Maribyrnong is one of Melbourne's most sought-after inner-western suburbs — a vibrant, riverside community that blends period charm with contemporary living. For owners of free standing homes in this postcode, understanding what drives home insurance costs is just as important as finding the right cover. This article breaks down a real home and contents insurance quote for a four-bedroom property in Maribyrnong (VIC 3032), comparing it against local, state, and national benchmarks to help you make a more informed decision.

---

Is This Quote Fair?

The annual premium for this property comes in at $2,765 per year (or approximately $261 per month), covering both building and contents under a combined Home and Contents policy. The building is insured for $1,130,000 and contents for $249,000, with a $1,000 excess applying to each.

Our price rating for this quote is FAIR — Around Average, which is a reasonable outcome for a property of this size and specification. It sits comfortably within the middle of the market for Maribyrnong, neither alarmingly high nor suspiciously low. Given the above-average fittings quality and the relatively generous sum insured, a premium in this range reflects what insurers would typically price for a well-appointed, modern home in an established Melbourne suburb.

That said, "fair" doesn't necessarily mean "the best available." It simply means this quote is broadly in line with what comparable households are paying — and there may still be room to improve on it with the right comparison.

---

How Maribyrnong Compares

To put this quote in proper context, here's how the $2,765 annual premium stacks up across different benchmarks:

| Benchmark | Premium |

|---|---|

| This Quote | $2,765/yr |

| Maribyrnong Suburb Average | $3,178/yr |

| Maribyrnong Suburb Median | $3,442/yr |

| Maribyrnong 25th Percentile | $1,887/yr |

| Maribyrnong 75th Percentile | $4,226/yr |

| VIC State Average | $3,000/yr |

| VIC State Median | $2,718/yr |

| National Average | $5,347/yr |

| National Median | $2,764/yr |

This quote sits below both the suburb average ($3,178) and the suburb median ($3,442), which is a positive sign. It also comes in slightly below the Victorian state average of $3,000 per year. Compared to the national average of $5,347, the premium looks very competitive — though it's worth noting that the national figure is skewed upward by high-risk regions such as cyclone-prone areas in Queensland and the Northern Territory, which tend to attract significantly higher premiums.

Interestingly, this quote is almost exactly on the national median of $2,764, suggesting it reflects a broadly typical cost for a home and contents policy across Australia when extreme-risk areas are excluded from the picture.

The Maribyrnong suburb insurance data shows a reasonably wide spread between the 25th percentile ($1,887) and the 75th percentile ($4,226), which tells us that premiums in this area can vary significantly depending on the insurer, the property, and the level of cover chosen. Explore VIC state insurance statistics and national insurance data for broader context.

---

Property Features That Affect Your Premium

Several characteristics of this property will have influenced how insurers assessed and priced the risk. Here's what matters most:

