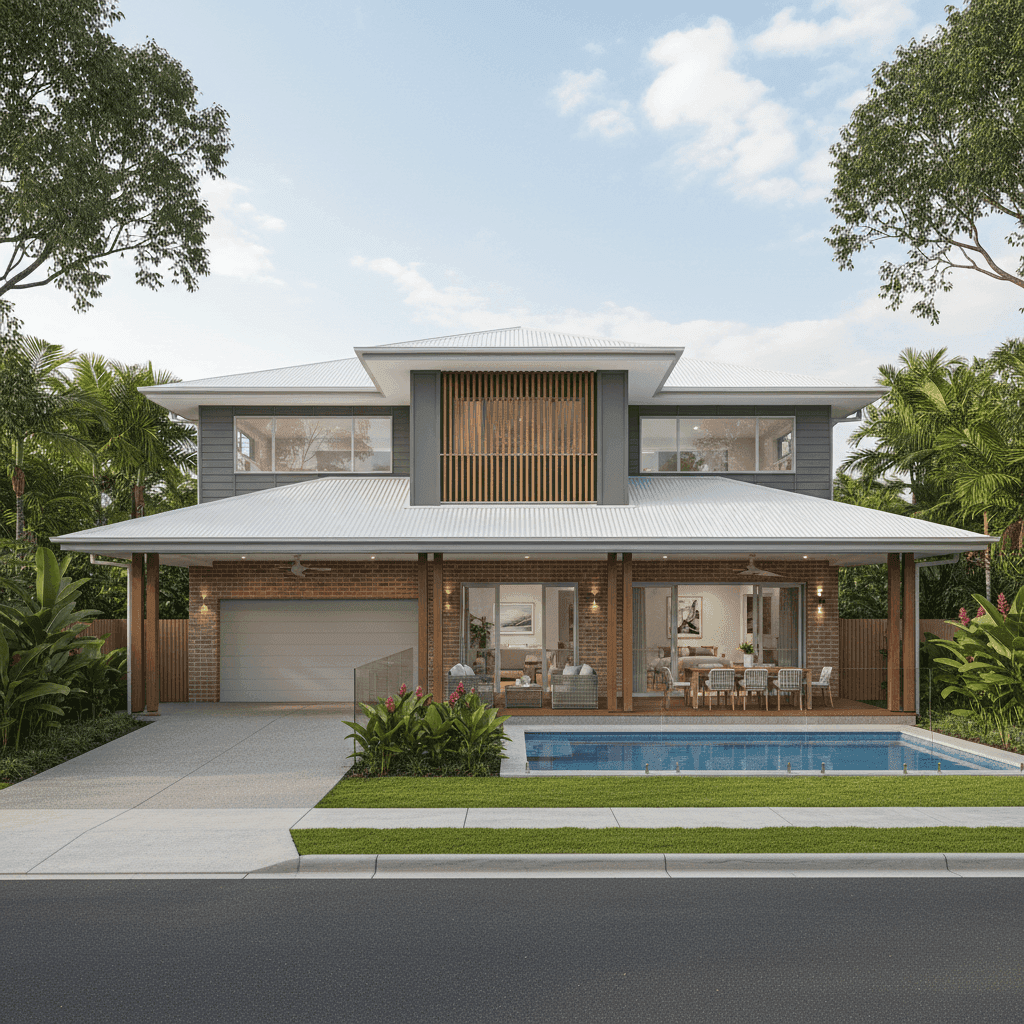

If you own a free standing home in Maroochydore, QLD 4558, you already know the Sunshine Coast lifestyle comes with plenty of perks — coastal breezes, a booming local economy, and a strong sense of community. But with great real estate comes the responsibility of protecting it properly. This article breaks down a real home and contents insurance quote for a three-bedroom, two-bathroom brick veneer home in Maroochydore, compares it against local, state, and national benchmarks, and offers practical tips to help you get the most out of your cover.

---

Is This Quote Fair?

The quote in question comes in at $3,485 per year (or $334/month) for combined home and contents insurance, covering a building sum insured of $850,000 and $60,000 worth of contents. Both the building and contents excess are set at $1,000.

Our pricing engine rates this quote as Fair — Around Average, and the data backs that up.

When you look at the suburb-level insurance data for Maroochydore, the median premium across 47 quotes sits at $4,607/yr — meaning this quote actually comes in below the local median by over $1,100. It also falls just above the suburb's 25th percentile of $3,399/yr, which means roughly three-quarters of comparable quotes in the area cost more.

