Kurrajong is a picturesque semi-rural suburb nestled in the Hawkesbury region of New South Wales, known for its leafy acreage properties and relaxed lifestyle just 65 kilometres north-west of Sydney. For owners of larger free standing homes in this area, getting the right home and contents insurance — and understanding whether you're paying a fair price — is an important part of protecting what is likely your most significant asset.

This article breaks down a recent home and contents insurance quote for a five-bedroom, two-bathroom free standing home in Kurrajong (postcode 2758), compares it against local, state and national benchmarks, and offers practical tips to help you make the most of your cover.

---

Is This Quote Fair?

The annual premium for this property came in at $3,450 per year (or $324/month), covering a building sum insured of $1,208,000 and contents valued at $125,000. Both the building and contents excess are set at $2,000.

Our pricing analysis rates this quote as Fair — Around Average. That means the premium sits comfortably within a normal range for the area — not the cheapest on the market, but certainly not an outlier on the high end either. For a property of this size and specification, a "fair" rating is a reasonable outcome, though it's always worth exploring whether a better deal exists.

To put it in context: the suburb average for Kurrajong sits at $4,742/year, meaning this quote comes in roughly $1,292 below the local average — a meaningful saving. It also falls below the suburb median of $4,175/year, placing it in the lower half of the local pricing distribution. Only the suburb's 25th percentile (the cheapest quarter of quotes) comes in lower, at $3,239/year.

---

How Kurrajong Compares

Kurrajong is notably more expensive to insure than both the state and national norms, which is important context for any homeowner in the area.

| Benchmark | Average Premium | Median Premium |

|---|---|---|

| Kurrajong (2758) | $4,742/yr | $4,175/yr |

| NSW State | $3,801/yr | $3,410/yr |

| National | $2,965/yr | $2,716/yr |

| Lithgow LGA | $5,454/yr | — |

Compared to the NSW state average of $3,801/year, Kurrajong premiums run about 25% higher. Against the national average of $2,965/year, the gap widens further — local premiums are nearly 60% above what the typical Australian homeowner pays.

Interestingly, the Lithgow LGA average (which encompasses Kurrajong and surrounding areas) is even higher at $5,454/year, suggesting that some neighbouring properties carry significantly elevated risk profiles. This quote, at $3,450/year, compares favourably even within that broader LGA picture.

You can explore more localised pricing data on the Kurrajong suburb stats page, which is based on a sample of 53 quotes from the area.

---

Property Features That Affect Your Premium

Several characteristics of this particular property influence how insurers assess and price the risk. Here's what's most relevant:

