If you own a free standing home in Kowen, ACT 2620, you're likely no stranger to the challenge of finding the right home insurance at a fair price. Kowen is a semi-rural locality on the eastern fringe of the Australian Capital Territory, characterised by larger blocks, bushland surrounds, and an older housing stock — all of which play a meaningful role in how insurers price your risk. This article breaks down a real home and contents insurance quote for a 3-bedroom, 1-bathroom free standing home in Kowen, and puts the numbers in context so you can make a more informed decision.

---

Is This Quote Fair?

The quote in question comes in at $2,447 per year (or $239/month) for combined home and contents cover, with a building sum insured of $505,000 and contents valued at $50,000. The building excess is $3,000 and the contents excess is $600.

Our price rating for this quote is FAIR — Around Average. That assessment is well supported by the data. The premium sits modestly above the ACT state average of $2,288/yr and the ACT median of $2,186/yr, but it is not an outlier by any stretch. When you factor in the specific characteristics of this property — fibro asbestos walls, stump foundations, a 1966 construction year, and a relatively generous building sum insured of over half a million dollars — a slight premium above the state average is entirely reasonable.

In short, this is not a quote to walk away from in frustration, but it is also worth understanding what's driving the price before simply accepting it.

---

How Kowen Compares

Putting this quote into a broader pricing context is useful for any homeowner doing their research. Here's how the numbers stack up:

| Benchmark | Premium |

|---|---|

| This quote | $2,447/yr |

| ACT average | $2,288/yr |

| ACT median | $2,186/yr |

| Snowy Monaro LGA average | $2,328/yr |

| National average | $5,347/yr |

| National median | $2,764/yr |

A few things stand out immediately. First, this quote is well below the national average of $5,347/yr — by more than $2,900. That's a significant saving compared to what homeowners in higher-risk parts of Australia (think cyclone-prone Queensland or flood-affected regional NSW) are paying. Second, the quote tracks closely with the Snowy Monaro LGA average of $2,328/yr, which is the most geographically relevant benchmark given Kowen's position on the ACT/NSW border.

The modest premium above the ACT state figures is consistent with what you'd expect for a property with some age-related and construction-related risk factors (more on those below). For a deeper look at how premiums trend across the territory, visit the ACT home insurance stats page, or explore Kowen-specific data as it becomes available. You can also benchmark against national home insurance trends if you're curious about the bigger picture.

---

Property Features That Affect Your Premium

Understanding how insurers view your property is one of the most empowering things you can do as a homeowner. Several features of this particular property are worth examining closely.

