If you own a free standing home in Learmonth, VIC 3352, you're probably curious whether your home insurance premium is competitive — or whether you're quietly overpaying. This article breaks down a real home and contents insurance quote for a three-bedroom property in the area, compares it against Victorian and national benchmarks, and offers practical tips to help you get the best value cover.

---

Is This Quote Fair?

The annual premium for this quote comes in at $1,594 per year (or approximately $153 per month), covering both building (sum insured: $400,000) and contents ($100,000), each with a $1,000 excess. Our independent price rating classifies this as CHEAP — below average relative to comparable properties.

That's a meaningful result. A "below average" rating doesn't mean the cover is lacking — it means the premium is lower than what most homeowners in similar situations are paying. For a combined home and contents policy with a solid sum insured, paying under $1,600 annually represents genuine value.

It's worth noting that a lower premium should still be scrutinised for what it actually covers. Confirm the policy includes events like storm, fire, accidental damage, and liability, and check whether the building sum insured of $400,000 is sufficient to fully rebuild your home at current construction costs in regional Victoria.

---

How Learmonth Compares

To put this quote in context, here's how it stacks up against broader market data:

| Benchmark | Annual Premium |

|---|---|

| This Quote | $1,594 |

| LGA (Corangamite) Average | $2,766 |

| VIC State Average | $3,000 |

| VIC State Median | $2,718 |

| National Average | $5,347 |

| National Median | $2,764 |

The numbers tell a compelling story. This quote is 42% below the Corangamite LGA average, 47% below the Victorian state average, and a remarkable 70% below the national average. Even measured against the more conservative national median of $2,764, this premium is nearly $1,200 cheaper per year.

It's important to understand why national averages are so elevated — high-risk postcodes in Queensland, Northern Territory, and coastal areas prone to cyclone, flood, and storm surge significantly drag the national figure upward. Still, even within Victoria, this quote sits well below what most homeowners in the state are paying.

You can explore more detailed pricing data for this area at our Learmonth suburb stats page, or browse the broader Victorian home insurance statistics and national home insurance data for further context.

---

Property Features That Affect Your Premium

Insurance pricing is never one-size-fits-all. Insurers assess a range of property characteristics when calculating your premium. Here's how the features of this particular home likely influence its cost:

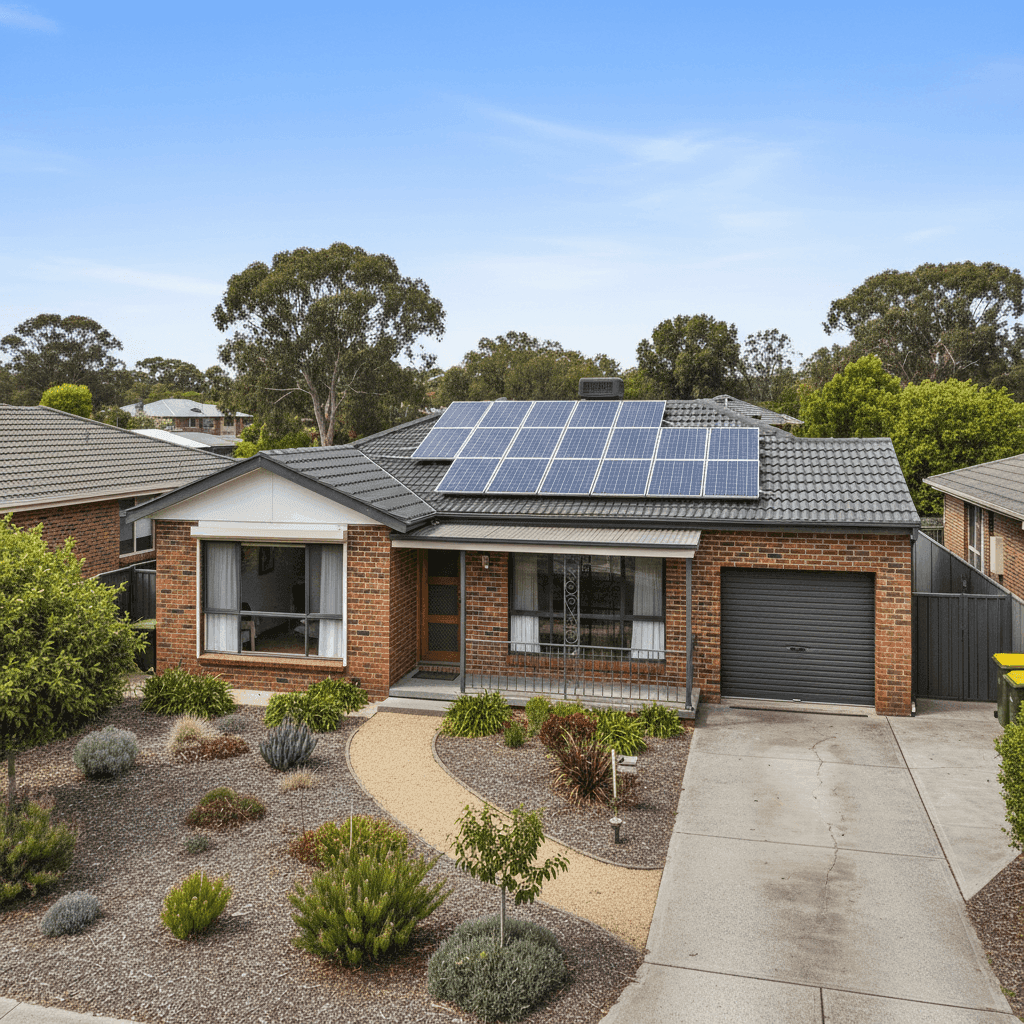

Brick Veneer Walls Brick veneer is one of the most common wall types in Australian homes built from the 1960s onwards, and insurers generally view it favourably. It offers solid fire resistance and structural durability, which can contribute to lower premiums compared to timber-framed or clad exteriors.

Tiled Roof A tiled roof is another positive signal to insurers. Tiles are durable, weather-resistant, and long-lasting when properly maintained. That said, a home built in 1978 means the roof is now approaching 50 years old — regular inspections are worthwhile to ensure no cracked or slipped tiles are creating vulnerability to water ingress.

Concrete Slab Foundation A slab foundation is generally considered low-risk from an insurance perspective. It eliminates the underfloor space that can harbour moisture, pests, or structural issues common in older stumped homes.

Solar Panels This property has solar panels installed, which are typically covered under home and contents policies — but it pays to check. Some insurers include them automatically under the building sum insured; others treat them as an optional add-on. Confirm your policy explicitly covers solar panels for damage from storms, hail, or fire.

Ducted Climate Control Ducted heating and cooling systems are a significant asset and can be costly to replace. Ensure your building sum insured accounts for the full replacement value of the system, particularly in a home of this age where the original system may have been upgraded.

No Pool, No Cyclone Risk Zone The absence of a swimming pool removes a liability risk factor that can add to premiums. Learmonth is also not classified as a cyclone risk area, which keeps the risk profile — and therefore the premium — more manageable than properties in northern Australia.

130 sqm Building Size At 130 square metres, this is a modest but comfortable footprint for a three-bedroom, two-bathroom home. The building sum insured of $400,000 equates to roughly $3,077 per square metre — broadly in line with regional Victorian rebuild costs, though it's always prudent to revisit this figure as construction costs continue to rise.

---

Tips for Homeowners in Learmonth

1. Review your sum insured annually Construction costs in regional Victoria have increased significantly over the past few years. A sum insured that was adequate when you first took out the policy may no longer cover a full rebuild. Use a building cost calculator or speak with a local builder to sense-check your figure before renewal.

2. Confirm solar panel coverage in your policy documents Don't assume your solar panels are covered — read the product disclosure statement (PDS) carefully. Check whether they're included under the building definition, and whether accidental damage is covered alongside storm and fire.

3. Increase your excess to reduce your premium (strategically) Both the building and contents excess on this policy are set at $1,000. If you have a financial buffer and rarely make small claims, opting for a higher excess can meaningfully reduce your annual premium. Just ensure you could comfortably cover that excess if you needed to claim.

4. Bundle building and contents for simplicity and potential savings This policy already combines building and contents cover — a smart move. Having a single insurer for both simplifies the claims process and can sometimes attract a bundling discount. When comparing alternatives, always compare the combined cost rather than looking at building-only quotes.

---

Compare Your Options with CoverClub

Whether you're renewing soon or simply want to know if you're getting a fair deal, CoverClub makes it easy to compare home insurance quotes tailored to your property and location. With pricing benchmarks drawn from real Australian policies, you can see exactly how your premium stacks up — and find better value if it's available. Get a quote today and take the guesswork out of home insurance.