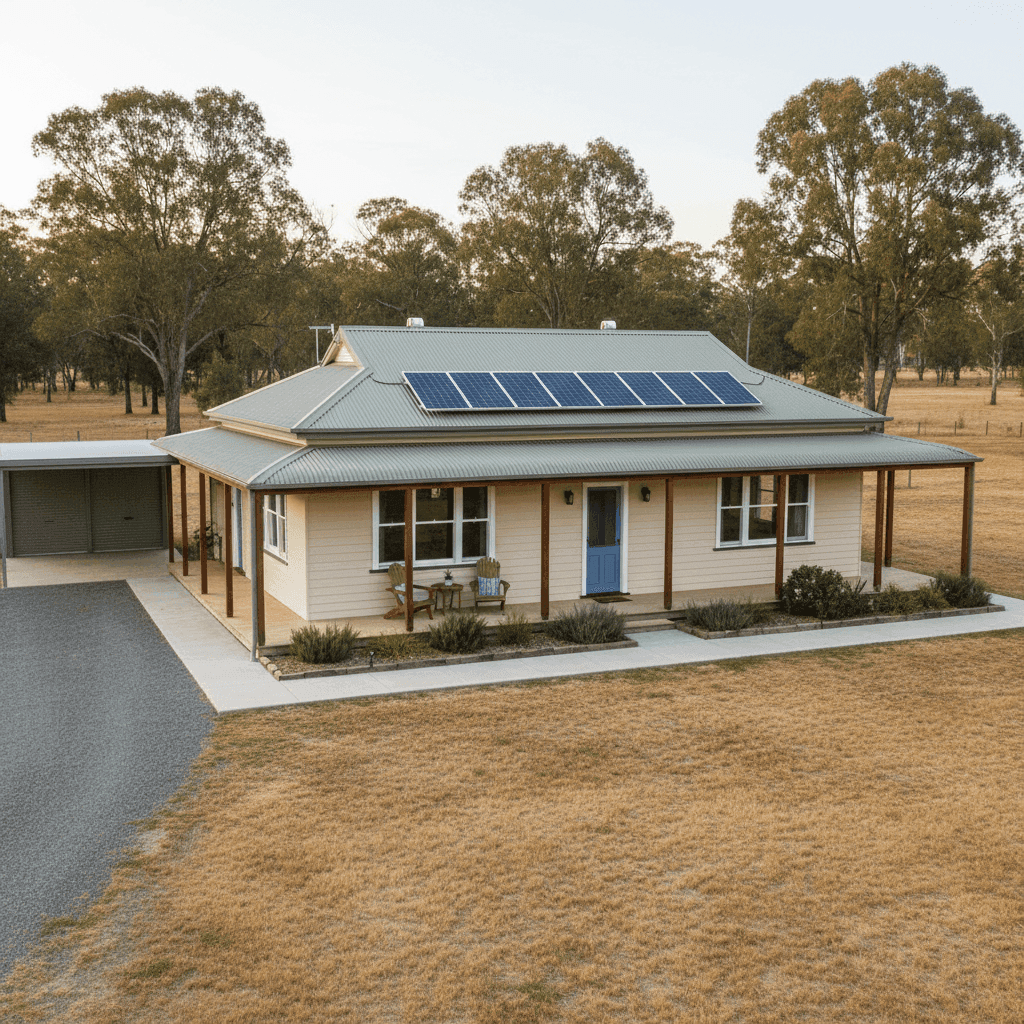

Leyburn is a quiet rural township in Queensland's Southern Downs region, roughly 90 km south-west of Toowoomba. It's the kind of place where properties tend to be spacious, unpretentious, and built to last — and this 3-bedroom, free-standing weatherboard home is a solid example of the local housing stock. If you're a homeowner here wondering whether your insurance premium stacks up, this analysis breaks down a real quote and puts it in context against suburb, state, and national data.

---

Is This Quote Fair?

The annual premium for this property came in at $3,862 per year (or $370/month), covering both building (sum insured: $749,000) and contents ($30,999), each with a $1,000 excess. Our pricing engine has rated this quote as FAIR — around average.

That rating holds up under scrutiny. The suburb average for Leyburn (4365) sits at $5,343/yr, with a median of $4,844/yr. This quote lands comfortably below both figures, and also below the suburb's 75th percentile of $7,008/yr. In fact, at $3,862/yr, this premium is only marginally above the 25th percentile of $3,557/yr — meaning roughly 75% of comparable quotes in this postcode cost more.

