Langwarrin is a well-established suburb on the Mornington Peninsula fringe, sitting within the City of Frankston in Victoria's south-east. Known for its leafy streets, spacious blocks, and family-friendly atmosphere, it's the kind of suburb where a solid, freestanding home is the norm rather than the exception. If you own a three-bedroom, double brick home here, you're probably wondering whether your home and contents insurance is giving you fair value — or whether there's a better deal waiting to be found.

This article breaks down a real insurance quote for exactly this type of property in Langwarrin, comparing it against local, state, and national benchmarks so you can make a more informed decision at renewal time.

---

Is This Quote Fair?

The annual premium for this quote comes in at $1,898 per year (or $182/month), covering a building sum insured of $504,000 and contents valued at $220,000 — both with a $1,000 excess. Our pricing analysis rates this quote as FAIR (Around Average).

That rating reflects a premium that sits comfortably in the middle of the market — not the cheapest available, but certainly not overpriced either. For a combined home and contents policy with a solid level of cover, landing near the median is a reasonable outcome, particularly in a suburb where premiums can vary quite significantly depending on the insurer and the specifics of the property.

It's worth noting that "fair" doesn't mean you can't do better. Even a modest saving of $200–$300 per year adds up meaningfully over time, and the competitive nature of the Australian home insurance market means comparison shopping is always worthwhile.

---

How Langwarrin Compares

To put this quote in context, here's how it stacks up against suburb, state, and national data:

| Benchmark | Premium |

|---|---|

| This Quote | $1,898/yr |

| Langwarrin suburb median | $2,007/yr |

| Langwarrin suburb average | $2,826/yr |

| Langwarrin 25th percentile | $1,545/yr |

| Langwarrin 75th percentile | $3,161/yr |

| LGA (Frankston) average | $3,283/yr |

| VIC state median | $2,718/yr |

| VIC state average | $3,000/yr |

| National average | $5,347/yr |

| National median | $2,764/yr |

You can explore the full Langwarrin suburb insurance stats and Victoria-wide data on CoverClub.

A few things stand out from this data. First, this quote at $1,898 sits below the suburb median of $2,007 and well below the suburb average of $2,826 — a positive sign. It also comfortably beats the Frankston LGA average of $3,283, which suggests the insurer has priced this property favourably relative to the broader local government area.

Compared to Victoria as a whole, the quote again comes in below both the state median and average — a good result. And when measured against national figures, the difference is striking: the national average of $5,347 is nearly three times this quote, reflecting just how much premiums vary across Australia, particularly in high-risk regions like cyclone-prone Queensland and flood-affected parts of New South Wales.

The spread within Langwarrin itself is also worth highlighting. With a 25th percentile of $1,545 and a 75th percentile of $3,161, there's more than $1,600 separating the cheapest quarter of quotes from the most expensive. That's a significant range based on 70 quotes — and it underscores why comparing multiple insurers matters so much.

