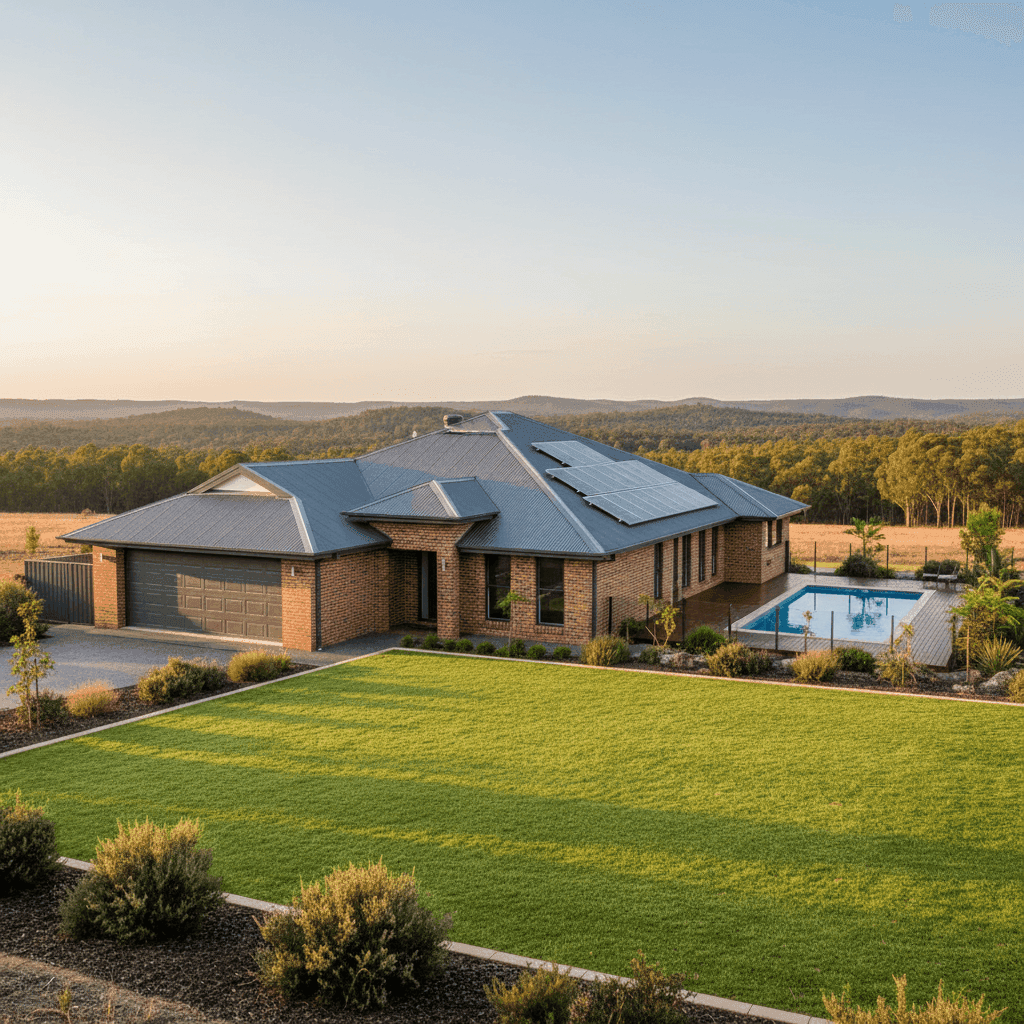

Lower Belford is a quiet rural locality tucked within the Hunter Valley, roughly an hour's drive north of Sydney. It's the kind of place where acreage blocks, new builds, and a relaxed lifestyle attract families looking to escape the city — and with that comes the very real need to protect what is often a significant property investment. This article breaks down a real home and contents insurance quote for a five-bedroom free standing home in Lower Belford (NSW 2335), examines how it stacks up against state and national benchmarks, and offers practical guidance for homeowners in the area.

---

Is This Quote Fair?

The quote in question sits at $3,636 per year (or $356 per month) for combined home and contents cover, with a building sum insured of $1,481,000 and contents valued at $99,000. Both the building and contents excess are set at $1,000 — a fairly standard arrangement.

Our pricing analysis rates this quote as CHEAP — below average for the market. That's genuinely good news for the homeowner. Given the size and quality of the property — a brand-new, five-bedroom home with top-of-the-range fittings, a pool, solar panels, and ducted climate control — securing cover at this price point represents solid value.

It's worth understanding what "cheap" means in context. It doesn't imply the cover is inadequate; rather, it means the premium is lower than what comparable properties are typically paying. For a home of this calibre, with a rebuild value approaching $1.5 million, a sub-$4,000 annual premium is a result worth noting.

