447/yr | $2,242/yr |

| Logan LGA | $4,617/yr | — |

| Queensland | $9,129/yr | $3,903/yr |

| National | $5,347/yr | $2,764/yr |

A few things stand out here. Queensland's average premium of $9,129 is extraordinarily high — largely driven by cyclone-prone regions in Far North Queensland, which dramatically skew the state average upward. Kooralbyn, fortunately, sits outside cyclone risk zones, which keeps local premiums considerably more grounded.

Interestingly, the Logan LGA average of $4,617/yr is actually higher than this individual quote, suggesting that within the broader council area, insurance costs can climb considerably. Kooralbyn itself trends cheaper than the LGA average, which is a positive sign for locals.

Compared to the national average of $5,347, this quote is below average — but compared to the Kooralbyn suburb median of $2,242, it's a clear outlier on the expensive end.

You can explore more local data on the Kooralbyn suburb insurance stats page, compare it against Queensland-wide figures, or benchmark against national home insurance averages.

---

Property Features That Affect Your Premium

Several characteristics of this particular property are worth examining, as they each play a role in how insurers calculate risk and price premiums.

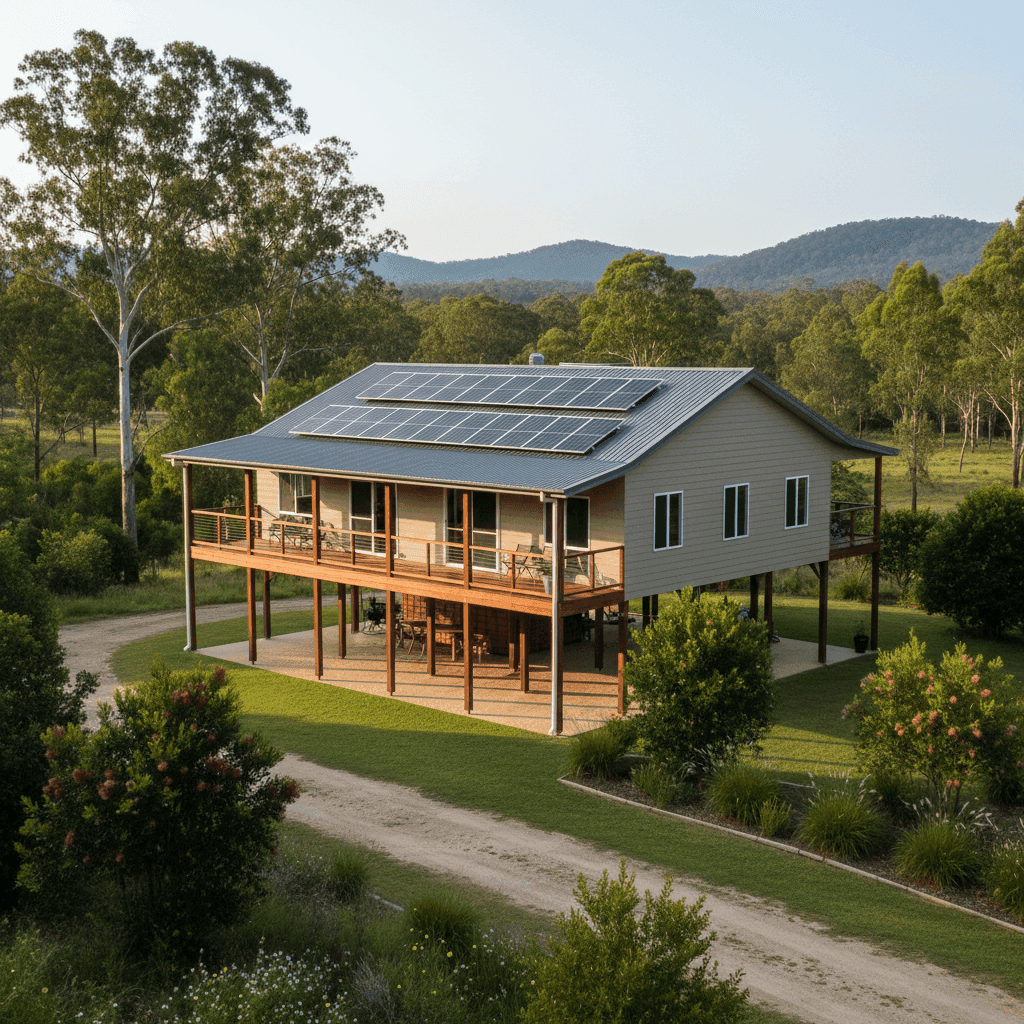

Elevated Foundation (Poles)

This home is elevated by at least 1 metre on a pole foundation — a classic Queensland construction style. Elevation can be a double-edged sword for insurance. On the positive side, it provides excellent flood mitigation, as water is less likely to reach the living areas during heavy rainfall events. On the other hand, elevated homes can be more susceptible to wind damage, and the underfloor space may introduce additional considerations for some insurers.

Hardiplank / Hardiflex External Walls

Fibre cement cladding like Hardiplank is generally viewed favourably by insurers. It's durable, fire-resistant, and low-maintenance compared to timber weatherboards. This material choice shouldn't be driving premiums up — if anything, it's a neutral-to-positive factor.

Steel / Colorbond Roof

Colorbond roofing is one of the most common and insurer-friendly roof types in Australia. It's lightweight, durable, and performs well in high-wind conditions. This is unlikely to be contributing to a higher premium.

Solar Panels

The presence of solar panels adds replacement cost to the building sum insured, and some insurers charge a modest loading for them. It's worth confirming that your solar system is explicitly covered under your policy and that the replacement value is factored into your building sum insured.

