If you own a free standing home in Long Jetty, NSW 2261, you'll know that the Central Coast has a lot going for it — beach proximity, a relaxed lifestyle, and a tight-knit community. But when it comes to home insurance, the picture can be a little more complex. This article breaks down a real home and contents insurance quote for a 3-bedroom, 1-bathroom property in the suburb, examines how it stacks up against local and national benchmarks, and offers practical tips to help you manage your premium.

---

Is This Quote Fair?

The quote in question comes in at $6,786 per year (or $650/month), covering both building ($730,000 sum insured) and contents ($200,000), each with a $500 excess. Our price rating for this quote is Expensive — above average for the area.

To put that in perspective, the suburb average premium in Long Jetty sits at just $2,039 per year, with a median of $1,959. Even at the 75th percentile — meaning 75% of comparable quotes are cheaper — the figure is $2,618/yr. This quote lands well above that upper band, suggesting it is priced significantly higher than what most Long Jetty homeowners are paying.

That said, premiums are never one-size-fits-all. The sum insured here is $730,000 for the building alone, which is a substantial figure and will naturally push the premium upward. The contents cover of $200,000 adds further to the total. When you're insuring more, you generally pay more — but it's still worth asking whether the price is competitive for what's on offer.

---

How Long Jetty Compares

Understanding where your suburb sits relative to broader benchmarks is a useful exercise. Here's a snapshot:

| Benchmark | Average Premium | Median Premium |

|---|---|---|

| Long Jetty (NSW 2261) | $2,039/yr | $1,959/yr |

| Central Coast LGA (NSW) | $8,387/yr | — |

| New South Wales | $9,528/yr | $3,770/yr |

| National | $5,347/yr | $2,764/yr |

A few things stand out. Long Jetty's suburb-level average of $2,039 is actually well below both the NSW state average and the national average, which may reflect the relatively low catastrophe risk profile of the area (no cyclone zone, moderate flood risk in parts). The Central Coast LGA average of $8,387 is notably high, likely skewed by higher-value properties and waterfront homes across the broader region.

The quote being analysed here, at $6,786, sits above the national average of $5,347 but below the NSW state average of $9,528. In that context, it's not extraordinary — but when measured against the local suburb benchmark of $2,039, the gap is hard to ignore. You can explore more Long Jetty insurance data here.

It's worth noting that the suburb sample size is 36 quotes, which is a reasonable dataset but not enormous. Averages can shift as more data comes in, so treat these figures as a useful guide rather than an absolute rule.

---

Property Features That Affect Your Premium

Several characteristics of this property are likely contributing to the elevated premium. Understanding these factors can help you have more informed conversations with insurers.

