Malua Bay is a peaceful coastal village on the NSW South Coast, nestled within the Shoalhaven local government area. It's the kind of place where residents enjoy ocean views, bush surrounds, and a relaxed lifestyle — but those same environmental charms can make home insurance a more complex (and costly) conversation. This article breaks down a real home and contents insurance quote for a four-bedroom, free-standing home in Malua Bay (postcode 2536), examines how it stacks up against local, state, and national benchmarks, and offers practical guidance for homeowners looking to get better value on their cover.

---

Is This Quote Fair?

The annual premium for this property came in at $7,134 per year (or $677/month), covering a building sum insured of $1,203,000 and contents valued at $90,000, each with a $1,000 excess.

Our pricing analysis rates this quote as Expensive — above average for the Malua Bay area. Based on 14 quotes sampled in the suburb, the average premium sits at $4,090 per year and the median at $4,176. This quote lands well above the suburb's 75th percentile of $4,463 — meaning it's higher than at least three-quarters of comparable quotes in the area.

That said, context matters. The building sum insured of $1,203,000 is substantial and likely reflects the above-average fittings quality and the property's size. A higher replacement value naturally pushes premiums upward, and insurers will price accordingly. Still, the gap between this quote and the suburb median is significant enough to warrant shopping around.

---

How Malua Bay Compares

Understanding where your premium sits relative to broader benchmarks is one of the most useful tools a homeowner has.

| Benchmark | Average Premium | Median Premium |

|---|---|---|

| Malua Bay (2536) | $4,090/yr | $4,176/yr |

| NSW (State) | $9,528/yr | $3,770/yr |

| National | $5,347/yr | $2,764/yr |

| Shoalhaven LGA | $11,272/yr | — |

A few things stand out here. The NSW state average of $9,528 is heavily skewed by high-value and high-risk properties across the state — the median of $3,770 tells a more grounded story. Similarly, the national average of $5,347 is pulled upward by cyclone-prone regions in Queensland and WA, while the national median sits at just $2,764.

The Shoalhaven LGA average of $11,272 is notably elevated, likely reflecting a mix of coastal flood risk, bushfire exposure, and higher-value dwellings across the region. By that measure, this quote is actually below the LGA average — which offers some reassurance that the pricing, while above the suburb norm, isn't entirely out of step with the broader area.

For a deeper dive into how premiums track across the postcode, visit the Malua Bay suburb stats page.

