Maryborough, nestled in Queensland's Fraser Coast region, is a town rich in heritage architecture and classic Queensland character homes. For owners of a four-bedroom free standing home in this postcode, understanding the true cost of home insurance — and whether you're getting a fair deal — can make a significant difference to your household budget. This article breaks down a recent home and contents insurance quote for a property in Maryborough QLD 4650, comparing it against local, state, and national benchmarks.

---

Is This Quote Fair?

The quote in question comes in at $2,225 per year (or $219/month) for combined home and contents cover, with a building sum insured of $600,000 and contents valued at $100,000. The building excess sits at $3,000 and the contents excess at $1,000.

Our pricing analysis rates this quote as CHEAP — below average for the area. That's a meaningful finding. In a suburb where premiums can swing dramatically — from under $2,695 at the 25th percentile all the way to $13,043 at the 75th percentile — landing below the 25th percentile mark is a genuinely strong result.

To put it plainly: this quote is significantly more affordable than what most Maryborough homeowners are paying. It sits well beneath the suburb average of $7,129/yr and even comfortably below the suburb median of $4,008/yr. For a homeowner with this property profile, that's a potential saving of $1,783 compared to the median alone.

It's worth noting that the higher excess on the building ($3,000) does contribute to the lower premium — insurers typically reward policyholders who are willing to absorb more of the initial cost of a claim. That's a reasonable trade-off for many homeowners, particularly those who are financially positioned to cover smaller incidents out of pocket.

---

How Maryborough Compares

Maryborough's insurance market is notably more expensive than both the state and national norms, which makes this quote all the more impressive in context. Here's how the numbers stack up:

| Benchmark | Average Premium | Median Premium |

|---|---|---|

| Maryborough (4650) | $7,129/yr | $4,008/yr |

| Gympie LGA | $5,581/yr | — |

| Queensland | $4,547/yr | $3,931/yr |

| National | $2,965/yr | $2,716/yr |

You can explore the full Maryborough suburb insurance stats, Queensland state data, and national benchmarks on CoverClub.

The wide spread between Maryborough's 25th percentile ($2,695) and 75th percentile ($13,043) — a gap of over $10,000 — tells an important story. Insurance pricing in this area is highly variable, which strongly suggests that the specific characteristics of each property play a major role in how insurers assess risk. This is a suburb where shopping around is not just advisable — it's essential.

Queensland as a whole carries higher premiums than the national average, largely due to elevated weather-related risks including flooding, storms, and cyclone exposure in many parts of the state. Maryborough's averages sit above even the Queensland state average, reflecting localised risk factors in the Fraser Coast region.

---

Property Features That Affect Your Premium

Several characteristics of this particular property influence how insurers price the risk. Understanding these factors helps explain both the quote received and the broader premium landscape in Maryborough.