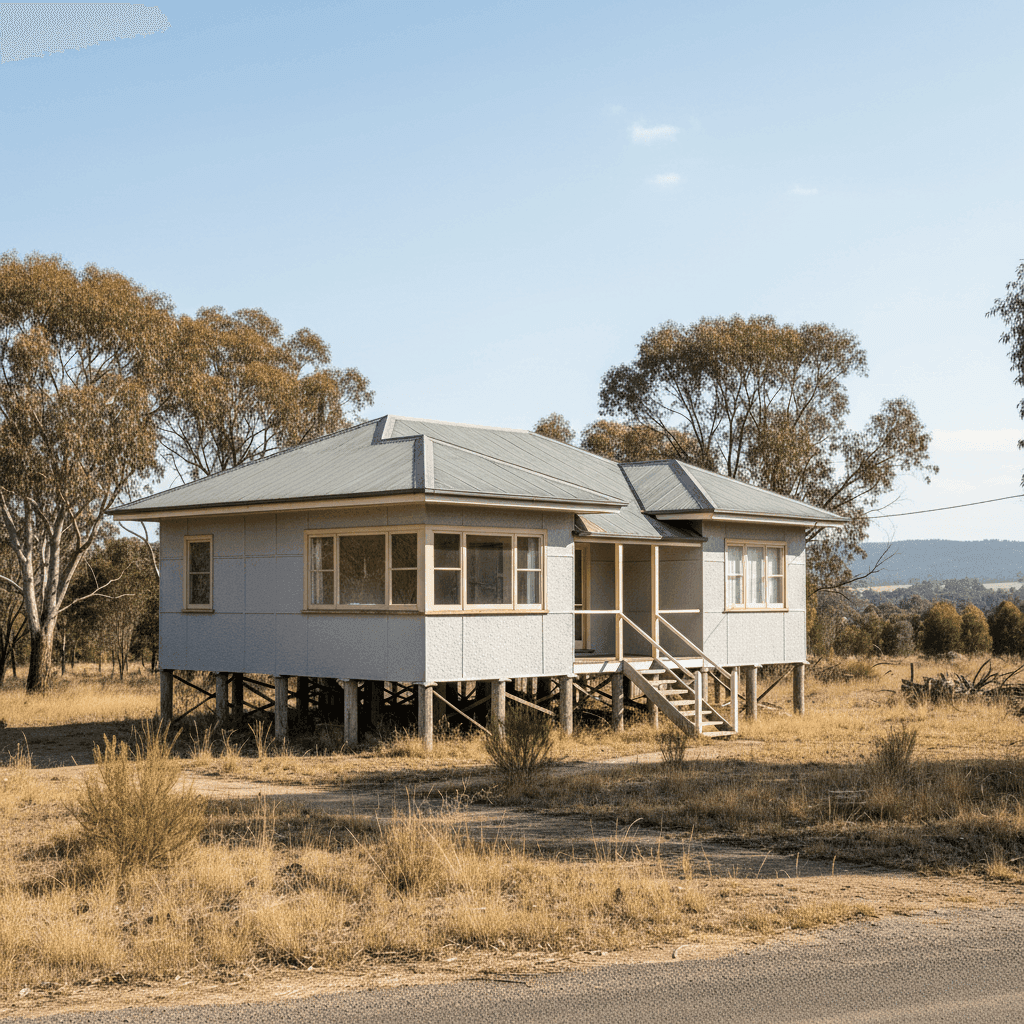

Fibro Asbestos Walls

This is arguably the most significant risk factor in this quote. Homes with fibro asbestos cladding — common in Australian homes built before the mid-1980s — attract higher premiums because of the cost and complexity involved in repairs or rebuilding. Any damage that disturbs asbestos-containing materials requires licensed removal and disposal, which adds substantially to claim costs. Insurers price this risk accordingly.

Construction Year (1966)

A home built in 1966 is now approaching 60 years old. Older homes can have ageing electrical wiring, plumbing, and structural elements that increase the likelihood and cost of claims. Some insurers apply age-based loadings, particularly once a property passes the 40–50 year mark.

Stump Foundations

Homes on stumps (also called pier or post foundations) are common in older Australian builds. While stumps provide good ventilation and can be practical on uneven terrain, they can deteriorate over time and may require periodic inspection and replacement. This adds a layer of risk that insurers consider.

Steel/Colorbond Roof

On the positive side, a steel Colorbond roof is generally viewed favourably by insurers. It's durable, fire-resistant, and handles hail and wind better than many tile alternatives. This likely helps moderate the premium compared to what it might otherwise be.

Elevated Less Than 1m

The slight elevation of this home is a minor factor, but it can assist with drainage and reduce flood risk at the ground level — a marginal positive in the insurer's eyes.

Building Size and Sum Insured

At 214 sqm with a building sum insured of $505,000, this is a solidly insured property. Getting the sum insured right is critical — underinsurance is one of the most common and costly mistakes Australian homeowners make. At roughly $2,360 per sqm, this figure is in a reasonable range for ACT, though it's worth periodically reviewing whether it reflects current rebuild costs.

---

Tips for Homeowners in Kowen

Whether you're reviewing an existing policy or shopping for the first time, here are four practical steps worth considering.

1. Get an asbestos assessment if you haven't already. If your home has fibro asbestos cladding and you haven't had a professional assessment, it's worth organising one. Knowing the condition and extent of asbestos in your home helps you understand your risk — and may be relevant information for your insurer.

2. Review your building sum insured annually. Construction costs have risen significantly in recent years. The cost to rebuild your home today may be higher than it was when you first took out your policy. Use a building cost calculator or speak to a quantity surveyor to make sure your sum insured keeps pace with reality.

3. Consider your excess carefully. This quote carries a $3,000 building excess — on the higher end of the spectrum. A higher excess typically lowers your premium, but it means more out-of-pocket cost when you claim. Think about what you could comfortably afford in the event of a loss, and adjust accordingly.

4. Compare quotes before renewing. Insurers don't always reward loyalty with competitive pricing. Even if your current insurer has treated you well, it costs nothing to compare alternatives at renewal time. You may find equivalent or better cover at a lower price.

---

Ready to Compare Home Insurance in Kowen?

Whether this quote is your current policy or one you're evaluating, the best way to know if you're getting value is to compare. At CoverClub, we make it easy to see how different insurers price your specific property — no guesswork, no jargon. Get a home insurance quote today and find out if you could be paying less for the same level of protection.