If you own or are looking to insure a townhouse in Labrador, QLD 4215, you're probably wondering whether you're getting a fair deal on your home and contents insurance. Labrador sits on the northern fringe of the Gold Coast, a suburb that blends coastal lifestyle with suburban convenience — but like much of South East Queensland, it comes with its own set of insurance considerations. This article breaks down a real home and contents insurance quote for a three-bedroom townhouse in the area, benchmarks it against local, state, and national data, and offers practical tips to help you make the most of your cover.

---

Is This Quote Fair?

The quote in question comes in at $2,119 per year (or roughly $203 per month) for a combined home and contents policy, covering a building sum insured of $505,000 and contents valued at $50,000, each with a $1,000 excess.

Our price rating for this quote is CHEAP — below average for the Labrador area. That's a meaningful finding. With a suburb median of $2,876 per year, this quote sits comfortably beneath the midpoint, and it also falls below the suburb's 25th percentile of $2,261 per year — meaning it's among the more competitively priced quotes seen in this postcode.

In plain terms: if you received this quote, you're doing better than most of your neighbours. That said, "cheap" doesn't always mean "right" — it's still worth checking that your cover levels are appropriate for your property and circumstances.

---

How Labrador Compares

To put this quote in proper context, here's how Labrador stacks up against broader benchmarks:

| Benchmark | Annual Premium |

|---|---|

| This Quote | $2,119 |

| Labrador Suburb Median | $2,876 |

| Labrador Suburb Average | $53,896* |

| Gold Coast LGA Average | $8,161 |

| QLD State Median | $3,903 |

| QLD State Average | $9,129 |

| National Median | $2,764 |

| National Average | $5,347 |

\The suburb average is significantly skewed by high-value outlier properties in the sample of 20 quotes — the median is a far more reliable indicator for typical homes.*

What stands out here is that this quote also beats the national median of $2,764, which is a strong result. Queensland homeowners generally pay more than the national median — the state median of $3,903 reflects the elevated risk profile of many QLD postcodes, driven by weather events, flooding, and storm damage. The fact that this Labrador townhouse comes in well below both state and national medians is notable.

You can explore more data for this area on our Labrador suburb stats page, compare it against Queensland-wide insurance data, or check out national home insurance benchmarks.

