Mandurah is one of Western Australia's most popular coastal cities — a relaxed, waterfront community about 75 kilometres south of Perth that continues to attract families, retirees, and investors alike. If you own a semi detached home in this area, understanding what you should be paying for home and contents insurance is a smart financial move. This article breaks down a real insurance quote for a 3-bedroom, 1-bathroom semi detached property in Mandurah (postcode 6210) and puts the numbers into context so you can make an informed decision.

---

Is This Quote Fair?

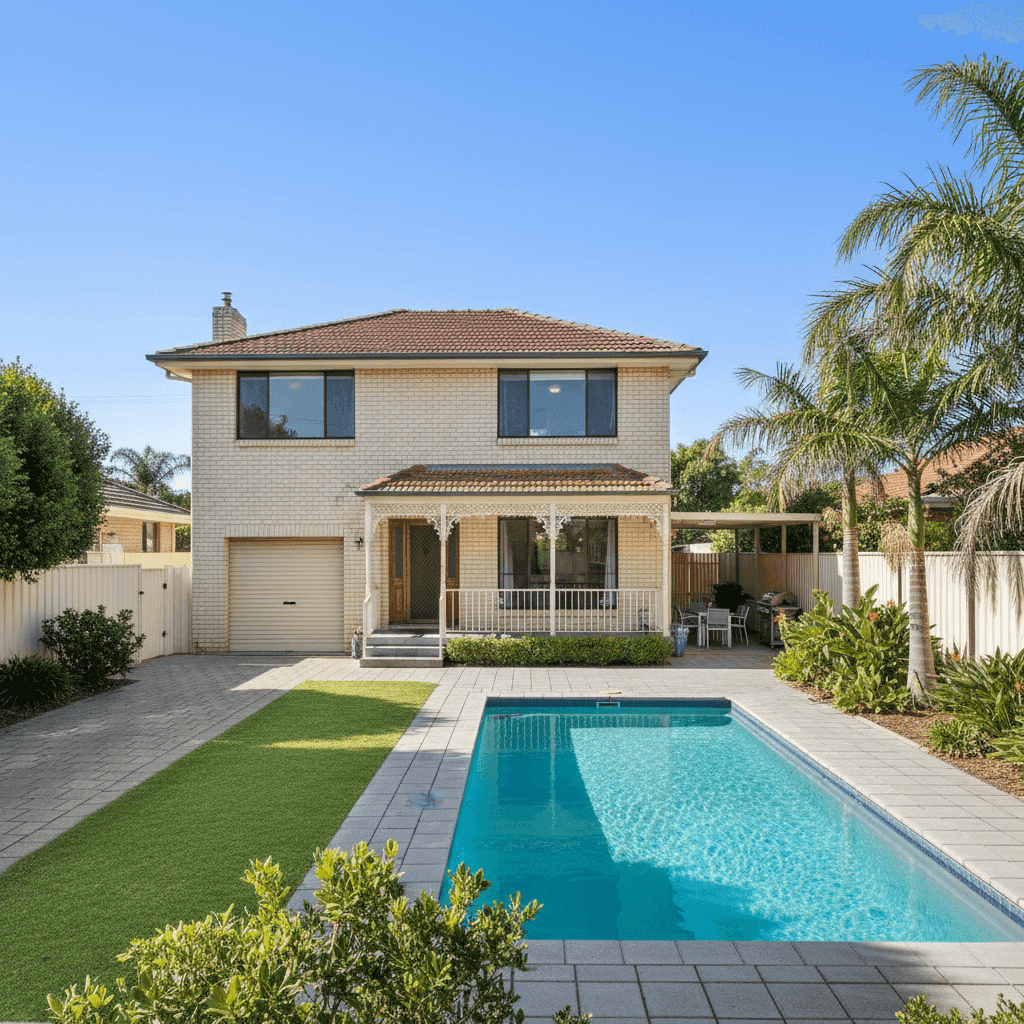

The annual premium on this quote comes in at $895 per year (or roughly $84 per month), covering both building and contents for a property insured at $685,000 for the building and $50,000 for contents. The building excess is $2,000 and the contents excess is $1,000.

Our price rating for this quote is FAIR — Around Average, and the data backs that up. The suburb median premium for Mandurah 6210 sits at $919 per year, meaning this quote is actually a touch below the midpoint of what other homeowners in the same postcode are paying. It's comfortably within a normal range — not a standout bargain, but certainly not overpriced either.

For context, the 25th percentile of quotes in this suburb is $555/yr, so there are cheaper options available in the market. At the same time, the 75th percentile reaches $1,758/yr — meaning a quarter of comparable properties are paying nearly double this premium. Landing close to the median is a reasonable outcome, particularly given the property's above-average fittings quality and the inclusion of a swimming pool, both of which typically push premiums upward.