Construction & Materials

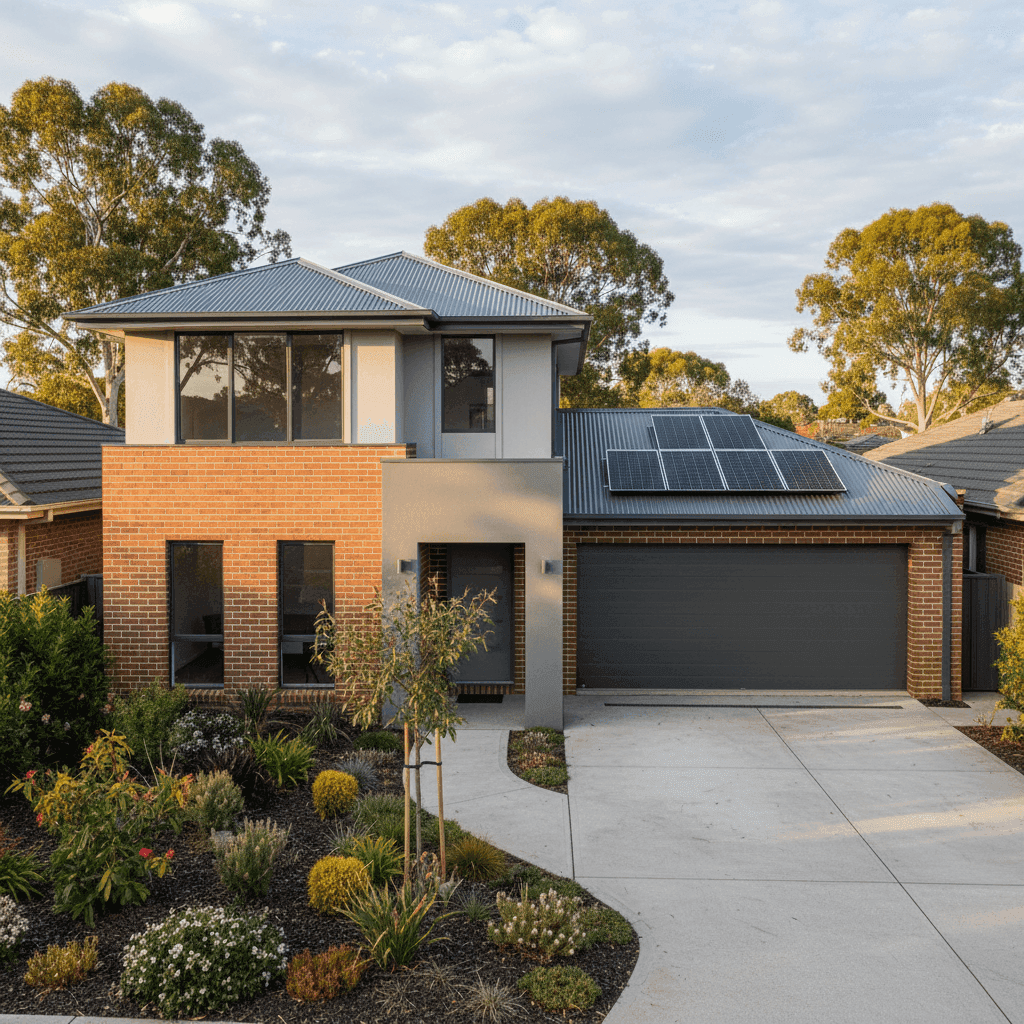

Built in 2003, this home benefits from relatively modern construction standards — a factor insurers view favourably. The brick veneer external walls offer solid fire resistance and structural durability, generally attracting lower premiums than timber-framed weatherboard homes. The Colorbond steel roof is another plus: it's lightweight, resistant to corrosion, and performs well in Melbourne's variable weather conditions.

Foundation & Flooring

A concrete slab foundation is considered low-risk by most insurers, as it's less susceptible to subsidence and pest damage compared to older pier-and-beam or timber subfloor systems. The timber and laminate flooring throughout the home contributes to the contents valuation and may influence replacement cost estimates in the event of a claim.

Above-Average Fittings

The property's above-average fittings quality — think stone benchtops, quality appliances, premium fixtures — is a meaningful factor in determining the building sum insured. Higher-quality finishes cost more to repair or replace, which is reflected in both the $1,130,000 building sum insured and the overall premium.

Solar Panels

The presence of solar panels adds to the replacement value of the property and is an increasingly common feature that insurers now factor into their assessments. It's important to confirm that your policy explicitly covers solar panels as part of the building, including damage from storms, hail, or electrical faults.

Ducted Climate Control

A ducted heating and cooling system is a significant fixed asset that forms part of the building's insurable value. These systems can be expensive to repair or replace, and their inclusion in the building sum insured is essential to avoid being underinsured.

No Pool, No Cyclone Risk

The absence of a swimming pool removes a common liability exposure, and the property's location outside any designated cyclone risk zone means it avoids the premium loadings that affect many properties in northern Australia.

---

Tips for Homeowners in Maribyrnong

Whether you're reviewing your existing policy or shopping for the first time, here are some practical steps to make sure you're getting the right cover at a competitive price.

- Check your building sum insured regularly. Construction costs in Melbourne have risen sharply in recent years. A sum insured set even two or three years ago may no longer be sufficient to fully rebuild your home. Use a building replacement cost calculator or speak with a quantity surveyor to verify your figure.

- Don't underestimate your contents. At $249,000, this policy's contents value is substantial — and rightly so for a well-appointed four-bedroom home. Walk through each room and take stock of furniture, electronics, clothing, jewellery, and appliances. Many homeowners are surprised by how quickly the total adds up.

- Review your excess settings. A $1,000 excess on both building and contents is fairly standard, but increasing your excess can meaningfully reduce your annual premium. If you have a solid emergency fund and are unlikely to make small claims, a higher excess could be a smart trade-off.

- Compare quotes annually. The insurance market shifts each year, and loyalty doesn't always pay. Even if your current insurer has treated you well, running a fresh comparison at renewal time ensures you're not quietly drifting above market rates. Maribyrnong's wide premium spread — from under $1,900 to over $4,200 — shows just how much prices can differ between providers.

---

Ready to Compare?

If you own a home in Maribyrnong or anywhere across Victoria, it pays to see what the broader market has to offer. CoverClub makes it easy to compare home and contents insurance quotes side by side, so you can find cover that suits your property without overpaying. Get a quote today at CoverClub and see how your premium stacks up.