---

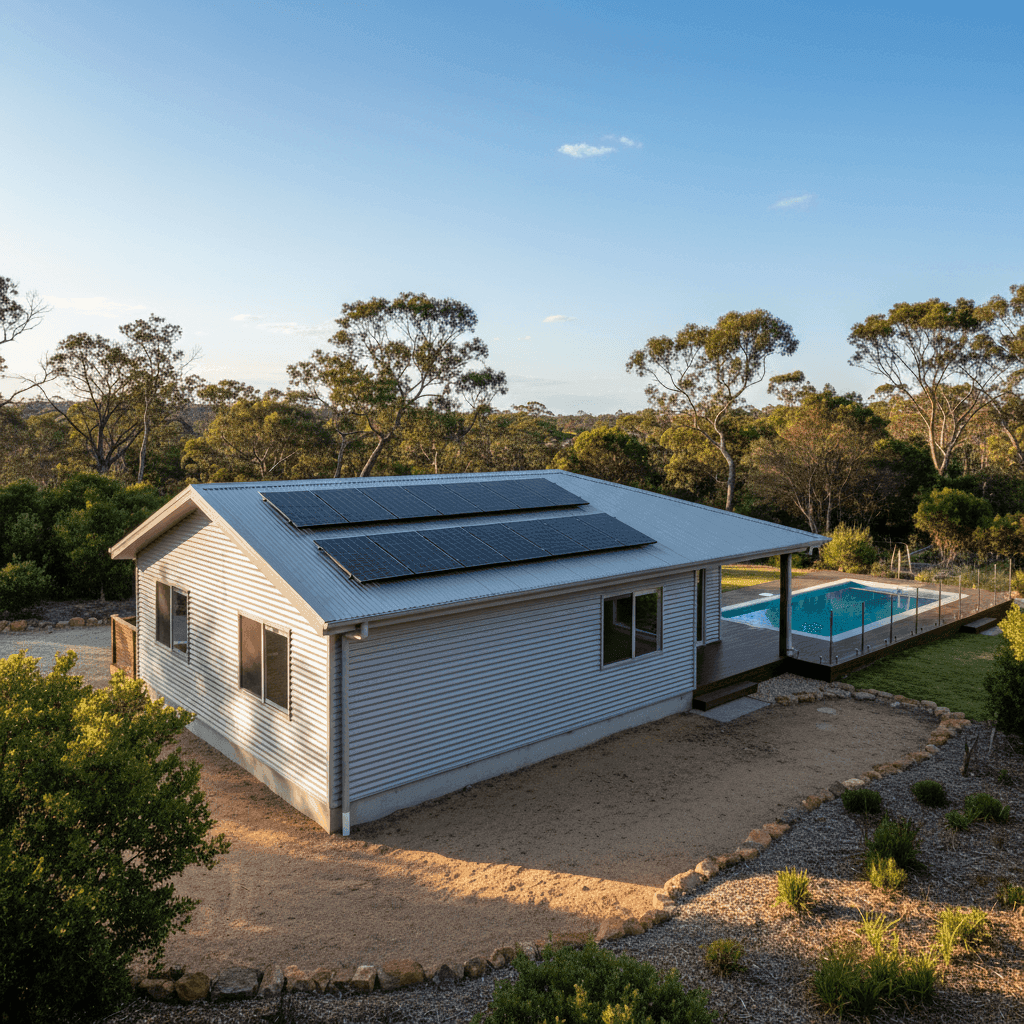

Property Features That Affect Your Premium

Several characteristics of this property will be influencing the premium, some in your favour and some working against you.

Aluminium cladding and Colorbond roof are generally viewed positively by insurers. Both materials are durable, fire-resistant, and low-maintenance — particularly important in coastal and bushfire-adjacent environments like Malua Bay. This combination can help moderate premiums compared to properties with timber weatherboard or terracotta tile roofing.

Concrete slab foundation is another plus. Slabs are structurally sound, resistant to pest damage, and less susceptible to movement than stumped or suspended foundations. Insurers typically regard slab construction as lower risk.

Timber and laminate flooring can be a double-edged sword. While aesthetically desirable, these materials are more vulnerable to water damage than tiles or polished concrete, which may factor into contents and building assessments.

Above-average fittings quality directly increases the cost to rebuild or repair. Premium fixtures, high-end appliances, and quality finishes all raise the sum insured required to restore the property to its original standard — and that flows through to your premium.

A swimming pool adds liability exposure and increases the replacement cost of the property, both of which nudge premiums higher.

Solar panels are an increasingly common feature, but they add to the insured value of the home and can complicate claims involving roof damage. Ensuring your policy explicitly covers solar panel systems — including the inverter and mounting hardware — is essential.

Ducted climate control is another high-value fixed asset that contributes to the building sum insured. Systems like these are expensive to replace and should be clearly itemised in your policy.

Slight elevation (less than 1 metre) offers modest protection against surface water intrusion but is unlikely to significantly reduce flood risk premiums on its own.

---

Tips for Homeowners in Malua Bay

1. Review your sum insured carefully A building sum insured of $1,203,000 is considerable. Make sure this figure reflects the actual cost to rebuild — not the market value of the land and property. Overcooking the sum insured is a common and costly mistake. Use a qualified quantity surveyor or your insurer's building calculator to validate the figure.

2. Shop around — seriously This quote sits above the suburb's 75th percentile. Even accounting for the high sum insured and quality fittings, there's a meaningful difference between this premium and the suburb average. Comparing quotes from multiple insurers through a platform like CoverClub can surface materially better pricing for equivalent cover.

3. Check your policy covers solar and pool Both features are present on this property and both can be sources of confusion at claim time. Confirm that your solar panel system (panels, inverter, wiring) is covered under your building policy, and that your pool and its equipment are explicitly included. Some policies exclude or limit cover for these items.

4. Consider your excess strategy Both the building and contents excess are set at $1,000. Increasing your excess — say, to $2,000 or $2,500 — can reduce your annual premium noticeably. If you're a low-claims household with solid savings, a higher excess can be a smart trade-off that pays off over time.

---

Compare Your Options with CoverClub

Whether you're renewing your policy or insuring a new property, it pays to know what the market looks like. CoverClub makes it easy to compare home and contents insurance quotes tailored to your specific property and location. If you own a home in Malua Bay or anywhere else on the NSW South Coast, get a quote today and see how your current premium stacks up.