Manunda is a well-established residential suburb sitting just west of Cairns CBD in Far North Queensland. It's home to a mix of older character homes and more modern builds, many of which share a common challenge: navigating home insurance in one of Australia's most weather-exposed regions. This article analyses a real home and contents insurance quote for a four-bedroom, two-bathroom free standing home in Manunda (postcode 4870), breaking down what's driving the cost and what homeowners can do about it.

---

Is This Quote Fair?

The quote in question sits at $9,632 per year (or $916 per month) for combined home and contents cover, with a building sum insured of $919,000 and contents valued at $50,000. Both the building and contents excess are set at $1,000.

Our price rating for this quote is Expensive (Above Average) — and the data backs that up when you look at the local suburb picture. The suburb average for Manunda sits at just $4,486 per year, with a median of $4,250. That means this quote is more than double the typical premium paid by other Manunda homeowners in our sample.

However, context matters enormously here. When you zoom out to the state level, the Queensland average premium is $9,129 per year — meaning this quote is actually tracking quite close to the QLD state average. And at the LGA level, the Cairns average is a striking $12,404 per year, which puts this quote well below what many Cairns homeowners are paying.

So is it fair? The honest answer is: it depends on what you're comparing it to. Against the suburb sample, it looks steep. Against the broader Cairns LGA, it's actually on the lower end. The property's specific characteristics — particularly its cyclone risk exposure and higher-than-average building sum insured — go a long way toward explaining the gap.

---

How Manunda Compares

Here's a snapshot of how this quote stacks up across different benchmarks:

| Benchmark | Premium |

|---|---|

| This Quote | $9,632/yr |

| Manunda Suburb Average | $4,486/yr |

| Manunda Suburb Median | $4,250/yr |

| QLD State Average | $9,129/yr |

| QLD State Median | $3,903/yr |

| National Average | $5,347/yr |

| National Median | $2,764/yr |

| Cairns LGA Average | $12,404/yr |

It's worth noting that the national median of $2,764 is dramatically lower than what Queenslanders — and especially Far North Queenslanders — are paying. This reflects the outsized impact of natural hazard risk on premiums in tropical and cyclone-prone regions. Homeowners in southern states benefit from far lower catastrophe exposure, which keeps their premiums comparatively modest.

The gap between the QLD average ($9,129) and the QLD median ($3,903) is also telling. It suggests a relatively small number of high-risk properties are pulling the average up significantly — and properties in Cairns and surrounds are almost certainly among them.

---

Property Features That Affect Your Premium

Several characteristics of this property have a direct bearing on the premium quoted.

Cyclone Risk Area

This is the single biggest factor. Manunda sits within a designated cyclone risk zone, and insurers price this in heavily. Cyclone damage claims can be catastrophic in scale, and the reinsurance costs that underpin these policies are substantial. Homeowners in this region should expect to pay a significant loading compared to properties in southern states — this is simply the cost of living in Far North Queensland.