So while "fair" might sound like damning with faint praise, in this context it's actually a reasonably competitive result. The homeowner is paying less than the majority of their Leyburn neighbours for equivalent cover.

---

How Leyburn Compares

To properly appreciate this quote, it helps to zoom out and look at the broader picture.

| Benchmark | Premium |

|---|---|

| This quote | $3,862/yr |

| Leyburn suburb average | $5,343/yr |

| Leyburn suburb median | $4,844/yr |

| QLD state average | $9,129/yr |

| QLD state median | $3,903/yr |

| National average | $5,347/yr |

| National median | $2,764/yr |

| Toowoomba LGA average | $2,479/yr |

A few things stand out here. The Queensland state average of $9,129/yr is strikingly high — driven largely by coastal and cyclone-prone postcodes in Far North Queensland, where premiums can be eye-watering. The state median of $3,903/yr is a far more representative figure for inland QLD properties, and this quote sits only slightly above that.

Compared to the national average of $5,347/yr, this quote is notably cheaper. And when measured against the Toowoomba LGA average of just $2,479/yr, it does appear elevated — though it's worth noting that LGA averages can be skewed by a mix of property types, cover levels, and sum insured amounts that may differ significantly from this property.

The bottom line: for a weatherboard home of this age and size in Leyburn, with a building sum insured of $749,000, this premium is broadly in line with what the market is charging.

---

Property Features That Affect Your Premium

Several characteristics of this property will have influenced the final premium. Understanding them can help you make sense of the pricing — and potentially identify ways to adjust.

Weatherboard timber construction is one of the most significant factors. Timber-clad homes are generally considered higher risk than brick or rendered masonry, primarily due to fire susceptibility. Insurers typically price this in, which can push premiums higher compared to equivalent brick homes.

Construction year (1979) means this home is over 45 years old. Older properties can attract higher premiums because ageing electrical wiring, plumbing, and structural components may increase the likelihood of certain claims. Some insurers also apply loading for homes built before certain building code updates.

Steel/Colorbond roofing is generally viewed favourably by insurers. It's durable, resistant to ember attack, and performs well in storms — all of which can help moderate the premium.

Slab foundation is a neutral-to-positive factor in most risk assessments. It's a common and stable foundation type that doesn't carry the same concerns as older stumped or pier-and-beam foundations.

Solar panels add modest replacement value to the building and may slightly increase the sum insured required to cover them adequately. It's worth confirming with your insurer that your solar system is explicitly covered under the building policy.

Ducted climate control is another feature that adds to the replacement cost of the home. These systems can be expensive to repair or replace, and their inclusion in the building sum insured is important to verify.

No pool and no cyclone risk both work in this property's favour. Pool liability and cyclone-related structural cover are two areas that can significantly inflate premiums in Queensland, so their absence here is a meaningful cost saving.

---

Tips for Homeowners in Leyburn

1. Review your building sum insured regularly A sum insured of $749,000 for a 130 sqm weatherboard home is on the higher end. While it's always better to be adequately covered than underinsured, it's worth using a building cost calculator (many insurers offer these) to confirm the figure reflects current construction costs in the Southern Downs region. Overinsuring unnecessarily increases your premium.

2. Compare quotes before renewal With only 19 quotes in the Leyburn suburb sample, the local data set is relatively small — which means there can be meaningful variation between insurers. Don't let your policy auto-renew without shopping around. A few minutes comparing quotes could save you hundreds of dollars annually.

3. Ask about timber home discounts or mitigation credits Some insurers offer discounts for fire mitigation measures on timber homes, such as ember guards, metal mesh on vents, or maintained firebreaks. Given Leyburn's rural setting, it's worth asking your insurer whether any of these measures could reduce your premium.

4. Check your contents cover is right-sized A contents value of $30,999 is relatively modest. Take a quick inventory of your belongings — furniture, appliances, electronics, clothing, and valuables — to make sure this figure is realistic. Being underinsured on contents is a common and costly mistake that only becomes apparent at claim time.

---

Ready to Find a Better Deal?

Whether you're reviewing an existing policy or insuring for the first time, comparing quotes is the single most effective way to make sure you're not overpaying. Get a home insurance quote through CoverClub and see how multiple insurers price your specific property — it's free, fast, and could save you a significant amount each year.