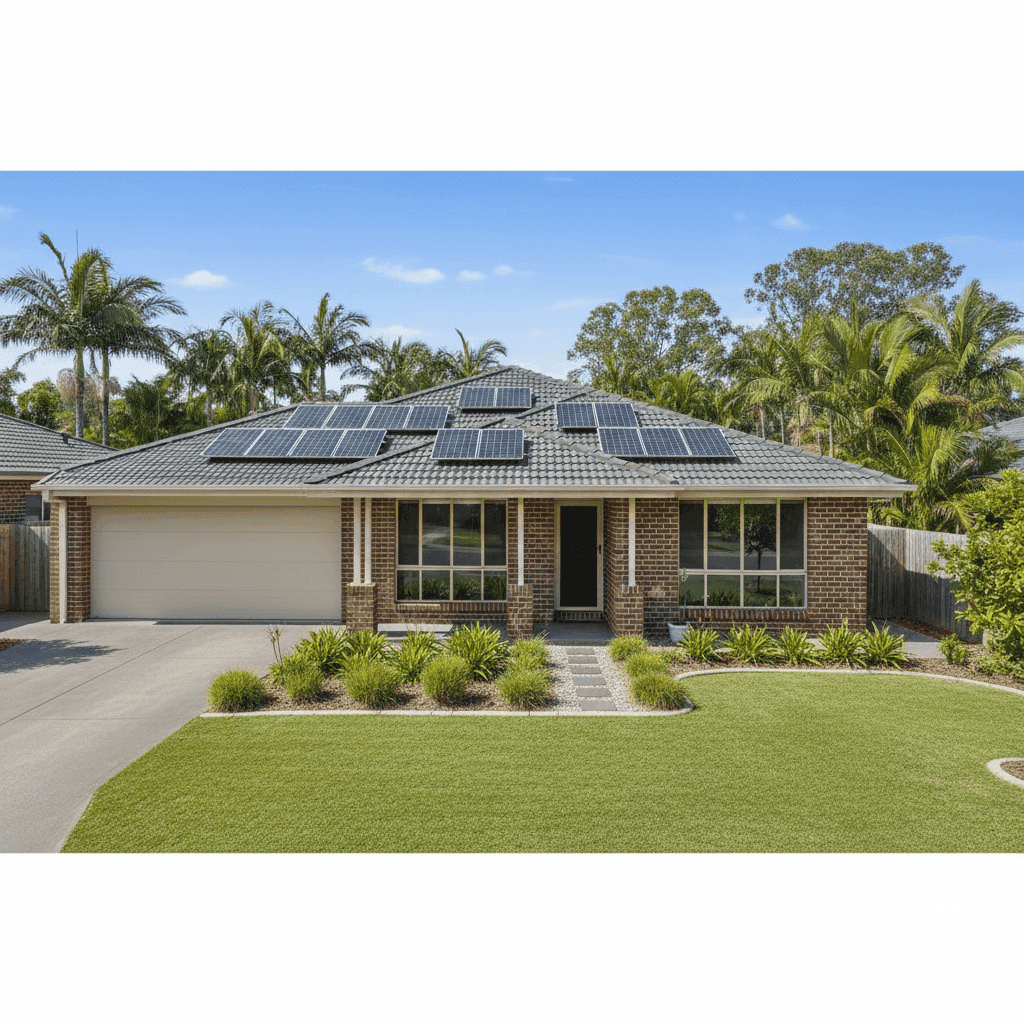

A four-bedroom, two-bathroom free standing home in Mango Hill, QLD 4509 is a solid asset worth protecting. Built in 2015, this brick veneer property sits on a concrete slab, features a tiled roof, and comes with solar panels — a profile that's increasingly common across the northern suburbs of Brisbane. But what does home and contents insurance actually cost for a home like this, and is the quote on the table a good deal? Let's break it down.

---

Is This Quote Fair?

The annual premium for this property comes in at $1,424 per year (or roughly $142 per month), covering both building and contents. The building is insured for $503,000, with $50,000 in contents cover — a reasonable setup for a well-appointed family home.

By any measure, this is a cheap quote. CoverClub's pricing analysis rates it as below average, meaning it sits well beneath what most comparable properties in the area are paying. The building excess is set at $3,000 and the contents excess at $1,000, which are on the higher side and partly explain the lower premium — but even accounting for that, this quote represents strong value.