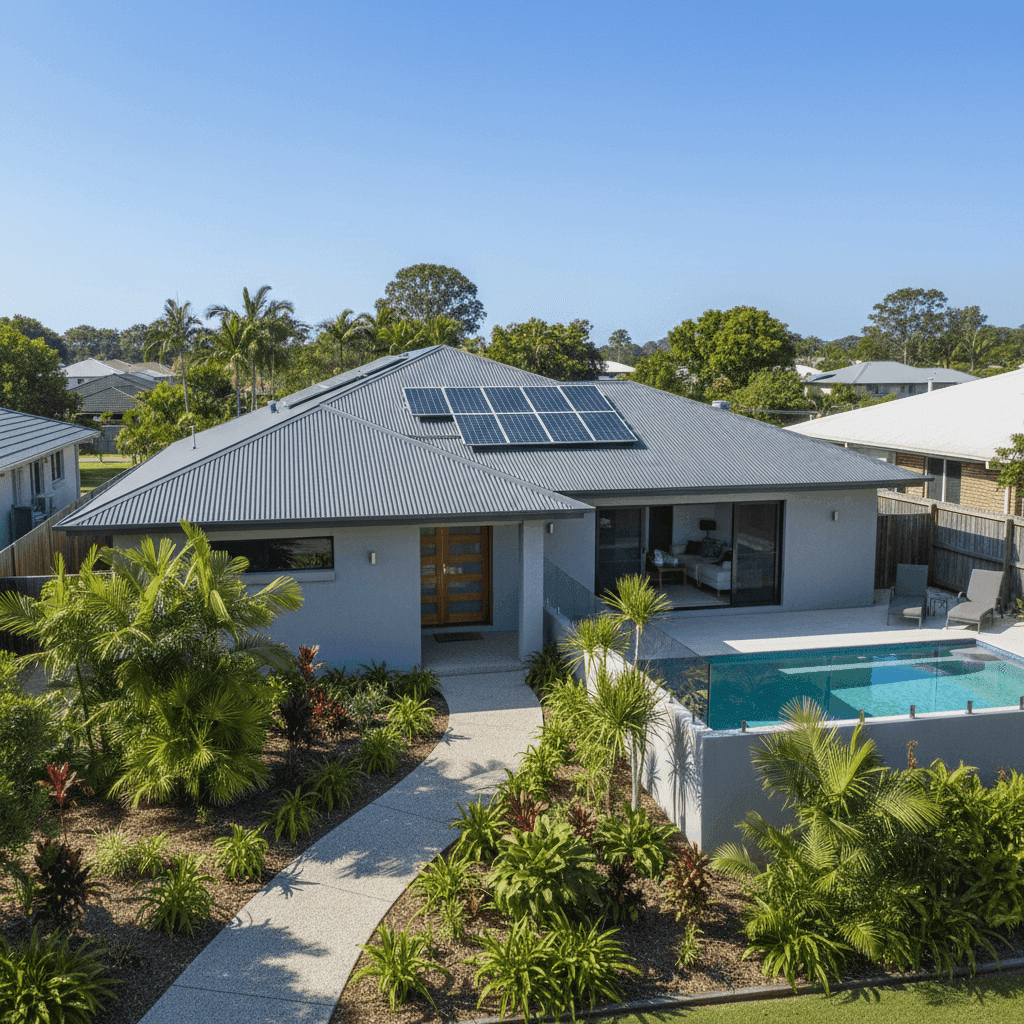

Building Sum Insured: $919,000

A building sum insured of $919,000 is on the higher side, even for a 214 sqm home. The sum insured represents the cost to fully rebuild the property from scratch — including demolition, materials, labour, and professional fees. In Cairns, construction costs are elevated due to the requirement for cyclone-rated building standards, which adds to rebuild costs. That said, it's worth periodically reviewing whether your sum insured accurately reflects current rebuild costs — both under- and over-insuring carry their own risks.

Concrete Walls & Steel/Colorbond Roof

Concrete external walls are generally viewed favourably by insurers as they offer strong resistance to wind and impact damage. Similarly, a steel Colorbond roof is a practical and durable choice in cyclone-prone areas, though it can be susceptible to wind uplift if not properly secured. These construction materials may offer some premium benefit compared to timber-framed or fibrous cement alternatives.

Slab Foundation & Tile Flooring

A concrete slab foundation is a stable and common choice in Queensland, and tile flooring throughout is both practical and relatively low-risk from an insurance perspective. Neither of these features is likely to attract a significant loading.

Pool, Solar Panels & Ducted Climate Control

The presence of a swimming pool adds to the contents and liability considerations of the policy. Solar panels represent an additional asset that needs to be covered — and in a cyclone zone, panels can become projectiles or sustain significant damage in a major weather event. Ducted climate control systems are expensive to repair or replace and contribute to the overall insured value of the home's fixtures and fittings.

---

Tips for Homeowners in Manunda

1. Shop Around — Seriously

With a premium this size, even a 10–15% saving translates to $960–$1,445 back in your pocket each year. Insurers price cyclone risk differently, and there can be meaningful variation between quotes for the same property. Use a comparison tool like CoverClub to see multiple quotes side by side.

2. Review Your Building Sum Insured

Make sure your $919,000 sum insured reflects a genuine rebuild cost estimate — not just the market value of your home. Tools like the Cordell Sum Sure Calculator can help you arrive at a more accurate figure. Overinsuring means you're paying more premium than necessary; underinsuring means you could face a shortfall when you need it most.

3. Consider Cyclone Mitigation Improvements

Some insurers offer premium discounts for homes that have undergone cyclone mitigation works — such as roof tie-down retrofits, impact-resistant shutters, or other structural improvements. If your 1985-built home hasn't been assessed recently, it may be worth exploring what upgrades could both protect your property and reduce your insurance costs.

4. Check Your Excess Options

Both the building and contents excesses on this policy are set at $1,000. Opting for a higher voluntary excess — say, $2,500 or $5,000 — can meaningfully reduce your annual premium. Just make sure you're comfortable covering that amount out of pocket in the event of a claim.

---

Compare Your Options with CoverClub

Whether you're a long-time Manunda resident or new to the area, it pays to make sure you're not overpaying for your home insurance. CoverClub makes it easy to compare quotes from multiple insurers in minutes, with transparent pricing and no hidden fees. Get a quote today and see how much you could save — or simply confirm that your current cover is genuinely competitive.

For more local data, visit the Manunda suburb insurance stats page or explore Queensland-wide insurance trends to better understand what's driving premiums in your area.