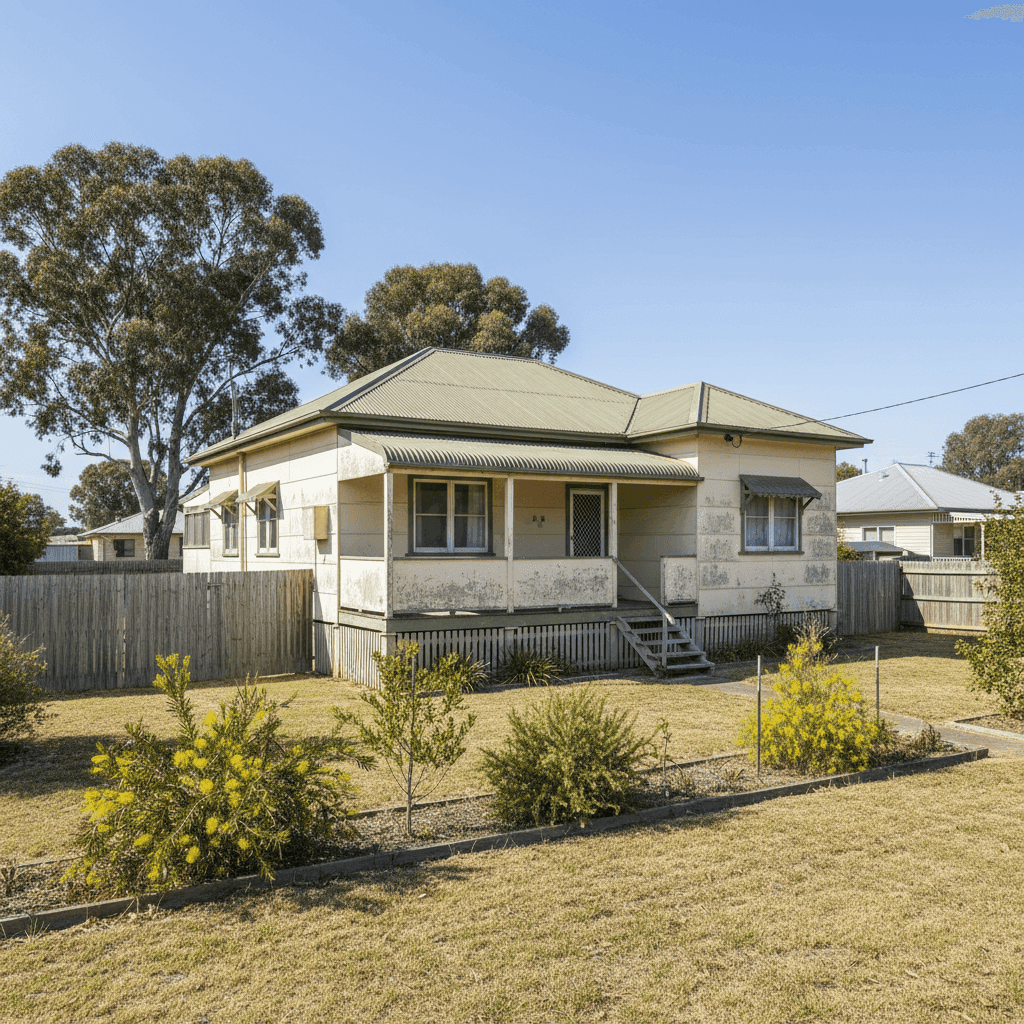

Longford is a quiet rural township in Victoria's Wellington Shire, situated in Gippsland near the Latrobe River. It's the kind of place where properties tend to have character — and this particular free standing home, built in 1980 with fibro asbestos walls and a Colorbond roof, is a solid example of the era's regional housing stock. But character comes with complexity when it comes to insurance pricing. If you've recently received a home and contents quote for a property like this, you may be wondering whether what you're paying is reasonable. Let's break it down.

---

Is This Quote Fair?

The quote in question sits at $3,471 per year (or $333/month) for a combined home and contents policy, covering a building sum insured of $450,000 and contents valued at $100,000, each with a $1,000 excess.

Our pricing analysis rates this quote as Expensive — above average for the Longford area. Here's why that matters:

The suburb average for Longford (3851) sits at just $2,177 per year, with a median of $2,161. This quote comes in at roughly 59% above the local suburb average — a significant gap that warrants attention. Even at the 75th percentile of local quotes ($2,356/yr), this premium is still considerably higher than what many Longford homeowners are paying.

That said, context is everything. Compared to the Victorian state average of $3,000/yr, this quote is only moderately above the norm. And when you factor in the Wellington LGA average of $4,409/yr, this quote actually looks more competitive within its broader local government context — sitting well below that benchmark.

