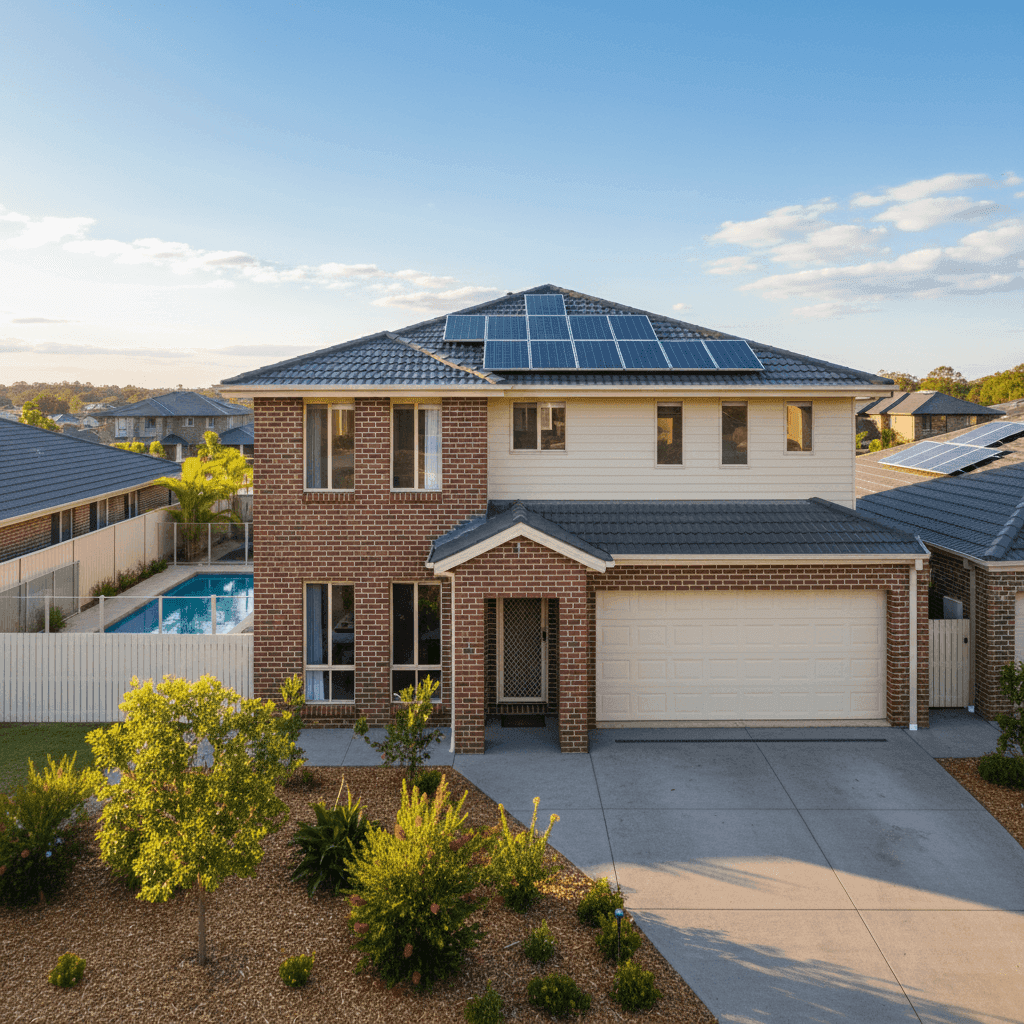

If you own a free standing home in Mango Hill, QLD 4509, you already know the suburb has a lot going for it — strong infrastructure, family-friendly streets, and solid property values in the Moreton Bay region. But what does it actually cost to insure a home here, and how do you know whether the quote sitting in your inbox is a good deal or not?

This article breaks down a real home and contents insurance quote for a four-bedroom, two-bathroom brick veneer home in Mango Hill, comparing it against suburb, state, and national benchmarks so you can make a genuinely informed decision.

---

Is This Quote Fair?

The quote in question comes in at $2,293 per year (or around $220 per month) for combined home and contents cover, with a building sum insured of $704,000 and contents valued at $100,000. Both the building and contents excess are set at $1,000 — a fairly standard arrangement.

Our pricing engine rates this quote as CHEAP — below average for the area. That's a meaningful finding. It doesn't simply mean the premium is low in absolute terms; it means this quote is priced below what most comparable properties in Mango Hill are paying, which is a genuinely positive signal for the homeowner.

To put it in perspective: the 25th percentile for premiums in this suburb sits at $2,477 per year. This quote, at $2,293, comes in below even that threshold — meaning it's cheaper than at least three-quarters of comparable quotes we've seen in the 4509 postcode. That's a strong result.