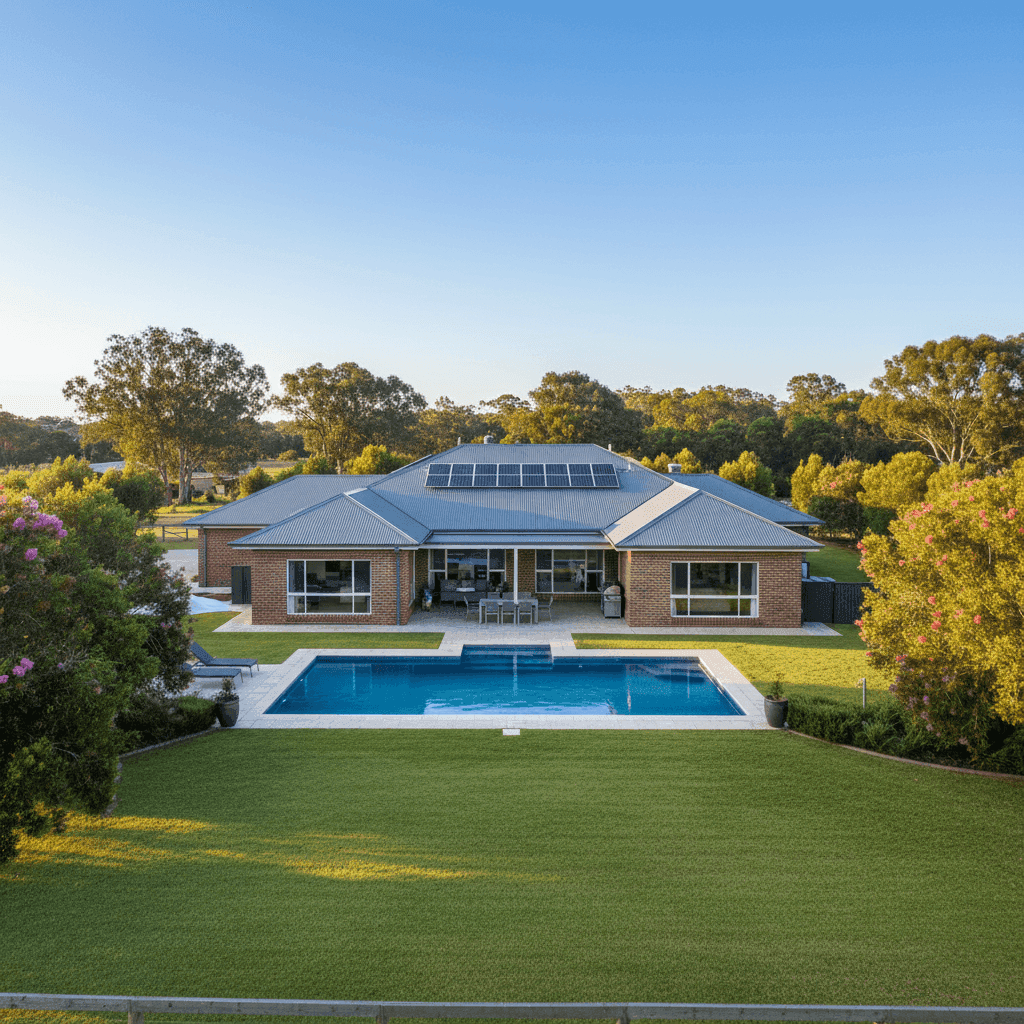

Size and construction (358 sqm, Brick Veneer, Colorbond roof, Slab foundation) At 358 square metres, this is a substantial home, and the building sum insured of $1,208,000 reflects that. Brick veneer construction is generally well-regarded by insurers — it offers solid structural integrity and reasonable fire resistance compared to weatherboard or lightweight cladding. A steel Colorbond roof is durable and low-maintenance, and tends to perform well in storms, which can positively influence premiums. A concrete slab foundation is stable and widely accepted across the industry.

Above average fittings quality The property's above-average fittings — think quality kitchen appliances, premium fixtures and higher-end finishes — push the rebuild cost upward. Insurers factor this into the sum insured calculation, which is why the $1,208,000 building cover is appropriate rather than excessive for a home of this calibre.

Swimming pool A pool adds both value and liability exposure. Most home insurance policies cover the pool structure itself as part of the building, but it's worth confirming your policy includes pool equipment and checking your liability coverage in case of accidents.

Solar panels Solar panels are increasingly common in NSW, but they do add complexity to a claim. Panels can be damaged in hailstorms or by fallen branches, and their replacement cost should be factored into your building sum insured. Confirm with your insurer that panels are explicitly covered under your policy.

Ducted climate control Ducted air conditioning systems are a significant fixed asset and are typically covered under building insurance. Given the system's value, it's worth ensuring your sum insured accounts for full replacement cost, not just partial coverage.

Timber and laminate flooring Timber and laminate floors can be costly to repair or replace following water damage or fire. If your contents policy covers floor coverings, double-check the limits — some policies cap this separately.

---

Tips for Homeowners in Kurrajong

1. Review your building sum insured regularly Construction costs have risen sharply in recent years. A sum insured that was accurate two or three years ago may no longer reflect the true cost to rebuild your home. Use a reputable building cost calculator or speak with a quantity surveyor to validate your figure — underinsurance is one of the most common and costly mistakes homeowners make.

2. Confirm your solar panels and pool equipment are covered Not all standard policies automatically extend to solar panel systems or pool pumps and filtration equipment. Ask your insurer directly, and if necessary, request a policy endorsement to ensure these assets are explicitly included.

3. Consider the impact of your excess on your premium This policy carries a $2,000 excess for both building and contents. Opting for a higher excess is one of the most straightforward ways to reduce your annual premium. If you have a financial buffer and are unlikely to make small claims, increasing your excess could yield meaningful savings.

4. Shop around — even a "fair" quote can be beaten A "fair" rating means this quote is reasonable, not necessarily the best available. The spread between the 25th percentile ($3,239/year) and the 75th percentile ($5,310/year) in Kurrajong is wide, which means there's genuine variation in what insurers will charge for similar properties. Comparing multiple quotes costs nothing and could save hundreds of dollars annually.

---

Compare Home Insurance Quotes in Kurrajong

Whether you're renewing your existing policy or shopping for cover on a new property, comparing quotes is the single most effective way to ensure you're not overpaying. CoverClub makes it easy to see real premiums from multiple insurers side by side, tailored to your specific property. Get a home insurance quote today and find out where your premium sits relative to your neighbours.