Ducted Climate Control

Ducted air conditioning is a significant fixed asset that adds to the replacement cost of the home. Like solar panels, it should be accounted for in your building sum insured — and it may contribute modestly to a higher premium.

Above-Average Fittings Quality

With above-average fittings, the cost to rebuild this home to the same standard is higher than a basic spec property. This is a legitimate driver of a higher building sum insured and, by extension, a higher premium.

Vinyl Flooring

Vinyl is a cost-effective and practical flooring choice. It's unlikely to significantly affect premium calculations either way.

---

Tips for Homeowners in Kooralbyn

1. Review Your Sum Insured Carefully

A building sum insured of $647,000 is substantial. Make sure this figure reflects the actual cost to rebuild your home (not its market value), including demolition, site costs, and professional fees. Overinsuring can lead to unnecessarily high premiums, while underinsuring leaves you exposed. Tools like the Cordell Sum Sure calculator can help you estimate an accurate rebuild cost.

2. Compare Multiple Quotes

This quote is rated as expensive relative to the local market. The single most effective way to reduce your premium is to compare offers from multiple insurers. Prices for identical coverage can vary by hundreds — sometimes thousands — of dollars. Get a comparison quote through CoverClub to see what else is available for your property.

3. Consider Your Excess Level

Both the building and contents excess on this policy are set at $1,000. Opting for a higher voluntary excess — say, $2,000 or $2,500 — can meaningfully reduce your annual premium. Just make sure you're comfortable covering that amount out of pocket in the event of a claim.

4. Bundle Building and Contents Thoughtfully

While bundling home and contents insurance with the same insurer often attracts a discount, it's not always the cheapest approach. Some insurers are more competitive on building cover, while others shine on contents. It's worth getting separate quotes for each to see if splitting the cover saves you money overall.

---

Ready to Find a Better Deal?

If your current home insurance premium feels steep, you don't have to accept it. CoverClub makes it easy to compare home and contents insurance quotes for properties in Kooralbyn and across Australia — so you can see at a glance whether you're getting fair value. Start your free quote comparison today and find out what you could be saving.