Lara is a fast-growing suburb in Victoria's Greater Geelong region, sitting roughly halfway between Melbourne and Geelong along the Princes Freeway. It's popular with families looking for newer, larger homes at relatively affordable prices — and that growth means more homeowners asking an important question: am I paying a fair price for my home insurance?

This article breaks down a real home and contents insurance quote for a four-bedroom, two-bathroom free standing home in Lara (postcode 3212), comparing it against local, state, and national benchmarks to help you understand what's driving the cost — and whether there's room to save.

---

Is This Quote Fair?

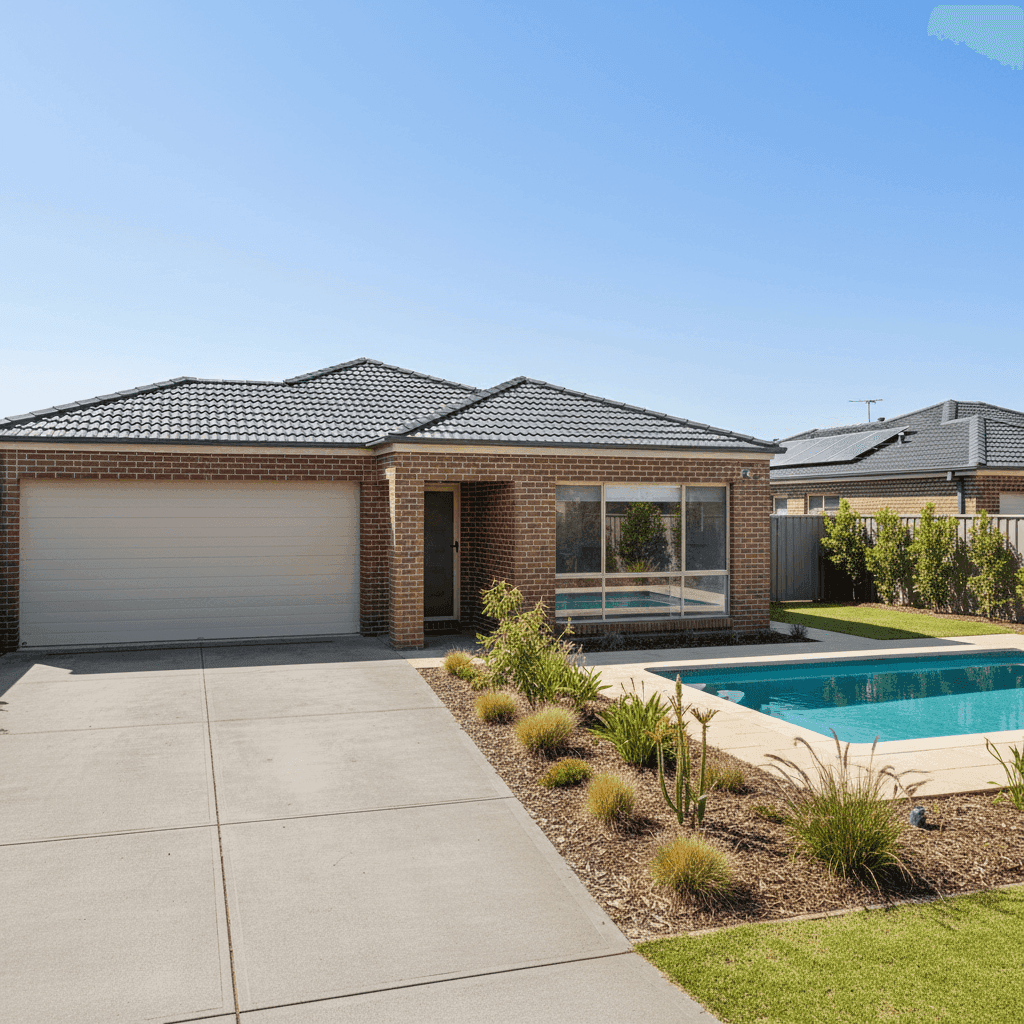

The quote in question sits at $1,947 per year (or $187 per month) for combined home and contents cover, with a building sum insured of $871,500 and contents valued at $150,000. Both the building and contents excess are set at $1,000.

Based on data from CoverClub's Lara suburb stats, this quote is rated Expensive — above average for the area. Here's why:

- The suburb average for Lara is $1,455/yr, and the median is $1,343/yr

- This quote is $492 above the suburb average and $604 above the median

- It sits above the 75th percentile for the suburb, which is $1,765/yr — meaning it's more expensive than roughly three-quarters of comparable quotes in the area

That said, "expensive" doesn't automatically mean "wrong." A higher sum insured, a pool, and ducted climate control all contribute to a larger insurable risk, which naturally pushes premiums up. The key is understanding whether the price reflects genuine risk factors or whether there's an opportunity to shop around.

