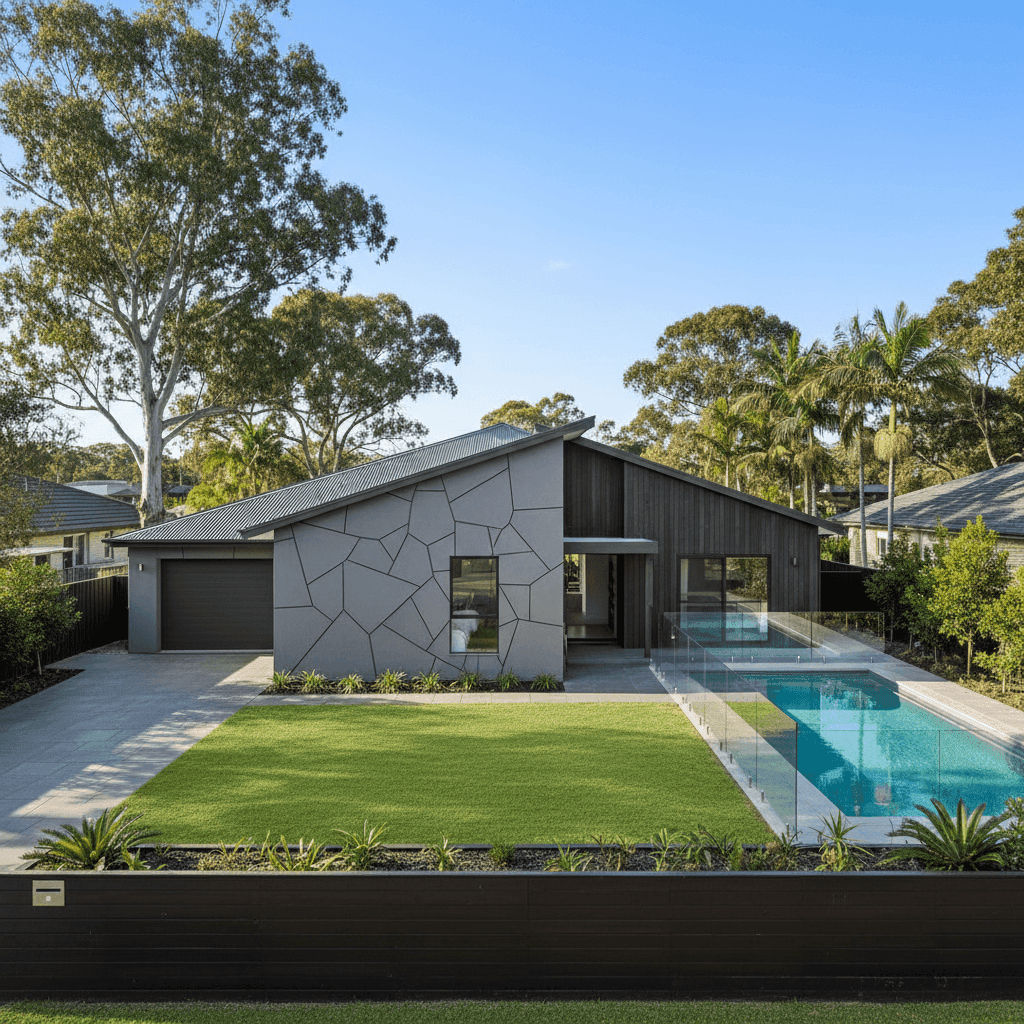

Manly Vale is one of Sydney's most desirable Northern Beaches suburbs — a leafy, coastal pocket in postcode 2093 where generous block sizes and established homes are the norm. For owners of large free standing homes in this area, getting the right home and contents insurance at a fair price is no small task. This article breaks down a real insurance quote for a substantial Manly Vale property and puts the numbers in context so you can make a more informed decision.

---

Is This Quote Fair?

The quote in question comes in at $6,702 per year (or $642 per month) for a combined home and contents policy, covering a building sum insured of $1,815,000 and contents valued at $440,000. Both the building and contents excess are set at $1,000 — a standard arrangement for policies at this level.

