Ludmilla is a quiet, established suburb sitting just a few kilometres from Darwin's CBD — but its proximity to the tropics means home insurance here carries some unique considerations. This article breaks down a real home and contents insurance quote for a six-bedroom, free-standing home in Ludmilla (postcode 0820), rated Fair (Around Average) by CoverClub's pricing engine. We'll unpack what's driving the premium, how it stacks up against local and national benchmarks, and what you can do to make sure you're getting the best value possible.

---

Is This Quote Fair?

The quoted annual premium of $7,395 (or $702/month) covers both building and contents, with a building sum insured of $1,311,000 and contents valued at $102,000. Both the building and contents carry a $1,000 excess.

CoverClub's analysis rates this quote as Fair — Around Average, and the numbers back that up. Within Ludmilla itself, the suburb average sits at $6,656/year and the median at $6,103/year. This quote lands above both of those figures, but it's well within the suburb's interquartile range — the 25th percentile is $4,927/year and the 75th percentile is $8,570/year. In other words, roughly half of comparable Ludmilla quotes fall between those two figures, and this one sits comfortably in the upper half of that band without breaching the top quarter.

That said, it's worth noting the suburb sample size is relatively small (7 quotes), so these averages should be treated as directional rather than definitive. As more data comes in, the picture may shift.

Given the property's size, age, and the elevated risk profile of the Northern Territory, a "Fair" rating here is a reasonable outcome — but it doesn't mean there's no room to improve.

---

How Ludmilla Compares

Understanding where Ludmilla sits in the broader insurance landscape helps put this quote in perspective. Here's a quick snapshot:

| Benchmark | Average Premium | Median Premium |

|---|---|---|

| Ludmilla (0820) | $6,656/yr | $6,103/yr |

| NT (State) | $10,773/yr | $3,402/yr |

| National | $5,347/yr | $2,764/yr |

| LGA (Unincorporated NT) | $4,811/yr | — |

A few things stand out immediately. The NT state average of $10,773/year is extraordinarily high — nearly double the national average — which reflects the concentration of high-risk, high-value properties across the Territory, particularly in cyclone-prone and remote areas. The state median of just $3,402/year tells a very different story, indicating a wide spread of premiums with a long tail of expensive outliers pulling the average up significantly.

Ludmilla's suburb average of $6,656/year sits well above the national average ($5,347/year) and the LGA average ($4,811/year), but comfortably below the NT state average. This positions Ludmilla as a moderately elevated-risk suburb — not the most expensive in the Territory, but meaningfully pricier than typical Australian suburbs.

For deeper data on local pricing trends, visit the Ludmilla suburb stats page, the NT state insurance stats, or the national home insurance overview.

---

Property Features That Affect Your Premium

This particular property has a number of characteristics that insurers weigh carefully when calculating risk. Here's how the key features play into the premium:

Cyclone Risk Area

This is arguably the single biggest factor. Ludmilla falls within a designated cyclone risk zone, and insurers price this in heavily. Cyclone damage can be catastrophic, and the cost of rebuilding after a severe event is substantial — especially for a large home. Expect cyclone risk to be a significant component of the base premium.