---

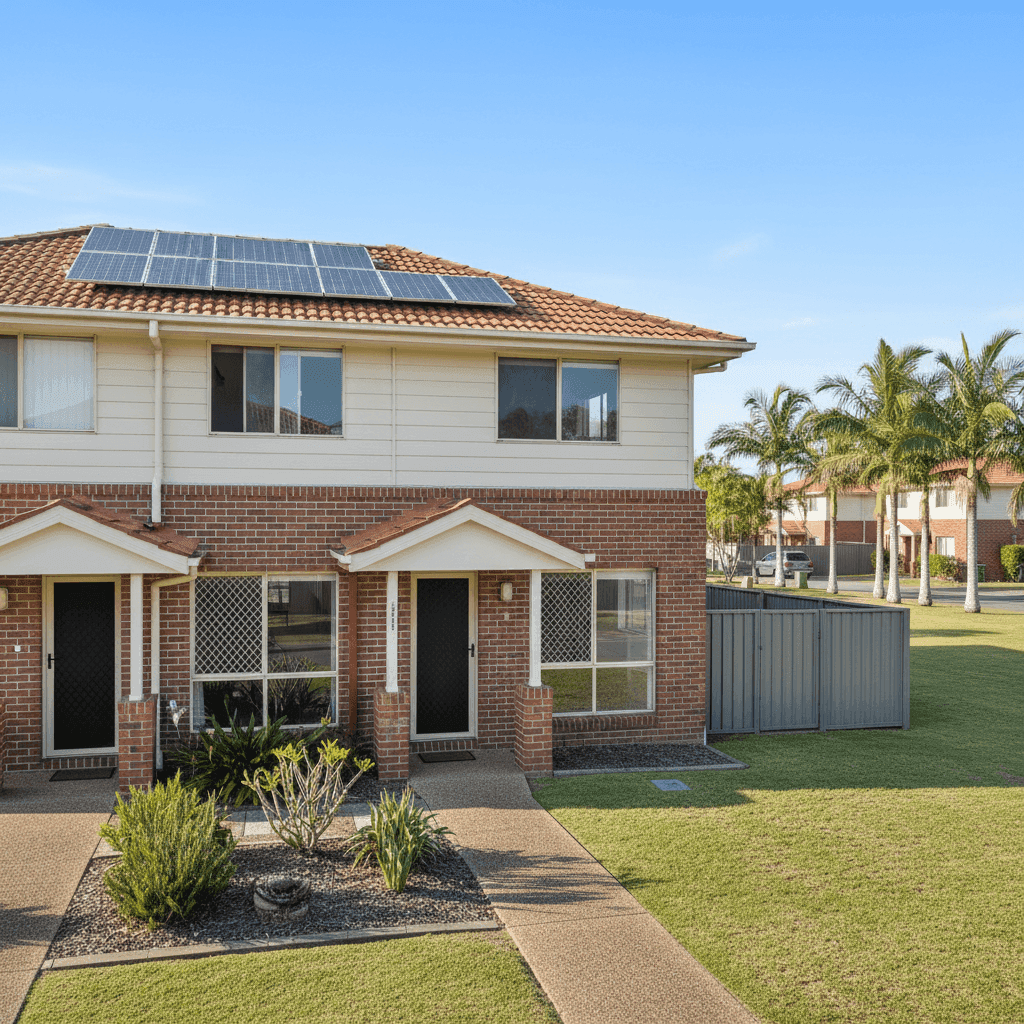

Property Features That Affect Your Premium

Several characteristics of this particular townhouse influence where the premium lands — and why it may be on the lower end of the scale.

Construction: Brick Veneer Walls & Tiled Roof

Brick veneer is generally viewed favourably by insurers. It offers solid fire resistance and structural durability compared to lightweight cladding materials, which can translate into lower premiums. A tiled roof similarly signals longevity and weather resilience, though tiles can be more costly to repair after hail events. Overall, this construction combination is considered relatively low-risk.

Slab Foundation

A concrete slab foundation is standard for Queensland homes of this era and is generally well-regarded by insurers. Unlike raised timber stumps, slabs are less susceptible to subfloor moisture issues and termite ingress, which can reduce the likelihood of structural claims.

Built in 1992

At just over 30 years old, this townhouse sits in a moderately aged bracket. It's old enough that some building components (roof tiles, plumbing, electrical) may be approaching the end of their service life, but it predates many modern construction standards. Insurers may factor in age-related wear when assessing risk, though a well-maintained 1992 build typically doesn't attract significant loading.

Solar Panels

The presence of solar panels adds a layer of complexity to the insurance picture. Panels are generally covered under building insurance, but they do represent an additional asset — and a potential liability in storm or hail events. It's worth confirming with your insurer that solar panels are explicitly included in your building cover and understanding how they'd be treated in a claim.

Ducted Climate Control

Ducted air conditioning is a meaningful contents or building item depending on how it's installed. Fixed ducted systems are typically treated as part of the building. Their presence can slightly increase replacement costs, which may influence the adequacy of your sum insured.

Body Corporate / Strata Property

As a strata property, the body corporate likely holds a separate insurance policy covering the building's common areas and exterior structure. This means your individual policy may primarily need to cover your lot's internal fixtures, fittings, and contents — though the specifics vary significantly between strata schemes. Always request a copy of the body corporate's Certificate of Currency to understand what's already covered before setting your own building sum insured.

No Cyclone Risk

Labrador falls outside the designated cyclone risk zone, which is a meaningful premium factor in Queensland. Properties in cyclone-prone areas (generally north of the Tropic of Capricorn) can attract significant loading. Being south of this threshold helps keep premiums more manageable.

---

Tips for Homeowners in Labrador

1. Review Your Strata Cover Carefully

Don't assume your body corporate's policy covers everything inside your townhouse. Request the strata policy details and identify any gaps — particularly around internal fixtures, flooring (vinyl in this case), and improvements you've made to the property. Your individual policy should complement, not duplicate, the strata cover.

2. Check Your Solar Panel Coverage

Confirm in writing that your solar panels are covered under your building policy and understand the basis of settlement (new for old vs. indemnity). Given Queensland's storm season, this is not a detail to leave to chance.

3. Don't Set and Forget Your Sum Insured

Building costs have risen sharply across Australia in recent years. A sum insured of $505,000 may have been appropriate at the time of the quote, but it's worth revisiting annually. Underinsurance is one of the most common — and costly — mistakes homeowners make. Use a building cost calculator or speak with a quantity surveyor if you're unsure.

4. Compare at Renewal Time

Even if this quote is competitively priced today, premiums can shift significantly at renewal. Insurers regularly re-price their books, and loyalty doesn't always pay. Set a reminder to compare quotes before your renewal date each year — a few minutes of effort can save hundreds of dollars.

---

Ready to Compare Your Own Quote?

Whether you're insuring a townhouse in Labrador or a property anywhere else in Australia, CoverClub makes it easy to see how your premium stacks up. Get a quote today and find out if you're paying a fair price — or if there's a better deal waiting for you.