Our price rating for this quote is CHEAP — meaning the premium sits below the average for comparable properties. That's a meaningful result, particularly for a home of this size and value. A 10-bedroom, 5-bathroom free standing home built in 1965 with a pool and ducted climate control represents a significant asset, and insuring it adequately at a below-average rate is genuinely good value.

To put it plainly: if you're a Manly Vale homeowner receiving a quote in this range for this level of cover, you're doing better than most.

---

How Manly Vale Compares

Understanding where your premium sits relative to broader benchmarks helps you gauge whether you're being treated fairly by your insurer. Here's how this quote stacks up:

| Benchmark | Annual Premium |

|---|---|

| This Quote | $6,702 |

| Northern Beaches LGA Average | $3,266 |

| NSW State Average | $9,528 |

| NSW State Median | $3,770 |

| National Average | $5,347 |

| National Median | $2,764 |

A few things stand out here. The NSW state average of $9,528 per year is notably high — well above both the national average of $5,347 and this quote. That gap reflects the elevated risk profile of many NSW coastal and urban properties, where extreme weather events, flooding, and storm damage are factored heavily into pricing.

The Northern Beaches LGA average of $3,266 is lower than this quote, but it's important to remember that averages across a council area include a wide range of property types — smaller homes, units, and townhouses all pull that figure down. A 457 sqm, 10-bedroom home with a pool naturally attracts a higher premium than a typical two-bedroom cottage in the same postcode.

For detailed suburb-level statistics and benchmarks for Manly Vale, you can explore the full data on CoverClub.

---

Property Features That Affect Your Premium

Several characteristics of this property play a direct role in how insurers calculate the premium. Here's what matters most:

Size and Age

At 457 sqm, this is a large home by any measure. Rebuild costs scale with size, which is why the $1,815,000 building sum insured is appropriate — and why the premium is higher than a typical suburban home. The 1965 construction year is also relevant: older homes can carry higher risk due to ageing plumbing, wiring, and structural elements, though a well-maintained mid-century home on a slab foundation can still be very insurable.

Roof and Walls

The steel/Colorbond roof is generally viewed favourably by insurers. Colorbond is durable, fire-resistant, and performs well in high-wind conditions — all factors that can moderate risk. The "other" external wall classification may introduce some uncertainty into underwriting, as non-standard materials can vary significantly in terms of fire resistance and structural resilience.

Pool

A swimming pool adds both value and liability to a property. Insurers factor in the cost of pool repair or replacement, as well as any associated liability risks. Homeowners with pools should confirm their policy explicitly covers pool infrastructure and check whether public liability limits are sufficient.

Ducted Climate Control

Ducted air conditioning systems are expensive to repair or replace and are typically included in the building sum insured. At this property's scale, that's a meaningful line item. Ensuring the sum insured reflects the full replacement cost of these systems is important — underinsurance is a common and costly mistake.

No Cyclone Risk

Manly Vale is not classified as a cyclone risk area, which removes one of the more significant premium loading factors that affect properties in northern Queensland and parts of WA. This contributes to the relatively competitive pricing seen here.

---

Tips for Homeowners in Manly Vale

1. Review your sum insured annually Construction costs have risen sharply in recent years. A building sum insured that was accurate two years ago may no longer reflect the true cost of rebuilding your home. Use a quantity surveyor or your insurer's calculator to check you're not underinsured — especially for a home of this size and age.

2. Document your contents thoroughly With $440,000 in contents cover, you'll want a detailed home inventory. Photograph valuables, keep receipts where possible, and store records securely off-site or in the cloud. This makes the claims process far smoother if the worst happens.

3. Ask about policy inclusions for your pool and HVAC Not all policies automatically cover pool equipment or ducted systems under the standard building definition. Clarify with your insurer exactly what's included — and what's not — before you sign.

4. Compare quotes before renewal Even if your current premium is rated as cheap, the market changes. Insurers reprice risk regularly, and a quote that's competitive today may not be next year. Comparing home insurance quotes on CoverClub takes minutes and could save you hundreds — or confirm you're already on the best deal available.

---

Ready to Compare?

Whether you're reviewing an existing policy or shopping for cover for the first time, CoverClub makes it easy to see how your quote stacks up. Enter your address at CoverClub to get a personalised comparison and find out if you're paying a fair price for your Manly Vale home.