Property Size and Age

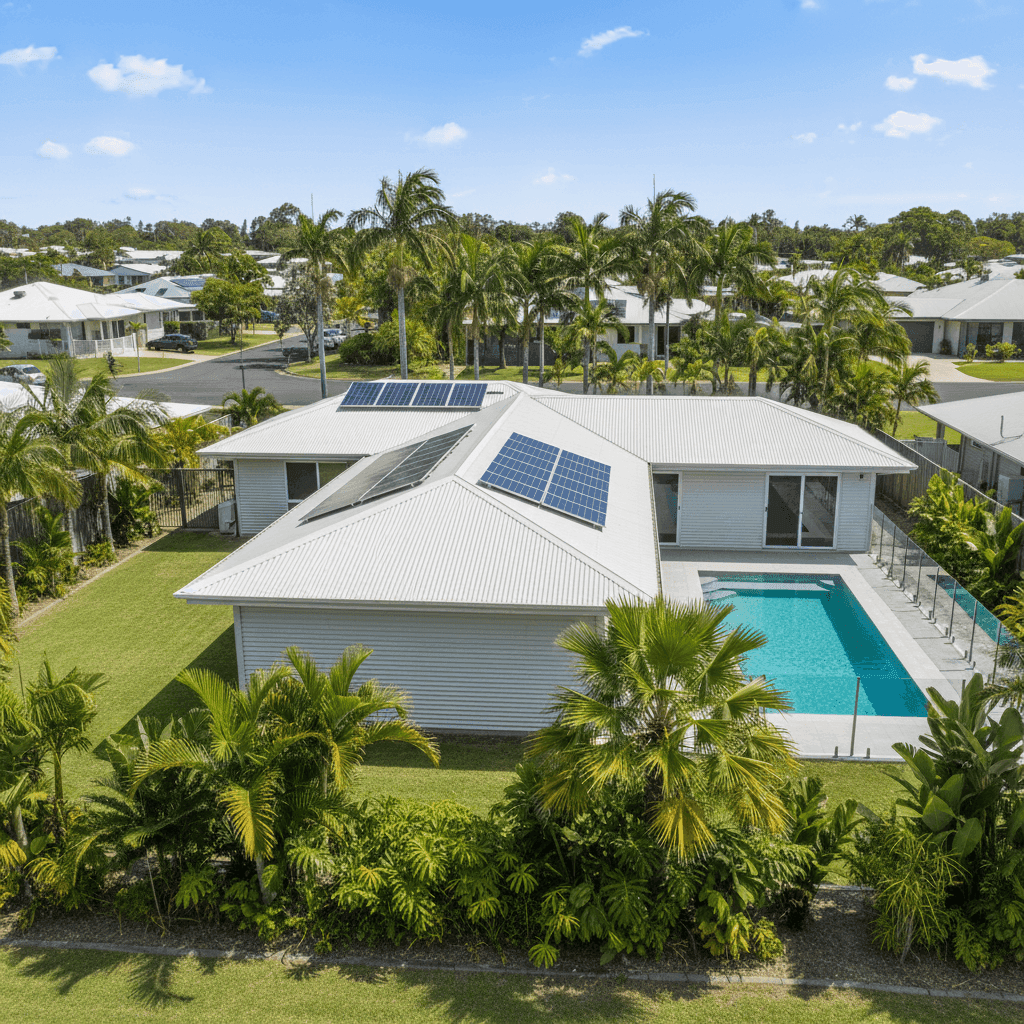

At 389 sqm with six bedrooms and three bathrooms, this is a substantial home. The larger the dwelling, the higher the rebuild cost — and at $1,311,000 sum insured, that's reflected here. The home was also built in 1978, which means it's over 45 years old. Older construction can present higher risk for insurers due to ageing materials, wiring, and plumbing, even when well-maintained.

Aluminium Walls and Colorbond Roof

Aluminium cladding and steel (Colorbond) roofing are generally viewed favourably by insurers — both materials are durable, fire-resistant, and well-suited to the Top End's harsh climate. These construction choices may help moderate the premium compared to timber-framed or older masonry homes.

Slab Foundation

A concrete slab foundation is typically considered low-risk for subsidence and termite ingress, which can work in the homeowner's favour during underwriting.

Pool, Solar Panels, and Ducted Climate Control

Each of these adds value — and therefore risk — to the property. A swimming pool increases liability exposure and adds to the rebuild cost. Solar panels are increasingly common in Darwin but represent an additional asset that needs coverage. Ducted climate control systems are expensive to replace and are factored into both the building sum insured and the overall risk assessment.

Timber and Laminate Flooring

Timber flooring, while aesthetically appealing, can be more susceptible to water and moisture damage than tiles — a relevant consideration in a tropical climate with high humidity and heavy wet season rainfall.

---

Tips for Homeowners in Ludmilla

If you're a homeowner in Ludmilla looking to get the most out of your insurance, here are four practical steps worth taking:

- Review your sum insured regularly. Construction costs in Darwin have risen sharply in recent years. Make sure your $1,311,000 building sum insured still reflects the true cost of rebuilding your home — not just its market value. Underinsurance is a common and costly mistake.

- Invest in cyclone-rated upgrades. Many insurers offer discounts or more competitive premiums for homes with cyclone-rated shutters, reinforced roofing fixings, or upgraded garage doors. Given the risk profile of the area, these improvements can pay for themselves over time — both in reduced premiums and genuine protection.

- Shop around at renewal time. A "Fair" rating means this quote is around average — but average isn't necessarily the best available. Insurers price risk differently, and the difference between the cheapest and most expensive quote for the same property can be thousands of dollars. Use CoverClub to compare multiple quotes side by side before renewing.

- Check your contents coverage. At $102,000, the contents sum insured should cover everything from furniture and appliances to clothing and personal items. Do a quick audit — especially after any major purchases — to ensure you're not underinsured on contents, particularly given the cost of replacing items damaged in a flood or cyclone event.

---

Compare Your Home Insurance with CoverClub

Whether you're renewing an existing policy or shopping around for the first time, CoverClub makes it easy to compare home and contents insurance quotes from multiple providers in one place. Don't settle for average when a better deal might be just a few clicks away. Get a quote today at CoverClub and see how much you could save.