If you own a free standing home on Macleay Island in Queensland's Redland City, you already know this bay island lifestyle comes with its own unique set of considerations — and home insurance is firmly on that list. This article breaks down a real home and contents insurance quote of $4,153 per year (or $398/month) for a 2-bedroom, 1-bathroom weatherboard home in postcode 4184, examining whether it's reasonable, how it stacks up against local and broader benchmarks, and what you can do to manage your premium.

---

Is This Quote Fair?

The short answer: it's on the higher side, but not dramatically out of step with what Macleay Island homeowners are paying.

This quote has been rated Expensive (Above Average) when measured against comparable properties in the suburb. The suburb average premium for Macleay Island sits at $3,267/year, with a median of $3,076/year. At $4,153, this quote lands just above the 75th percentile of $4,124 — meaning roughly three-quarters of similar quotes in the area come in cheaper.

That said, context matters. The 25th percentile for the suburb is $2,491/year, so there's meaningful variation across quotes. The gap between the cheapest and most expensive quotes in the suburb is significant, which suggests that shopping around could yield real savings.

It's also worth noting that the quote covers a $600,000 building sum insured alongside $10,000 in contents cover — a relatively modest contents figure. The building sum insured is the dominant cost driver here, and at $600,000 for a 105 sqm weatherboard home on stumps, it's worth double-checking that figure reflects accurate rebuild costs rather than market value.

---

How Macleay Island Compares

To put this quote in proper perspective, it helps to zoom out and look at the broader insurance landscape.

| Benchmark | Premium |

|---|---|

| This quote | $4,153/yr |

| Macleay Island suburb average | $3,267/yr |

| Macleay Island suburb median | $3,076/yr |

| LGA (Redland) average | $3,178/yr |

| QLD state median | $3,903/yr |

| QLD state average | $9,129/yr |

| National average | $5,347/yr |

| National median | $2,764/yr |

A few things stand out here. First, the Queensland state average of $9,129/year is extraordinarily high — a figure heavily skewed by far north Queensland properties facing severe cyclone and flood exposure. The state median of $3,903/year is a far more representative figure for most Queenslanders, and this quote sits just below that mark.

Compared to the national average of $5,347/year, this quote is actually below average — a reassuring sign for island homeowners who might expect to pay a significant premium for their location. The national median of $2,764/year is lower, reflecting the large proportion of lower-risk metropolitan properties across Australia.

The Redland LGA average of $3,178/year suggests that, broadly speaking, Macleay Island is priced in line with the surrounding region, though individual property characteristics can push premiums higher or lower.

---

Property Features That Affect Your Premium

Several characteristics of this particular home have a meaningful influence on the insurance premium quoted.

