If you own a free standing home in Mansfield, VIC 3722, you already know it's one of regional Victoria's most scenic and sought-after addresses — nestled at the foot of the Victorian Alps, surrounded by bushland, and a gateway to Mount Buller. But that lifestyle comes with its own insurance considerations. This article breaks down a real home and contents insurance quote for a four-bedroom property in the area, examines whether the price stacks up, and offers practical tips to help Mansfield homeowners get better value on their cover.

---

Is This Quote Fair?

The quote in question sits at $7,081 per year (or $679/month) for combined home and contents insurance, covering a building sum insured of $1,100,000 and contents valued at $180,000. The building excess is $2,000 and the contents excess is $1,000.

Our price rating for this quote is Expensive — above average when benchmarked against comparable properties in the area.

To put that in perspective:

- The suburb average for Mansfield (postcode 3722) is just $2,149/yr, and the median sits at $1,953/yr

- Even at the 75th percentile — meaning 75% of quotes in the suburb are cheaper — the figure is only $2,678/yr

- This quote comes in at more than 2.6 times the suburb average

That's a significant gap, and it warrants a closer look at what's driving the price up — which we'll get to shortly.

---

How Mansfield Compares

Understanding where Mansfield sits in the broader insurance landscape helps frame just how unusual this quote is. You can explore the full local data on the Mansfield VIC 3722 insurance stats page.

| Benchmark | Average Premium |

|---|---|

| Mansfield (suburb) | $2,149/yr |

| Mansfield (median) | $1,953/yr |

| Victoria (state average) | $3,000/yr |

| Victoria (state median) | $2,718/yr |

| National average | $5,347/yr |

| National median | $2,764/yr |

| LGA (Unincorporated Vic) | $4,336/yr |

Interestingly, Mansfield's local premiums are well below both the Victorian and national averages — suggesting that, in general, insurers don't view this postcode as especially high-risk compared to the broader market. You can compare Victoria's figures against other states on the VIC insurance stats page, or zoom out further on the national insurance stats page.

The fact that this particular quote sits at $7,081 — above even the national average of $5,347 — points strongly to property-specific factors rather than location risk alone being the primary driver of cost.

---

Property Features That Affect Your Premium

Several characteristics of this property are likely pushing the premium above what a typical Mansfield home would attract. Here's what insurers are likely weighing up:

High Building Sum Insured

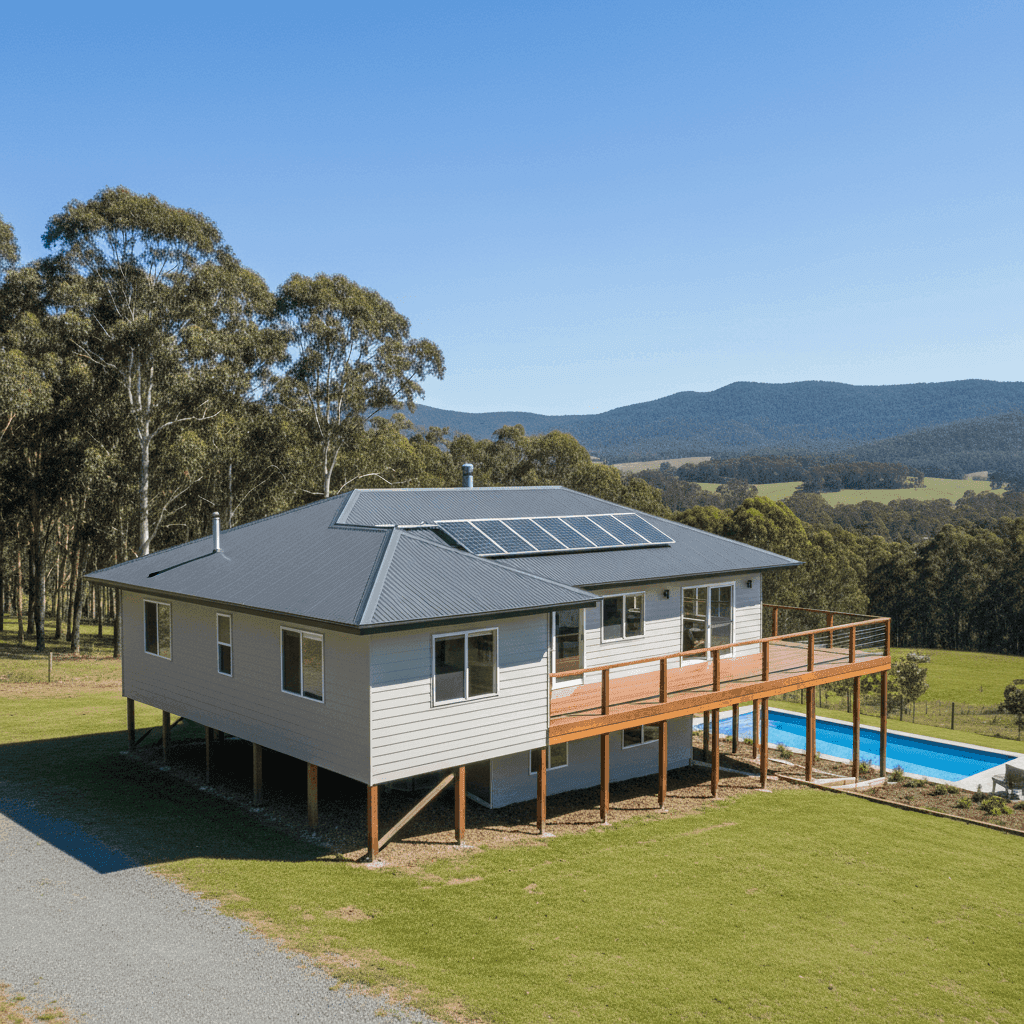

At $1,100,000, the building sum insured is substantial. This is the single biggest lever on any building insurance premium — the more it costs to rebuild, the more you pay to insure it. For a 214 sqm home, this equates to roughly $5,140 per sqm, which is on the higher end and may reflect premium finishes, the elevated construction style, or regional rebuild cost premiums.

Elevated Foundation on Stumps

This home sits on stumps and is elevated by at least one metre. While this style of construction offers excellent airflow and can reduce flood risk, it also increases rebuild complexity and cost. Insurers factor in the additional labour and materials required for elevated homes, which flows through to the premium.

Hardiplank/Hardiflex Walls and Colorbond Roof

Fibre cement cladding (Hardiplank/Hardiflex) is generally considered a solid, fire-resistant material — a meaningful advantage in a bushland-adjacent area like Mansfield. A steel Colorbond roof is similarly durable and low-maintenance. These materials may actually work in the homeowner's favour compared to timber weatherboard, but they don't eliminate risk entirely.

Timber and Laminate Flooring

Timber and laminate floors can be costly to replace and are susceptible to water damage. Insurers price this in, particularly for elevated homes where underfloor plumbing or weather exposure can become a factor.

Pool, Solar Panels, and Ducted Climate Control

Each of these additions increases the replacement value of the property and introduces specific risks. Swimming pools carry liability considerations. Solar panel systems — particularly on a roof — can be expensive to replace and may be damaged in storms or hail events. Ducted climate control systems are a significant fixed asset that adds to contents or building value depending on how they're classified.

Bushfire Proximity

While Mansfield is not designated a cyclone risk area, it sits in a region with elevated bushfire exposure. The Victorian Alps surrounds and the broader Mansfield Shire have experienced significant fire events historically. Many insurers apply loadings for properties in or near bushfire-prone zones, even when the construction materials are relatively fire-resistant.

---

Tips for Homeowners in Mansfield

1. Review Your Sum Insured Carefully

The $1,100,000 building sum insured may be accurate — or it may be over-estimated. Use a building cost calculator to check whether your sum insured reflects realistic rebuild costs for your area and construction type. Being over-insured means paying more premium than necessary, while being under-insured creates a different set of risks.

2. Shop Around — Seriously

With the suburb median sitting at $1,953/yr and this quote at $7,081/yr, there is clearly significant variation between insurers for properties in this postcode. Different insurers weight risk factors differently, and a property with a pool, solar panels, and elevated stumps will be priced very differently across the market. Compare quotes at CoverClub to see what multiple insurers would charge for your specific home.

3. Consider Your Excess Strategy

This policy carries a $2,000 building excess and $1,000 contents excess. Opting for a higher voluntary excess can meaningfully reduce your annual premium. If you have sufficient savings to cover a larger out-of-pocket amount in the event of a claim, increasing your excess is one of the most straightforward ways to lower your ongoing cost.

4. Maintain Bushfire Preparedness

In bushfire-prone areas like Mansfield, some insurers offer better terms to homeowners who actively maintain defensible space around their property — clearing gutters, trimming overhanging branches, and keeping grass short. Beyond the insurance benefit, it's simply good practice in this environment. Check with your insurer whether a documented bushfire preparedness plan affects your premium or policy terms.

---

Ready to Find a Better Rate?

Whether this quote represents your current policy or one you've just received, it's worth knowing what else is out there. CoverClub makes it easy to compare home and contents insurance quotes across multiple insurers — so you can see whether you're paying a fair price or leaving money on the table.