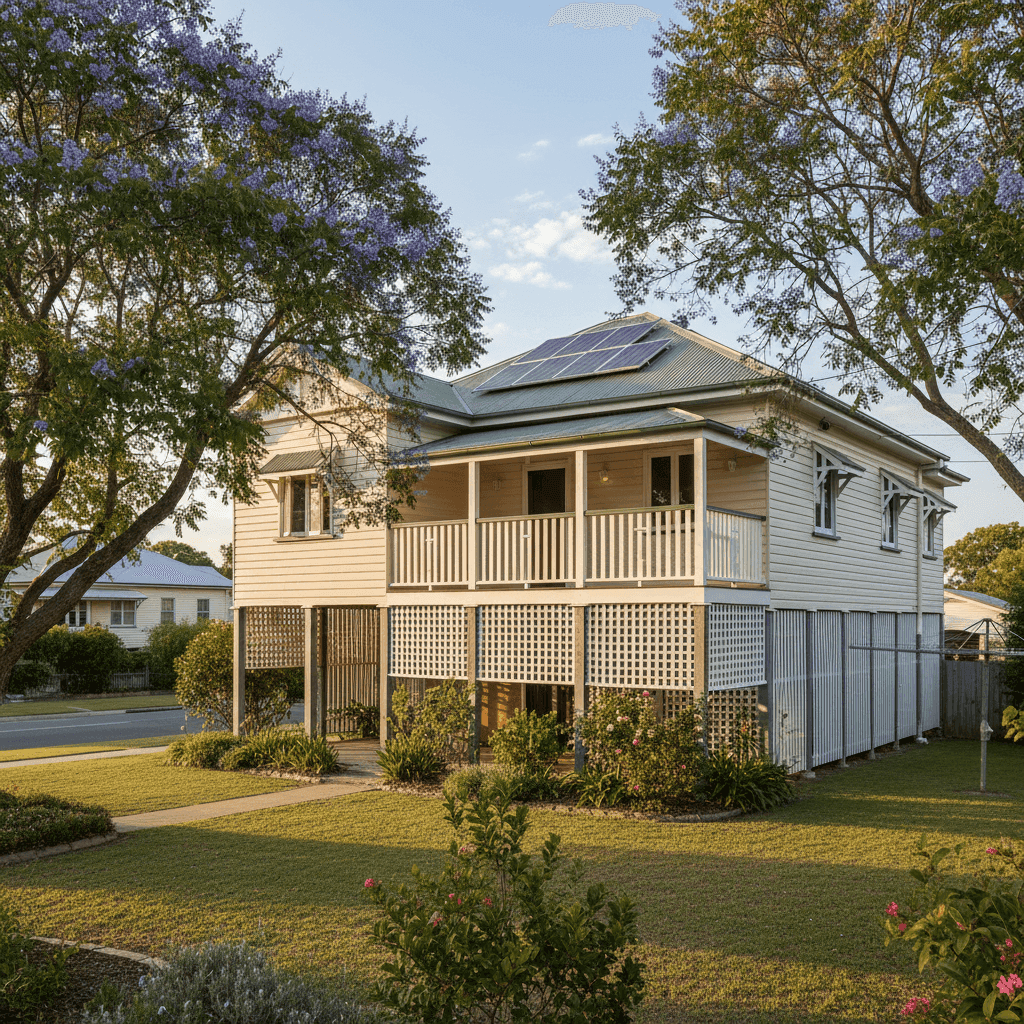

Weatherboard timber construction is one of the most significant variables. Older timber homes — particularly those built in or around 1968 — are generally considered higher risk by insurers due to their susceptibility to fire, rot, and the higher cost of like-for-like repairs. Sourcing matching weatherboard materials for heritage-style homes can be expensive, which is often reflected in building sum insured requirements.

Elevated on stumps is a classic feature of Queensland architecture, and in flood-prone areas it can actually work in a homeowner's favour. An elevation of at least one metre above ground level reduces the risk of inundation from minor flooding events, which some insurers reward with lower premiums. Given Maryborough's proximity to the Mary River, this is a particularly relevant feature.

Steel/Colorbond roofing is generally viewed favourably by insurers. It's durable, fire-resistant, and less prone to storm damage than older roofing materials like fibrous cement or terracotta tiles — all positives in a region that sees significant rainfall and storm activity.

Solar panels are an increasingly common feature and are worth flagging with your insurer. Most standard home policies cover solar panels as part of the building, but it's important to confirm this is the case and that the replacement value is adequately captured within your sum insured.

Construction year (1968) means the property is over 55 years old. Older homes may have ageing electrical systems, plumbing, or structural elements that can elevate risk in the eyes of underwriters. Keeping maintenance records up to date and addressing any known issues can support your position when renewing cover.

---

Tips for Homeowners in Maryborough

1. Review your sum insured annually. Building costs have risen sharply in recent years. A sum insured of $600,000 for a 139 sqm home may be appropriate today, but reconstruction costs — particularly for a heritage-style timber home — can escalate quickly. Use a building cost calculator each year at renewal to make sure you're not underinsured.

2. Confirm flood cover is included. Maryborough has experienced significant flood events historically, given its location near the Mary River. Standard home insurance policies don't always include flood cover by default — it may be an optional add-on or excluded entirely. Check your Product Disclosure Statement carefully and don't assume you're covered.

3. Shop around at every renewal. The enormous premium spread in this suburb (from $2,695 to $13,043) shows that insurers price this postcode very differently. The quote analysed here is well below average, but that won't always be the case. Comparing multiple quotes at renewal is the single most effective way to avoid overpaying. Get a fresh quote at CoverClub to see where you stand.

4. Maintain your timber home proactively. Insurers may ask about the condition of your roof, stumps, and external walls — particularly for older properties. Staying on top of maintenance (re-stumping, painting weatherboards, clearing gutters) not only protects your home but can also support your claim outcomes and potentially your premium at renewal.

---

Compare Your Own Quote

Whether you're a first-time buyer or a long-term Maryborough resident, it pays to know what the market looks like before you commit to a policy. CoverClub makes it easy to compare home and contents insurance quotes side by side, so you can see exactly how your premium stacks up against the suburb, state, and national averages.

Start comparing home insurance quotes today at CoverClub — it takes just a few minutes and could save you thousands.