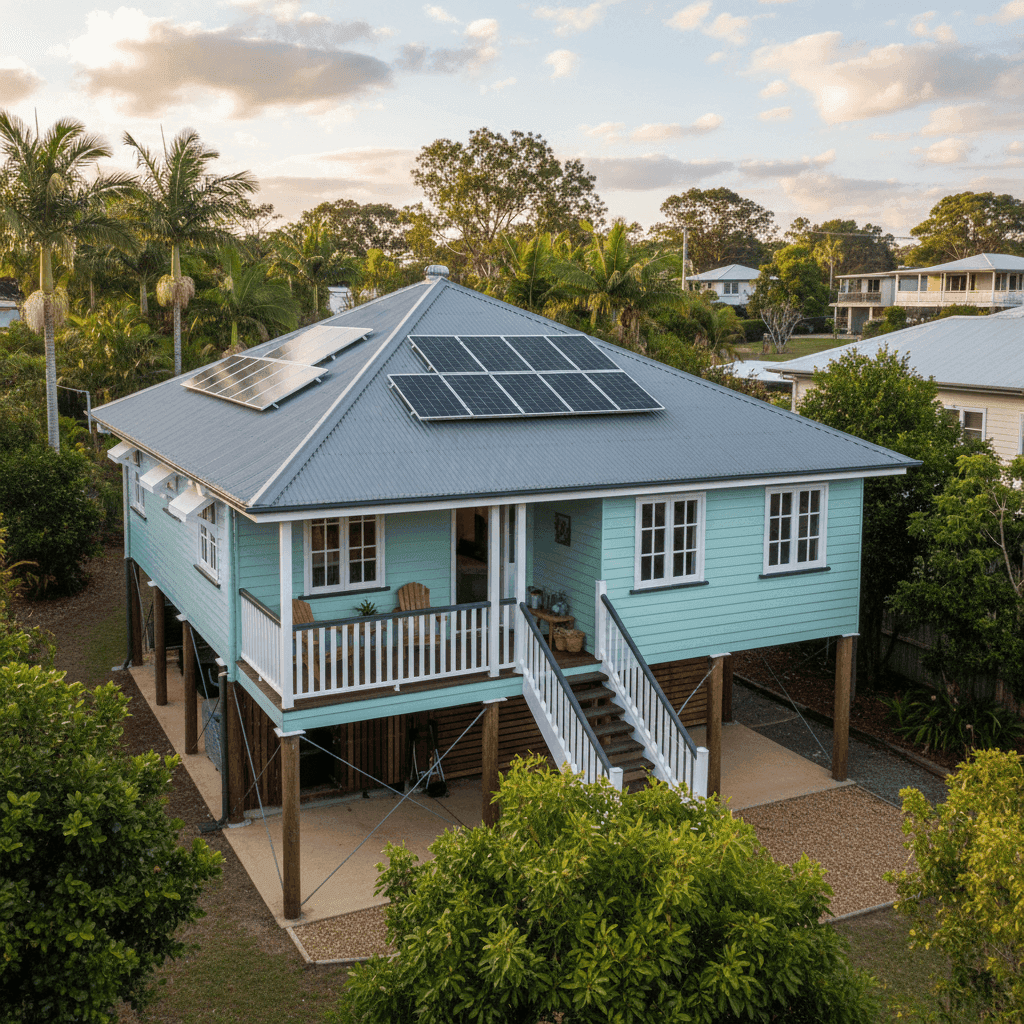

Weatherboard timber construction is one of the most significant factors. Timber-framed homes with weatherboard cladding are considered higher risk by insurers due to their susceptibility to fire, moisture damage, and general wear. Rebuild costs for this construction type can also be higher per square metre than brick or brick-veneer homes, which pushes up the sum insured.

Stump foundations are common in Queensland, particularly in older homes built before modern slab-on-ground construction became standard. While stumps allow for excellent airflow and can reduce flood risk by elevating the structure, insurers factor in the additional complexity of repairs and the potential for subfloor issues. This home is elevated by less than 1 metre — enough to offer some protection but not classified as a high-set Queenslander.

The 1990 construction year means the home is over 30 years old. Older homes can attract slightly higher premiums due to ageing materials, wiring, and plumbing systems that may be more prone to claims.

Timber and laminate flooring combined with the weatherboard exterior places this home firmly in a higher-risk construction category for insurers, particularly when it comes to water and storm damage.

On the positive side, the property has solar panels installed. Some insurers factor this into the building sum insured (since panels need to be replaced if damaged), but it also signals a well-maintained, modernised property. The ducted climate control system is another feature that adds to the replacement value of the home and should be accounted for in the building sum insured.

Notably, this property is not in a cyclone risk zone, which is a significant advantage for a Queensland island property. Cyclone-rated premiums in far north Queensland can be multiples of what's quoted here.

---

Tips for Homeowners in Macleay Island

1. Review your sum insured carefully A $600,000 building sum insured for a 105 sqm weatherboard home may be appropriate depending on current rebuild costs, but it's worth getting an independent building replacement cost estimate. Over-insuring pushes your premium up unnecessarily, while under-insuring can leave you exposed at claim time. Use a quantity surveyor or online calculator to validate the figure annually.

2. Compare multiple quotes With suburb premiums ranging from $2,491 at the 25th percentile to above $4,100 at the 75th, there's clearly significant variation between insurers for similar properties. Get a quote through CoverClub to compare options side by side and see whether a more competitive rate is available for your specific property.

3. Consider your contents cover amount A $10,000 contents sum insured is quite low for most households. Take stock of your furniture, appliances, clothing, and electronics — it's easy to underestimate how quickly replacement costs add up. Increasing contents cover is generally inexpensive relative to building cover, and it's far better to be adequately covered than to face a shortfall after a claim.

4. Ask about discounts and bundling Many insurers offer discounts for bundling home and contents cover (which this policy already does), paying annually rather than monthly, or for security features like deadbolts and alarm systems. It's always worth calling your insurer to ask what discounts may apply — you might be surprised.

---

Ready to Compare?

Whether you're renewing your existing policy or shopping for the first time, comparing quotes is the single most effective way to make sure you're not overpaying. Head to CoverClub to get a personalised home and contents insurance quote for your Macleay Island property, and see how your premium stacks up against the suburb, state, and national benchmarks we've outlined here. You can also explore detailed Macleay Island insurance statistics to better understand what your neighbours are paying.