---

How Lower Belford Compares

To put this quote in perspective, let's look at the broader pricing landscape.

| Benchmark | Annual Premium |

|---|---|

| This quote | $3,636 |

| NSW state median | $3,770 |

| NSW state average | $9,528 |

| National median | $2,764 |

| National average | $5,347 |

| Maitland LGA average | $13,875 |

A few things stand out here. First, the quote sits just below the NSW state median of $3,770 — meaning roughly half of NSW homeowners are paying more. Second, it is well beneath the NSW state average of $9,528, which is skewed upward by high-risk and high-value properties across the state. Third, the Maitland LGA average of $13,875 is strikingly high — more than three times this quote — suggesting that many properties in the broader Maitland area are attracting significantly elevated premiums, possibly due to flood exposure along the Hunter River corridor.

Compared to NSW home insurance averages and national benchmarks, this quote holds up very well. You can also explore localised data for the 2335 postcode on the Lower Belford suburb stats page.

It's also worth noting that the national median of $2,764 is lower than this quote — but that figure encompasses a wide range of property types, sizes, and locations across Australia, including modest homes in low-risk areas. For a large, high-value new build with premium inclusions, being close to the national median is a strong outcome.

---

Property Features That Affect Your Premium

Several characteristics of this property play a meaningful role in shaping the insurance premium — some pushing it up, others helping to keep it in check.

New construction (2024): A brand-new home is one of the most favourable factors from an insurer's perspective. Modern builds comply with current Australian building codes, use up-to-date materials, and carry far less risk of structural issues or outdated wiring. This almost certainly contributes to the competitive premium.

Brick veneer walls and Colorbond roof: Brick veneer is widely regarded as a resilient and insurer-friendly wall construction. Combined with a steel Colorbond roof — which is durable, fire-resistant, and low-maintenance — this property presents a lower claims risk profile than homes with timber cladding or terracotta tiles.

Concrete slab foundation: Slab foundations are standard for new builds in NSW and are generally considered stable and low-risk, particularly in areas without significant soil movement or flood exposure.

Swimming pool: Pools add to the insured value of the property and can introduce liability considerations, which typically nudges premiums upward. Ensuring your policy explicitly covers pool-related liability and the pool structure itself is important.

Solar panels: Solar systems are increasingly common and most insurers now include them under building cover — but it's worth confirming this with your insurer. Panels represent a meaningful asset (often $10,000–$20,000+) and should be adequately covered under your building sum insured.

Top-of-the-range fittings: High-end kitchens, bathrooms, and finishes increase the cost to rebuild or repair, which is reflected in the $1,481,000 building sum insured. Ensuring this figure accurately reflects current construction costs is critical — underinsurance remains one of the most common and costly mistakes Australian homeowners make.

Ducted climate control: Ducted systems are a significant fixed asset and are typically covered under building insurance. Their inclusion supports the higher sum insured and is worth factoring into any review of your coverage limits.

No cyclone risk: Lower Belford falls outside Australia's cyclone-prone zones, which removes one of the most significant premium loading factors seen in northern Queensland and parts of WA. This is a meaningful advantage for local homeowners.

---

Tips for Homeowners in Lower Belford

1. Review your sum insured annually Construction costs in NSW have risen sharply in recent years. A rebuild estimate that was accurate at the time of purchase may already be outdated. Use a building cost calculator or speak with a quantity surveyor to ensure your $1,481,000 sum insured still reflects current rates — especially for a home with premium fittings.

2. Confirm solar panels and pool equipment are covered Not all policies treat solar panels and pool equipment the same way. Ask your insurer specifically whether your solar system (including inverters and mounting hardware) and pool equipment (pumps, filters, heating) are included under your building cover — and to what limit.

3. Understand your flood and storm exposure The Hunter Valley region, including parts of the Maitland LGA, has a well-documented history of flooding. While Lower Belford itself may not be in a high-risk flood zone, it's worth confirming your policy's flood definition and whether storm surge or overland flow events are covered. These distinctions matter enormously at claim time.

4. Compare quotes before renewal Even if your current premium is competitive, the insurance market shifts every year. Insurers reprice based on claims data, reinsurance costs, and local risk assessments. Comparing quotes at renewal — rather than auto-renewing — is one of the simplest ways to avoid paying more than you need to.

---

Ready to Compare?

Whether you're a new homeowner in Lower Belford or coming up for renewal, it pays to see what the broader market has to offer. CoverClub makes it easy to compare home insurance quotes from multiple insurers in minutes — so you can be confident you're getting the right cover at a fair price.