The takeaway? While this premium isn't outlandish by state or LGA standards, there's meaningful room to shop around and potentially save several hundred dollars annually by comparing options.

---

How Longford Compares

Understanding where Longford sits in the broader insurance landscape helps put any individual quote into perspective.

| Benchmark | Annual Premium |

|---|---|

| Longford (3851) Average | $2,177 |

| Longford (3851) Median | $2,161 |

| Longford 25th Percentile | $1,892 |

| Longford 75th Percentile | $2,356 |

| Victoria Average | $3,000 |

| Victoria Median | $2,718 |

| Wellington LGA Average | $4,409 |

| National Average | $5,347 |

| National Median | $2,764 |

(Based on 19 quotes sampled for the Longford suburb.)

One thing that stands out immediately is how affordable Longford's suburb-level averages are compared to both state and national figures. The national average of $5,347/yr is more than double the local suburb average — a reflection of the enormous variation in risk profiles across Australia, from cyclone-prone northern Queensland to flood-affected river towns and bushfire zones.

Longford itself benefits from not being in a designated cyclone risk area, which keeps premiums lower than many regional counterparts. However, the Wellington LGA's elevated average ($4,409/yr) suggests that certain properties in the broader region do attract higher premiums — likely due to flood exposure, bushfire proximity, or older building characteristics.

---

Property Features That Affect Your Premium

Several characteristics of this property have a direct bearing on its insurance cost. Here's what insurers are likely weighing up:

Fibro Asbestos External Walls

This is arguably the most significant premium driver for this property. Homes with fibro asbestos cladding are more expensive to insure because of the specialised handling, disposal, and rebuilding costs associated with asbestos-containing materials. In the event of a claim, contractors must follow strict safety protocols, which substantially increases repair and rebuild costs. This alone can push premiums well above the suburb average.

Stump Foundation

The home sits on stumps, which is common for older Gippsland properties and homes in areas with reactive soils or flood-prone land. Stumped foundations can be more vulnerable to movement, pest activity (particularly termites), and flood inundation. Insurers factor in the added complexity and cost of repairing or relevelling a stumped home.

Timber and Laminate Flooring

Timber flooring, while aesthetically appealing, is more susceptible to water damage than tiled alternatives. In a claim scenario involving water ingress or flooding, timber floors often need full replacement rather than spot repairs — increasing the potential claim value.

1980 Construction

Homes built in 1980 are now over 40 years old. While many are structurally sound, ageing properties can carry higher risk profiles due to older wiring, plumbing, and materials that may not meet current building codes. Insurers price this in.

Ducted Climate Control

The presence of ducted climate control is a positive note — it's a higher-value fixture that adds to the rebuild cost, but it also signals a well-appointed home. It's worth ensuring your building sum insured accurately accounts for this system.

Colorbond Roof

Steel Colorbond roofing is generally viewed favourably by insurers. It's durable, fire-resistant, and lower maintenance than tiles, which can reduce the likelihood and cost of roof-related claims.

---

Tips for Homeowners in Longford

If you're paying above the suburb average, there are practical steps you can take to either reduce your premium or ensure you're getting genuine value for money.

1. Get multiple quotes and compare properly With only 19 quotes in our Longford sample, there's meaningful variation between insurers. A quote that's expensive with one provider may be competitive with another. Use CoverClub's free comparison tool to see a range of options side by side.

2. Review your building sum insured A sum insured of $450,000 for a 3-bedroom 1980s home with fibro walls may be higher than necessary — or it could be right on the money depending on local rebuild costs. Use a building calculator or speak with a quantity surveyor to confirm you're not over-insuring (which unnecessarily inflates premiums) or under-insuring (which could leave you exposed at claim time).

3. Understand your asbestos obligations If you're not already aware, homes with fibro asbestos cladding require licensed asbestos removalists for any work that disturbs the material. Ensure your policy explicitly covers asbestos-related removal and disposal costs in a claim scenario — not all standard policies do, or they may apply sub-limits.

4. Consider your excess carefully Both the building and contents excess are set at $1,000. Opting for a higher voluntary excess (say, $2,000 or $2,500) can meaningfully reduce your annual premium. This strategy works well if you have the financial buffer to cover a larger out-of-pocket cost in the event of a minor claim.

---

Compare Your Options with CoverClub

Whether you're renewing your policy or shopping around for the first time, it pays to compare. CoverClub makes it easy to benchmark your current quote against real market data and find a policy that suits your property and budget. Get a home insurance quote today and see how much you could save — without compromising on cover.

For more local data, explore the Longford suburb insurance stats, the broader Victoria insurance overview, or the national home insurance benchmarks.