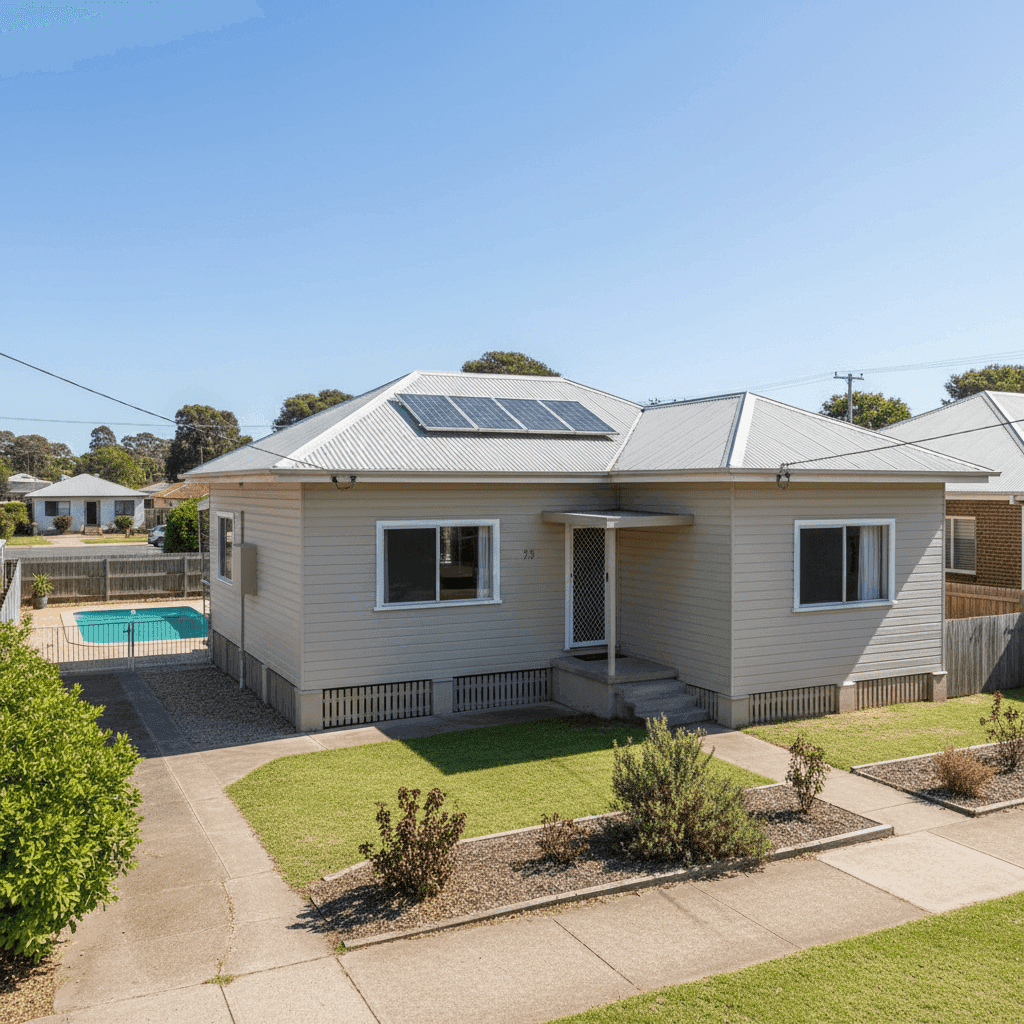

Fibro Asbestos Walls

This is arguably the most significant risk factor. Homes built with fibro asbestos (common in Australian homes constructed before the mid-1980s) carry higher rebuild costs and health and safety considerations. If the property is damaged and walls need to be replaced, the cost of safe removal and disposal of asbestos-containing materials is substantial. Insurers price this risk accordingly.

Construction Era (1960)

A home built in 1960 is over 60 years old. Older properties can have ageing electrical wiring, plumbing, and structural elements that increase the likelihood of a claim. Many insurers apply loading to premiums for homes of this age.

Swimming Pool

A pool adds both asset value and liability exposure. If a visitor or child is injured in or around the pool, the homeowner may face significant legal costs. This liability component is typically reflected in the premium.

Solar Panels

Solar panels increase the replacement value of the home and can also be a source of claims in storm or hail events. Their inclusion in the sum insured is important and does add to the overall cost.

Ducted Climate Control

Ducted air conditioning systems are expensive to repair or replace and are generally factored into the building sum insured. Their presence can subtly influence premium calculations.

Colorbond Roof

On the positive side, a steel Colorbond roof is generally viewed favourably by insurers. It's durable, fire-resistant, and less prone to storm damage than some alternatives like terracotta or older corrugated iron. This may help offset some of the other risk factors.

Slab Foundation & Timber/Laminate Flooring

A concrete slab foundation is generally considered stable and low-risk. Timber or laminate flooring, while attractive, can be susceptible to water damage — something worth keeping in mind when reviewing your contents cover.

---

Tips for Homeowners in Long Jetty

1. Review Your Sum Insured Carefully

A building sum insured of $730,000 is significant. Make sure this figure reflects the cost to rebuild — not the market value of the property. Overcovering can lead to unnecessarily high premiums, while undercovering leaves you exposed. Use a building calculator or speak to a quantity surveyor if you're unsure.

2. Get Clarity on Asbestos Coverage

Not all policies treat asbestos the same way. Before committing to a policy, confirm exactly how your insurer handles asbestos removal and disposal in the event of a claim. Some policies cap these costs or exclude them entirely. This is a critical detail for any pre-1990 fibro home.

3. Ask About Discounts and Bundling

Many insurers offer discounts for bundling home and contents cover (which this quote already does), paying annually rather than monthly, or for security features like deadbolts and alarms. It's always worth asking — these savings can add up.

4. Compare Multiple Quotes

The most effective way to know whether you're getting a fair deal is to compare. With a premium this far above the suburb average, shopping around is strongly recommended. Even a modest reduction could save you hundreds of dollars annually. Get a comparison quote at CoverClub to see what other insurers might offer for the same property.

---

Compare Your Options with CoverClub

Whether you're renewing your existing policy or shopping for the first time, it pays to compare. CoverClub makes it easy to see how your quote stacks up against real data from your suburb, your state, and across Australia. Start comparing home insurance quotes today and make sure you're not paying more than you need to for the cover your home deserves.