---

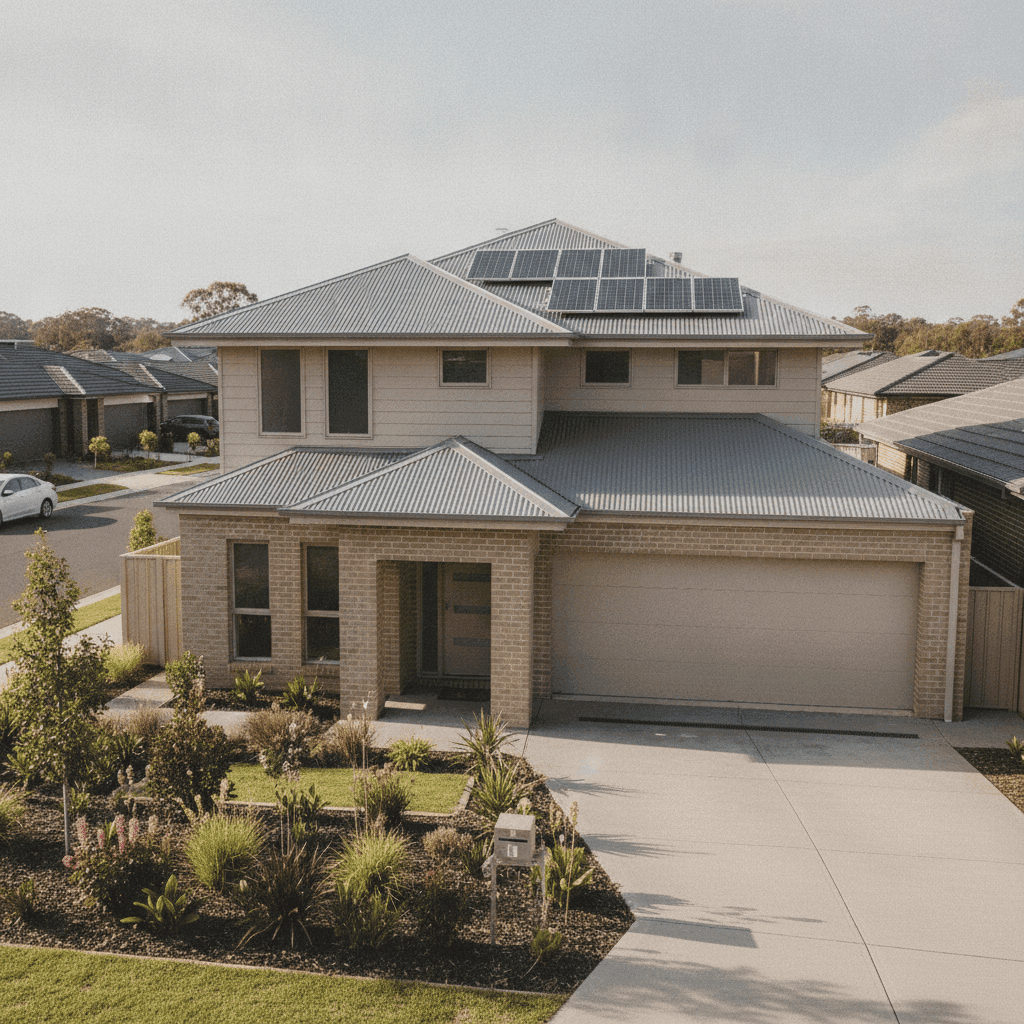

Property Features That Affect Your Premium

Several characteristics of this Langwarrin property influence how insurers price the risk — and in this case, most of them work in the homeowner's favour.

Double brick construction is generally viewed positively by insurers. It's durable, fire-resistant, and less susceptible to storm and wind damage than timber-framed alternatives. Homes built with double brick typically attract more competitive premiums, and this property is no exception.

Steel/Colorbond roofing is another tick in the right column. Colorbond is a popular and well-regarded roofing material in Australia — lightweight, durable, and resistant to corrosion. Insurers tend to rate it favourably compared to older materials like terracotta tiles, which can be heavier and more prone to cracking.

The 1979 construction year places this home in a mature but not ancient bracket. Homes from this era are generally well-built, though insurers may factor in the age of plumbing, electrical systems, and other infrastructure. Keeping these systems well-maintained and up to current standards can help manage your premium over time.

Solar panels are an increasingly common feature on Australian homes, and this property has them. It's important to confirm with your insurer that solar panels are explicitly covered under your policy — either as part of the building sum insured or as a specified item. Coverage terms vary between providers, so this is worth checking carefully.

Ducted climate control adds to the replacement value of the home and is factored into the building sum insured. At $504,000, the building cover appears to be set at a reasonable level for a 139 sqm home in this area, though it's always wise to periodically review your sum insured to ensure it reflects current construction costs.

The slab foundation and standard fittings are both neutral factors — nothing that would push the premium up or down significantly. The absence of a pool also removes a common source of liability risk, which can marginally benefit the overall pricing.

---

Tips for Homeowners in Langwarrin

1. Review your sum insured annually Construction costs in Victoria have risen considerably in recent years. The cost to rebuild a 139 sqm home today may be meaningfully higher than it was even two or three years ago. Use a building cost calculator or speak with a builder to ensure your $504,000 cover is still adequate — being underinsured at claim time can be a costly mistake.

2. Confirm solar panel coverage in writing Solar panel systems can represent a significant investment. Ask your insurer directly whether your panels are covered under the building section of your policy, what events are included (e.g. storm, fire, accidental damage), and whether there are any sub-limits that apply. Don't assume — get it confirmed.

3. Compare quotes at every renewal The $1,600+ spread between the cheapest and most expensive quotes in Langwarrin shows that loyalty to a single insurer doesn't always pay off. Insurers frequently reprice their books, and a quote that was competitive two years ago may no longer be. Set a reminder to compare at least 30 days before your renewal date.

4. Consider your excess level strategically Both the building and contents excess on this policy sit at $1,000. Opting for a higher excess can reduce your annual premium — but only makes sense if you're confident you could comfortably cover that amount in the event of a claim. Run the numbers: if a $500 excess increase saves you $150/year, it takes over three years to break even on a single claim.

---

Ready to See What You Could Save?

Whether you're renewing soon or just curious about what the market looks like, comparing quotes is the smartest first step. CoverClub makes it easy to see real prices from multiple insurers for your specific property — no obligation, no pressure.