To put it in perspective: the suburb average for Mango Hill is $6,202 per year, and the median sits at $4,830. This quote is paying less than a third of the average and less than a third of the median. That's a significant saving — potentially thousands of dollars annually.

---

How Mango Hill Compares

Understanding where Mango Hill sits in the broader insurance landscape helps put this quote into context. You can explore the full data on the Mango Hill insurance stats page.

| Benchmark | Premium |

|---|---|

| This Quote | $1,424/yr |

| Mango Hill 25th Percentile | $2,477/yr |

| Mango Hill Median | $4,830/yr |

| Mango Hill Average | $6,202/yr |

| Mango Hill 75th Percentile | $9,324/yr |

| Moreton Bay LGA Average | $3,435/yr |

| QLD State Average | $9,129/yr |

| QLD State Median | $3,903/yr |

| National Average | $5,347/yr |

| National Median | $2,764/yr |

A few things stand out here. Queensland's state average of $9,129 is notably high — well above the national average of $5,347 — largely driven by properties in cyclone-risk zones in Far North Queensland pushing premiums upward. You can dig into the full Queensland insurance data and national comparisons for more context.

Mango Hill itself sits in the Moreton Bay LGA, where the average premium of $3,435 is far more moderate than the broader state figure. This reflects the area's relatively low natural hazard exposure compared to coastal or far-north Queensland locations. Even so, this particular quote beats the LGA average by more than 50%.

It's worth noting that the suburb sample size is 19 quotes, which is a reasonable dataset but not enormous — averages can shift as more data comes in. Still, the directional story is clear: this is a very competitively priced policy.

---

Property Features That Affect Your Premium

Several characteristics of this property work in its favour from an insurance pricing perspective:

Brick veneer construction is generally viewed favourably by insurers. It's durable, fire-resistant, and less susceptible to storm damage than timber-framed weatherboard homes. Combined with a tiled roof, the property presents a low-risk profile structurally.

Concrete slab foundation is the standard for modern Queensland builds and is well-regarded by underwriters — it's stable, resistant to termite ingress, and less prone to movement than older pier-and-beam foundations.

The 2015 construction year is another positive. Newer homes are built to more stringent Australian Standards, including updated wind and cyclone resistance requirements, improved electrical safety, and modern plumbing. Insurers tend to price newer homes more favourably than older stock that may carry unknown maintenance issues.

Solar panels are worth mentioning. They add value to the property and are typically covered under building insurance, but some policies treat them differently — it's worth confirming with your insurer that your solar system (including inverter and mounting hardware) is explicitly covered under your building sum insured.

The above-average fittings quality is reflected in the $503,000 building sum insured for a 244 sqm home — approximately $2,062 per square metre. This is a reasonable rebuild cost estimate for a well-finished home in this area, though it's always worth reviewing your sum insured annually to keep pace with construction cost inflation.

The absence of a pool and ducted climate control simplifies the risk profile slightly, and the property falling outside a cyclone risk zone is a meaningful factor in keeping premiums lower than many other Queensland postcodes.

---

Tips for Homeowners in Mango Hill

1. Review your building sum insured annually Construction costs in South East Queensland have risen significantly over recent years. A sum insured that was accurate in 2022 may no longer reflect what it would cost to fully rebuild your home today. Use a quantity surveyor's estimate or an online rebuild calculator to stay on top of this — underinsurance is one of the most common and costly mistakes homeowners make.

2. Understand your excess structure This policy carries a $3,000 building excess and a $1,000 contents excess. Higher excesses lower your premium, but make sure you can comfortably cover those amounts out of pocket if you need to make a claim. If cash flow is a concern, it may be worth paying a slightly higher premium in exchange for a lower excess.

3. Confirm solar panel coverage With solar panels installed, check your policy wording carefully. Most home insurance policies cover panels as part of the building, but coverage for accidental damage, inverter failure, or storm damage can vary. Ask your insurer directly what's included and what's excluded.

4. Compare quotes at renewal time Even if you're happy with your current premium, the insurance market moves. Insurers reprice risk regularly, and a policy that was competitive last year may not be the best deal at renewal. Spending 15 minutes comparing quotes before you renew can save you hundreds — or in some cases, thousands — of dollars.

---

Ready to Compare?

Whether you're reviewing an existing policy or shopping for cover for the first time, CoverClub makes it easy to see what home and contents insurance should cost for your specific property. Get a quote today and find out if you're paying a fair price — or leaving money on the table.