The suburb's average premium, however, is a striking $48,776/yr — a figure heavily skewed by high-value outliers at the upper end of the market. The 75th percentile sits at $15,269/yr, which signals that a meaningful portion of Maroochydore properties attract significantly higher premiums, likely due to flood exposure, elevated rebuild costs, or higher-value homes. Against that backdrop, $3,485/yr looks very competitive.

---

How Maroochydore Compares

Zooming out to a broader view, this quote holds up well across every comparison point.

| Benchmark | Average | Median |

|---|---|---|

| Maroochydore (4558) | $48,776/yr | $4,607/yr |

| Queensland | $9,129/yr | $3,903/yr |

| Sunshine Coast LGA | $7,249/yr | — |

| National | $5,347/yr | $2,764/yr |

You can explore the full Queensland insurance stats here and national averages here.

A few things stand out in this comparison:

- Queensland premiums are high. The state median of $3,903/yr is already 41% above the national median of $2,764/yr — a reflection of Queensland's elevated exposure to cyclones, storms, flooding, and hail events.

- The Sunshine Coast LGA average of $7,249/yr is well above the national average, underscoring the region's risk profile and the premium real estate values that drive higher rebuild costs.

- This quote at $3,485/yr sits comfortably below both the QLD and Sunshine Coast LGA averages, and only slightly above the national median — a solid outcome for a Sunshine Coast property.

---

Property Features That Affect Your Premium

Several characteristics of this particular property work in the homeowner's favour when it comes to pricing.

New construction (2025): A brand-new home is one of the strongest premium reducers available. Modern builds must comply with current Australian building codes, which means better cyclone strapping, improved waterproofing, and more resilient structural design. Insurers reward this with lower risk assessments.

Brick veneer external walls: Brick veneer is a well-regarded construction type in the insurance world. It offers solid fire resistance and durability compared to timber or weatherboard, which can translate into more favourable underwriting terms.

Colorbond steel roof: Steel roofing is durable, low-maintenance, and performs well in high-wind conditions. Colorbond in particular is a popular choice for Queensland homes and is generally viewed positively by insurers.

Slab foundation with tile flooring: A concrete slab foundation is structurally sound and eliminates the sub-floor moisture and pest risks associated with older timber stumps. Combined with tile flooring, this setup is both durable and easy to assess for replacement cost purposes.

Elevated by at least 1 metre: This is a meaningful risk mitigator in Queensland, where flash flooding and storm surge can affect low-lying properties. An elevated home is less vulnerable to inundation, which insurers factor into flood and storm cover pricing.

Swimming pool: A pool adds value to the property and increases the contents/structure replacement cost slightly, but it's a standard feature in Queensland and well understood by insurers. It's unlikely to have a major impact on premiums for a property of this type.

Ducted climate control: Ducted air conditioning is a significant asset and adds to the overall replacement value of the home. It's worth ensuring your building sum insured accounts for the full cost of reinstalling a ducted system, which can run into tens of thousands of dollars.

No cyclone risk area: Despite being in Queensland, Maroochydore is not classified as a cyclone risk zone — a factor that meaningfully reduces premiums compared to properties in Far North Queensland or coastal areas north of Bundaberg.

---

Tips for Homeowners in Maroochydore

1. Review your building sum insured annually With a newly built home in 2025, construction costs and material prices can shift quickly. Your $850,000 sum insured should reflect the full cost to rebuild — not the market value of the land and property combined. Use a quantity surveyor or your insurer's rebuild calculator to verify this figure each year.

2. Don't underestimate contents value $60,000 in contents cover is a reasonable starting point, but it's easy to underestimate what you own. Walk through each room and tally up electronics, furniture, appliances, clothing, and valuables. Many homeowners find their actual contents value is higher than they initially thought — and being underinsured at claim time is a costly mistake.

3. Ask about bundling discounts Many insurers offer discounts when you hold both home and contents cover under the same policy — which this quote already does. But it's also worth asking whether bundling with car insurance or other policies could unlock further savings.

4. Consider the value of your excess Both excesses here are set at $1,000. Opting for a higher excess (say, $2,000 or $2,500) can reduce your annual premium noticeably. If your home is new, well-built, and in a lower-risk area, the likelihood of a small claim is reduced — making a higher excess a potentially smart trade-off.

---

Ready to Compare?

A "Fair" rating is a solid starting point, but it doesn't mean you can't do better. Insurance premiums vary significantly between providers, even for identical properties — so comparing quotes is always worth the effort.

Get a home insurance quote at CoverClub and see how your property stacks up in seconds. Whether you're a first-time buyer or a long-term Maroochydore local, finding the right cover at the right price starts with having the right data.