---

How Mandurah Compares

One of the most striking takeaways from this quote is just how well Mandurah stacks up against broader benchmarks. Check out the numbers:

| Benchmark | Average Premium | Median Premium |

|---|---|---|

| Mandurah 6210 (suburb) | $1,173/yr | $919/yr |

| Mandurah LGA | $1,672/yr | — |

| Western Australia | $2,144/yr | $1,944/yr |

| Australia (National) | $2,965/yr | $2,716/yr |

Homeowners in Mandurah's 6210 postcode are paying significantly less than the WA state average and are well below the national average. The suburb average of $1,173/yr is roughly 45% lower than the WA average and over 60% lower than the national average. This reflects a combination of favourable risk factors in the area — including the absence of a designated cyclone risk zone — as well as the predominance of solid construction types like double brick.

You can explore more localised data on the Mandurah 6210 suburb stats page, compare it against the WA state overview, or see where it sits on the national insurance landscape.

It's worth noting that the LGA-wide Mandurah average ($1,672/yr) is considerably higher than the 6210 postcode average ($1,173/yr). This suggests that certain pockets within the broader Mandurah LGA — perhaps properties closer to flood-prone waterways or higher-value beachfront homes — are pulling that figure upward. The 6210 postcode appears to be one of the more affordably insured areas within the region.

---

Property Features That Affect Your Premium

Several characteristics of this property play a meaningful role in how insurers calculate the premium.

Double Brick Construction Double brick is widely regarded by insurers as one of the most resilient wall types available. It offers strong resistance to impact, fire, and general wear, which typically translates to lower rebuild risk and more competitive premiums compared to timber or lightweight cladding alternatives.

Tiled Roof Terracotta or concrete tiles are a durable roofing choice that performs well in most Australian climates. Tiled roofs generally attract favourable treatment from underwriters, though they can be more costly to repair after storm or hail events than metal roofing — something worth keeping in mind when reviewing your sum insured.

Slab Foundation & Tiled Flooring A concrete slab foundation is standard for homes of this era in WA and is considered low-risk by most insurers. Combined with tiled flooring throughout, there's reduced exposure to water damage and subsidence claims compared to properties with timber subfloors.

Construction Year: 1981 Homes built in the early 1980s are generally well-established and have moved past the higher-risk early years of a building's life. However, older properties may have ageing plumbing, electrical systems, or roofing materials that could increase claim likelihood over time. It's worth ensuring your sum insured ($685,000 in this case) reflects current rebuild costs, not just market value.

Swimming Pool The presence of a pool adds a layer of liability and maintenance risk that insurers factor into the premium. Pool-related claims — from equipment failure to accidental damage — are not uncommon, so it's important to confirm your policy explicitly covers pool structures and associated liability.

Above-Average Fittings Quality Higher-quality fixtures and fittings mean higher replacement costs in the event of a claim. This is appropriately reflected in both the sum insured and the premium, and it's a factor homeowners sometimes underestimate when setting their coverage levels.

---

Tips for Homeowners in Mandurah

1. Review Your Sum Insured Annually Building costs in WA have risen considerably over recent years. A sum insured of $685,000 for a 105 sqm semi detached may be appropriate today, but it's worth revisiting each renewal to ensure it keeps pace with construction cost inflation. Underinsurance is one of the most common — and costly — mistakes homeowners make.

2. Shop the Market at Renewal Time The wide spread of premiums in this suburb (from $555/yr at the 25th percentile to $1,758/yr at the 75th percentile) shows that insurers price this area very differently. Don't auto-renew without comparing — there may be meaningfully cheaper cover available for the same level of protection.

3. Consider Your Excess Levels Strategically This policy carries a $2,000 building excess and $1,000 contents excess. Opting for a higher excess is one of the most effective ways to reduce your annual premium, but make sure the excess amount is genuinely affordable for you in the event of a claim. A higher excess that you can't comfortably pay defeats the purpose of having insurance.

4. Check Your Pool and Liability Cover If you have a swimming pool, confirm that your policy covers the pool structure itself, any associated equipment (pumps, filters, heating), and — critically — public liability in case a guest or neighbour is injured on your property. Not all standard policies include comprehensive pool cover by default.

---

Compare Quotes and Find Better Value

Whether this quote looks right for your situation or you're wondering if you could be paying less, the best way to find out is to compare. CoverClub makes it easy to get multiple home and contents quotes side by side, so you can see exactly what's on offer for your property in Mandurah. Start comparing quotes today and make sure your home is protected at a price that makes sense.