---

How Mango Hill Compares

Understanding where a quote sits relative to local and broader benchmarks is one of the most useful things you can do before signing up for a policy. Here's how the numbers stack up:

| Benchmark | Annual Premium |

|---|---|

| This Quote | $2,293 |

| Mango Hill Suburb Average | $6,202 |

| Mango Hill Suburb Median | $4,830 |

| Mango Hill 25th Percentile | $2,477 |

| Moreton Bay LGA Average | $3,435 |

| QLD State Average | $9,129 |

| QLD State Median | $3,903 |

| National Average | $5,347 |

| National Median | $2,764 |

A few things stand out here. First, the suburb average of $6,202 is dramatically higher than the median of $4,830 — which suggests a relatively small number of very expensive quotes are pulling the average upward. With only 19 quotes in our Mango Hill sample, a handful of outliers (perhaps homes with higher rebuild values or greater risk profiles) can skew that figure considerably.

Second, Queensland as a state has one of the highest average premiums in the country at $9,129 per year — largely driven by cyclone-prone northern and coastal regions. Mango Hill, sitting south-east of Brisbane, is not classified as a cyclone risk area, which is a significant factor in keeping premiums more manageable here.

Third, this quote comes in well below the national median of $2,764, which is itself a useful reference point. Broadly speaking, this homeowner is paying less than most Australian homeowners with similar cover.

You can explore the full breakdown for this postcode at our Mango Hill insurance stats page, compare it against Queensland-wide data, or see how it sits against national benchmarks.

---

Property Features That Affect Your Premium

Insurance pricing isn't arbitrary — every feature of a property feeds into the risk calculation. Here's how this particular home's characteristics likely influence the quote:

Brick veneer construction and tile roof are generally viewed favourably by insurers. Brick veneer is durable, fire-resistant, and performs well in storms compared to lightweight cladding. Tiled roofs similarly offer good longevity and weather resistance, though they can be more costly to repair after hail events than metal roofing.

Slab foundation is standard for homes built in Queensland from the 1990s onward and carries no particular premium loading. A home built in 1999 sits in a relatively modern bracket — post-1980s construction typically benefits from improved building codes, particularly around cyclone strapping and structural standards.

Swimming pool — pools add a layer of liability and replacement cost to a policy. Insurers factor in the cost of the pool structure itself, as well as any associated fencing and equipment, when calculating building cover.

Solar panels are an increasingly common feature and are generally covered under building insurance as a fixed installation. However, it's worth confirming with your insurer that your system is explicitly covered — both for storm damage and for electrical faults.

Ducted climate control adds to the overall value of the home's fixtures and fittings, which is reflected in the building sum insured. At $704,000, the rebuild value accounts for a 214 sqm home with standard fittings quality, inclusive of features like the ducted system and pool.

Contents cover of $100,000 is a reasonable starting point for a four-bedroom home, though homeowners should periodically audit their contents — particularly electronics, furniture, and valuables — to ensure they're not underinsured.

---

Tips for Homeowners in Mango Hill

Whether you're reviewing an existing policy or shopping around for the first time, here are four practical steps worth taking:

1. Don't anchor to the suburb average The average premium in Mango Hill is $6,202, but as we've seen, that figure is skewed by outliers. Use the median ($4,830) as a more realistic benchmark — and remember that a well-priced quote like this one can come in significantly below even that.

2. Review your sum insured annually Construction costs in South East Queensland have risen sharply in recent years. A rebuild cost estimate that was accurate in 2022 may be materially understated today. Use a building cost calculator or speak with a quantity surveyor if you're unsure whether $704,000 reflects the true cost to rebuild your home from scratch.

3. Check your solar panels are explicitly covered Solar installations are a grey area for some policies. Confirm whether your insurer covers panel damage (hail, storms), inverter failure, and any resulting damage to the roof or electrical system. Don't assume — ask directly.

4. Consider your excess strategically A $1,000 excess on both building and contents is standard, but increasing your excess can meaningfully reduce your premium. If you're financially comfortable absorbing a higher out-of-pocket cost in the event of a claim, bumping the excess to $2,000 or more could shave a noticeable amount off your annual bill.

---

Ready to Compare?

A below-average quote is a great start — but it's only meaningful if the cover itself is right for your needs. Policy inclusions, exclusions, and claim handling vary considerably between insurers, and the cheapest premium doesn't always represent the best value.

Compare home insurance quotes at CoverClub to see how multiple insurers price your specific property in Mango Hill. It takes minutes, and you might be surprised by the range on offer.