If you own a free standing home in Lloyd, NSW 2650, you're likely wondering whether what you're paying for home insurance is reasonable — or whether you could be doing better. This article breaks down a real home and contents insurance quote for a four-bedroom, two-bathroom brick veneer home in Lloyd, compares it against local, state, and national benchmarks, and offers practical tips to help you get the most out of your cover.

---

Is This Quote Fair?

The quote in question comes in at $2,467 per year (or $236 per month) for combined home and contents insurance, with a building sum insured of $720,000 and contents valued at $150,000. Both the building and contents excess are set at $1,000.

Our price rating for this quote is FAIR — Around Average, and the data backs that up. The suburb average premium for Lloyd sits at $2,375 per year, meaning this quote is only about $92 above what most Lloyd homeowners are paying. That's a difference of less than 4%, which is well within the normal variation you'd expect between insurers.

It's worth noting that the suburb median is actually a little higher at $2,755 per year, which means roughly half of Lloyd homeowners with similar properties are paying more than this quote. Sitting below the median is a solid position to be in.

The 25th to 75th percentile range for Lloyd premiums spans $1,156 to $3,313 per year — a wide spread that reflects the variation between different insurers, property characteristics, and cover levels. At $2,467, this quote lands comfortably in the middle of that range, reinforcing the "fair" rating.

---

How Lloyd Compares

To put Lloyd's premiums in broader context, it helps to look at how the suburb stacks up against the rest of New South Wales and the national picture. You can explore the full data on the Lloyd suburb stats page, the NSW state stats page, and the national stats page.

| Benchmark | Average Premium | Median Premium |

|---|---|---|

| Lloyd (suburb) | $2,375/yr | $2,755/yr |

| LGA (Narrandera) | $2,038/yr | — |

| NSW (state) | $9,528/yr | $3,770/yr |

| National | $5,347/yr | $2,764/yr |

A few things stand out here. The NSW state average of $9,528 per year looks alarming at first glance, but averages can be heavily skewed by high-value properties in expensive Sydney suburbs and coastal areas with elevated flood or storm risk. The NSW median of $3,770 is a more representative figure — and Lloyd's median of $2,755 sits well below it, suggesting the suburb is a relatively affordable place to insure a home.

Compared to the national median of $2,764, Lloyd is essentially on par. This quote of $2,467 actually comes in below the national median, which is encouraging. The LGA average for Narrandera of $2,038 is the lowest benchmark in the comparison, though LGA averages can include a broader mix of property types and cover levels that may differ from this specific home.

Overall, Lloyd homeowners appear to benefit from lower-than-average insurance costs compared to much of NSW — a meaningful advantage worth keeping in mind when budgeting.

---

Property Features That Affect Your Premium

Every home is different, and insurers weigh up a range of property characteristics when calculating a premium. Here's how the key features of this particular property are likely influencing the quote:

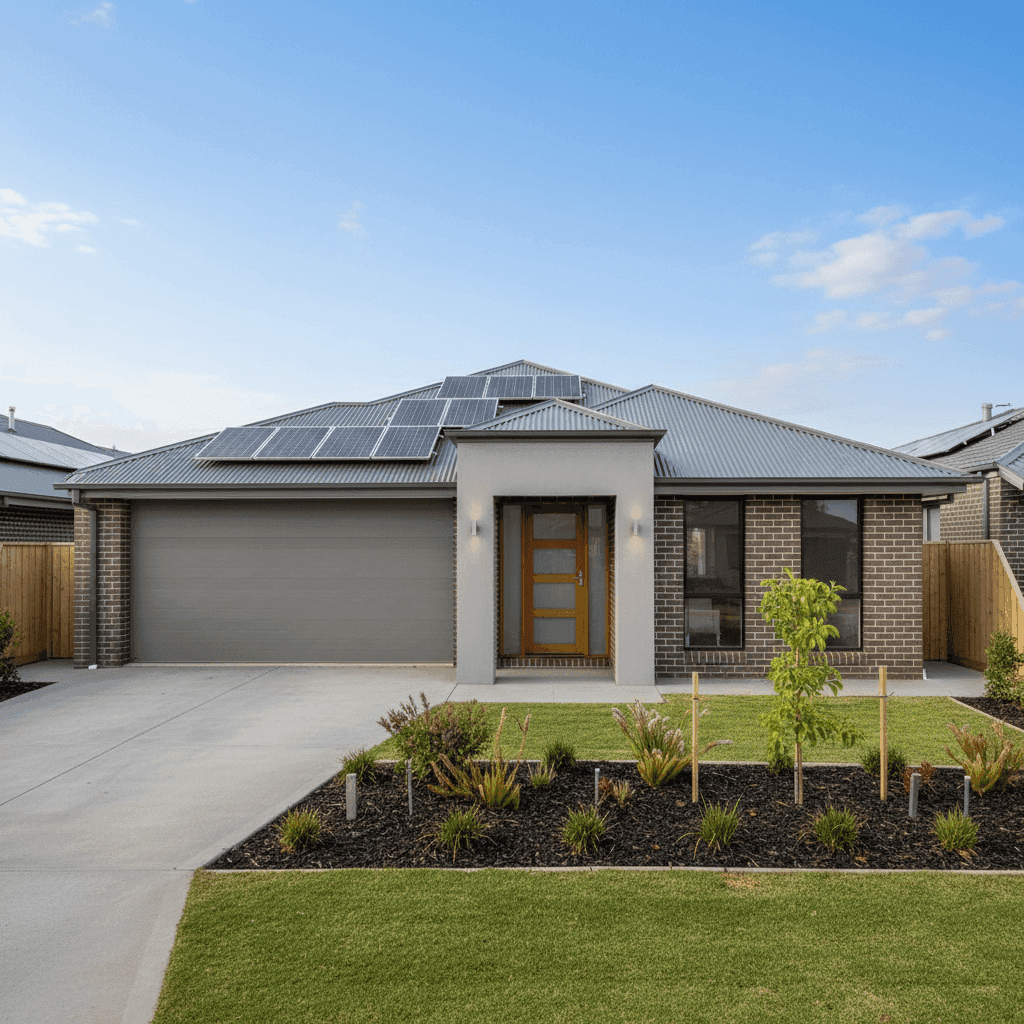

Brick Veneer Walls & Colorbond Roof Brick veneer is one of the most common and well-regarded wall materials in Australian residential construction. It offers good fire resistance and structural durability, which insurers tend to view favourably. The steel Colorbond roof is similarly well-regarded — it's lightweight, resistant to corrosion, and performs well in high-wind conditions. Together, these materials contribute to a lower risk profile compared to, say, timber-framed weatherboard construction.

Slab Foundation & Tiled Flooring A concrete slab foundation is standard for modern builds and generally poses fewer risks than older pier-and-beam or strip footings. Tiled flooring is durable, water-resistant, and less susceptible to damage from minor flooding or moisture — another factor that can work in your favour at claim time.

Construction Year: 2017 At just a few years old, this home was built to modern Australian building codes, which incorporate improved standards for structural integrity, fire safety, and energy efficiency. Newer homes tend to attract lower premiums because they're less likely to have ageing infrastructure issues like outdated wiring or deteriorating plumbing.

Above-Average Fittings Quality The above-average fittings rating signals higher-quality fixtures, finishes, and appliances throughout the home. While this can increase the cost to rebuild or repair — and therefore the building sum insured — it's appropriately reflected in the $720,000 cover amount rather than inflating the premium unnecessarily.

Solar Panels & Ducted Climate Control Solar panels are increasingly common on Australian homes and are generally covered under a standard home insurance policy as a fixed fixture. However, it's worth confirming with your insurer that your panels are explicitly included in the building sum insured. Ducted climate control is a significant built-in system, and again, ensuring it's captured in your rebuild cost estimate is important.

No Pool, No Cyclone Risk The absence of a swimming pool removes a common source of liability and property claims. And being located outside a cyclone risk zone means this home avoids the significant premium loadings that apply to properties in northern Queensland and other high-risk coastal areas.

---

Tips for Homeowners in Lloyd

1. Review your sum insured regularly Building costs have risen significantly across Australia in recent years. A $720,000 sum insured may have been accurate at the time of the quote, but it's worth checking whether it still reflects the true cost to rebuild your home from scratch — including demolition, professional fees, and current labour and material rates. Underinsurance is one of the most common and costly mistakes homeowners make.

2. Confirm solar panels are covered If you have solar panels (as this property does), ask your insurer specifically whether they're included in the building cover and to what value. Some policies cover them automatically; others may require them to be listed separately or have sub-limits that apply.

3. Compare quotes before renewal The 25th percentile for Lloyd premiums is $1,156 per year — significantly lower than this quote. While a cheaper policy may not offer the same level of cover, it's always worth shopping around at renewal time. CoverClub makes it easy to compare multiple quotes side by side so you can weigh up price against features.

4. Consider your excess carefully Both the building and contents excess on this policy are set at $1,000. Opting for a higher excess (say, $1,500 or $2,000) can reduce your annual premium, which may make sense if you have a healthy emergency fund and are unlikely to make small claims. Conversely, if cash flow is a concern, a lower excess might be worth the slightly higher premium.

---

Compare Your Home Insurance on CoverClub

Whether you're a first-time buyer or a long-term Lloyd local, it pays to make sure your home insurance is working as hard as you are. CoverClub lets you compare home and contents quotes from a range of Australian insurers in minutes — so you can see exactly where your current premium sits and whether there's a better deal available.

Get a home insurance quote today and find out how much you could save.