If you own a free standing home in Manilla, NSW 2346, you're probably curious whether you're getting a fair deal on your home insurance. Manilla is a small rural town in the Tamworth Regional Council area, nestled in the New England region of New South Wales. Like many country properties, homes here come with their own unique risk profile — and that has a direct bearing on what you'll pay to protect yours.

In this article, we break down a real home and contents insurance quote for a 3-bedroom, 1-bathroom free standing home in Manilla, examining how the premium stacks up against local, state, and national benchmarks — and what you can do to make sure you're not paying more than you need to.

---

Is This Quote Fair?

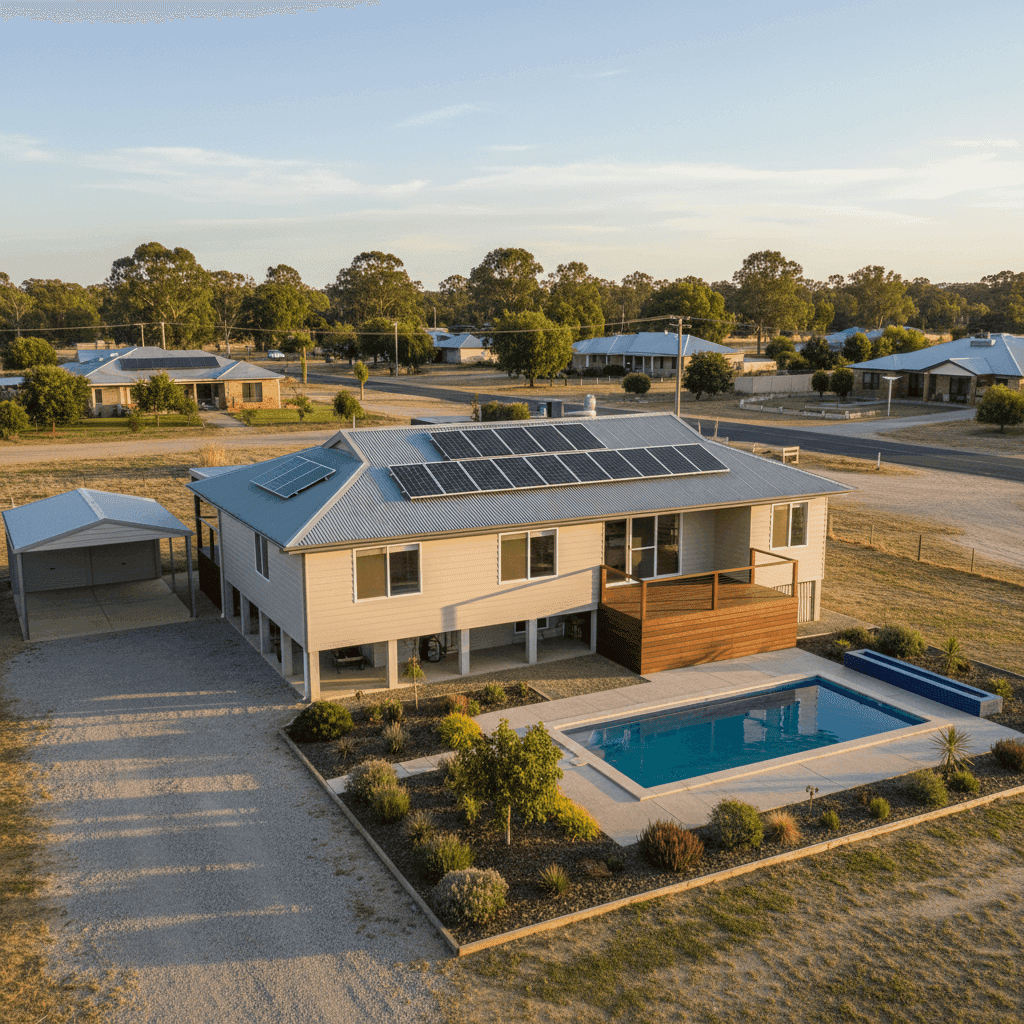

The quote in question comes in at $4,224 per year (or $398/month) for combined home and contents cover, with a building sum insured of $619,000 and contents valued at $80,000. Both the building and contents excess are set at $1,000.

Our price rating for this quote is FAIR — Around Average, which is a reasonable outcome for a property of this type in this location.

To put that in context:

- The suburb average for Manilla (postcode 2346) sits at $3,964/yr, with a median of $3,928/yr

- The 25th percentile is $3,697/yr and the 75th percentile is $4,537/yr

- This quote falls between the median and the 75th percentile, meaning it's slightly above the middle of the pack but still within the normal range for the area

In practical terms, this homeowner is paying a little more than half of Manilla's quoted properties, but is comfortably below the top quarter. Given the property's features — including a swimming pool and solar panels — a modest premium uplift above the median is entirely expected. You can explore the full Manilla suburb insurance stats on CoverClub for more detail.