---

How Lara Compares

One of the most useful ways to evaluate any insurance quote is to zoom out and look at the broader picture. Here's how this quote stacks up across different geographies:

| Benchmark | Annual Premium |

|---|---|

| This Quote | $1,947 |

| Lara Suburb Average | $1,455 |

| Lara Suburb Median | $1,343 |

| Greater Geelong LGA Average | $1,754 |

| VIC State Average | $3,000 |

| VIC State Median | $2,718 |

| National Average | $5,347 |

| National Median | $2,764 |

(Based on 122 quotes sampled in the Lara area. Source: [CoverClub VIC stats](https://coverclub.com.au/stats/VIC) and [national stats](https://coverclub.com.au/stats/national))

The contrast with state and national figures is striking. At $1,947, this quote is well below the Victorian state average of $3,000 and dramatically lower than the national average of $5,347 — a figure heavily influenced by high-risk regions in Queensland, Western Australia, and the Northern Territory where cyclone, flood, and storm damage are far more prevalent.

Within Victoria, Lara is considered a relatively low-risk postcode. It's not in a cyclone zone, and while parts of Greater Geelong can experience bushfire risk, Lara itself sits in a more suburban corridor. This helps keep premiums comparatively modest by national standards, even if this particular quote is on the higher end locally.

---

Property Features That Affect Your Premium

Several characteristics of this property directly influence what insurers charge. Understanding these can help you have more informed conversations when comparing policies.

Building size and sum insured At 367 sqm and a building sum insured of $871,500, this is a substantial home. Larger homes cost more to rebuild, and insurers price accordingly. It's worth periodically checking that your sum insured reflects current construction costs — both under-insuring and over-insuring carry their own risks.

Brick veneer construction and tiled roof This combination is generally viewed favourably by insurers. Brick veneer offers solid fire resistance, and tiled roofs are durable and less susceptible to storm damage than some alternatives (such as Colorbond in certain hail-prone areas). These features can work in your favour when it comes to pricing.

Slab foundation A concrete slab is a standard, low-risk foundation type for modern Australian homes. It doesn't attract the same concerns as older stumped or suspended timber floors, which can be more vulnerable to moisture and movement.

Swimming pool Pools add to the insurable value of a property and introduce additional liability considerations. Most home and contents policies cover the pool structure under building cover, but it's worth confirming exactly what's included — particularly for pool equipment, fencing, and any liability for third-party injury.

Ducted climate control Ducted heating and cooling systems are a significant fixed asset. They're covered under building insurance as a permanent fixture, but their replacement cost contributes to the overall sum insured. A quality ducted system in a 367 sqm home can easily cost $15,000–$25,000 to replace, so it's important this is factored into your building sum insured.

Construction year: 2015 A home built in 2015 is relatively modern and likely complies with contemporary Australian building codes, including energy efficiency and structural standards. Newer homes generally attract slightly lower premiums than older properties, which may have ageing wiring, plumbing, or roofing.

---

Tips for Homeowners in Lara

Whether you're reviewing an existing policy or shopping for the first time, here are some practical steps to make sure you're getting the right cover at a competitive price.

1. Shop around — especially if you're above the 75th percentile If your quote is above the local 75th percentile, it's a strong signal to compare alternatives. Insurers use different pricing models, and the same property can attract meaningfully different premiums across providers. Use a comparison tool like CoverClub to see multiple quotes side by side.

2. Review your sum insured annually Construction costs in Victoria have risen significantly in recent years. The cost to rebuild a 367 sqm brick veneer home today may be higher than it was even two or three years ago. Underinsurance is a common and costly mistake — make sure your building sum insured keeps pace with current rebuild costs.

3. Check what's covered for your pool Not all policies treat pool infrastructure the same way. Confirm whether your policy covers the pool shell, pump, filtration equipment, and safety fencing under building cover — and review any liability provisions that apply to guests or neighbours.

4. Consider your excess strategically Both the building and contents excess on this quote are set at $1,000. Opting for a higher excess (say, $2,500 or $5,000) can meaningfully reduce your annual premium. If you have a strong emergency fund and wouldn't claim for smaller incidents, a higher excess can be a smart way to lower ongoing costs.

---

Compare Your Options with CoverClub

Whether this quote is the right fit depends on more than just the price — policy inclusions, claim limits, and insurer reputation all matter. The best way to know if you're getting value is to compare. Visit CoverClub to get personalised home and contents quotes for your Lara property, and see how your current premium stacks up against the market in real time.