---

How Manilla Compares

One of the more striking takeaways from this data is just how differently Manilla fares compared to broader benchmarks.

| Benchmark | Average Premium | Median Premium |

|---|---|---|

| Manilla (2346) | $3,964/yr | $3,928/yr |

| LGA (Tamworth Regional) | $4,038/yr | — |

| NSW | $9,528/yr | $3,770/yr |

| National | $5,347/yr | $2,764/yr |

The NSW average of $9,528/yr looks alarming at first glance, but the median of $3,770/yr tells a more accurate story — the state average is heavily skewed by high-risk coastal and flood-prone areas, particularly in Greater Sydney and parts of northern NSW. Manilla's premiums sit very close to the NSW median, suggesting it's a relatively moderate-risk location from an insurer's perspective.

Nationally, the picture is similar. The national average of $5,347/yr is pulled upward by cyclone-prone Queensland and flood-affected regions, while the median of $2,764/yr reflects the more typical Australian homeowner experience.

For Manilla specifically, premiums align closely with the broader NSW state data, and the Tamworth LGA average of $4,038/yr is virtually identical to the suburb average — suggesting consistent pricing across the region. With only 21 quotes in the Manilla sample, there's some natural variability, but the data paints a coherent picture.

---

Property Features That Affect Your Premium

Several characteristics of this particular property will have influenced the final premium. Understanding these factors helps explain why the quote lands where it does.

Hardiplank / Hardiflex Cladding

Fibre cement cladding such as Hardiplank or Hardiflex is generally viewed favourably by insurers. It's more resistant to fire and rot than timber weatherboards, and typically attracts lower premiums than brick veneer alternatives in some markets. It's a solid, low-maintenance external wall material that suits the Manilla climate well.

Steel / Colorbond Roof

A Colorbond steel roof is one of the most insurer-friendly roofing materials in Australia. It's durable, fire-resistant, and performs well in high-wind conditions. Compared to terracotta tiles or older corrugated iron, Colorbond can contribute to a more competitive premium.

Stump Foundation

Homes on stumps (also known as pier or post foundations) are common in regional NSW. While this style of construction is well-suited to the local terrain, it can introduce some additional underwriting considerations — particularly around subfloor maintenance and pest access. It's worth ensuring your policy covers subfloor structures adequately.

Swimming Pool

The presence of a pool adds to the insured value of the property and introduces additional liability considerations. Most home and contents policies include public liability cover, which is especially relevant when you have a pool. Make sure your policy's liability limit is sufficient.

Solar Panels

Solar panels are increasingly common and are generally covered under home building insurance as a fixed structure. However, it's worth confirming with your insurer that your panels are explicitly included in your sum insured and that coverage extends to inverter damage and storm events.

Construction Year (1995) and Vinyl Flooring

A home built in 1995 is relatively modern by regional standards and shouldn't attract significant age-related loading. Vinyl flooring is straightforward to replace and generally doesn't complicate claims assessments.

---

Tips for Homeowners in Manilla

Whether you're reviewing an existing policy or shopping around for the first time, here are some practical steps to make sure you're getting the best value.

- Review your sum insured annually. Building costs have risen significantly in recent years due to labour shortages and material price increases. A sum insured of $619,000 for a 130 sqm home in Manilla may be appropriate today, but it's worth recalculating your replacement cost each year using a building cost estimator to avoid being underinsured.

- Confirm solar panel and pool coverage explicitly. Don't assume these features are automatically included at full value. Ask your insurer to confirm in writing that solar panels (including the inverter) and pool infrastructure are covered under your building policy.

- Consider your excess strategically. Both the building and contents excess on this quote are set at $1,000. Opting for a higher excess — say $2,500 — can meaningfully reduce your annual premium. If you have a good claims history and solid emergency savings, this can be a smart trade-off.

- Compare at renewal time. The insurance market is competitive, and loyalty doesn't always pay. Even if your current premium seems fair, running a comparison at renewal can reveal meaningfully cheaper options for the same level of cover. Get a new quote through CoverClub to see what else is available in your area.

---

Compare Home Insurance in Manilla Today

Whether this quote reflects your own situation or you're simply researching what home insurance costs in Manilla, the best way to ensure you're getting fair value is to compare multiple policies side by side. CoverClub makes it easy to see real quotes for properties like yours — so you can make a confident, informed decision.