If you own a free standing home in Maryborough, QLD 4650, you've probably noticed that home insurance premiums in regional Queensland can vary enormously — sometimes shockingly so. This article breaks down a real home and contents insurance quote for a 3-bedroom, 1-bathroom weatherboard home in Maryborough, comparing it against suburb, state, and national benchmarks so you can judge whether your own premium stacks up.

---

Is This Quote Fair?

The annual premium for this property came in at $6,138 per year (or $581/month), covering a building sum insured of $535,000 and contents valued at $52,500. The building excess is $1,000 and the contents excess $500.

Our price rating for this quote is FAIR — Around Average.

That assessment holds up when you look at the data. The suburb's 75th percentile premium sits at $6,579 per year, meaning this quote lands just inside the upper-middle range of what Maryborough homeowners are paying. It's well above the suburb median of $3,515, but it's also a fraction of the suburb average of $13,564 — a figure that's heavily skewed by a handful of very expensive outlooks in the area.

In practical terms, "fair" means you're not being gouged, but there's likely room to do better. Premiums in the 25th percentile for this suburb sit at $2,360 per year, which shows that some homeowners with comparable properties are paying considerably less. Whether that's achievable for this particular home depends on the features involved — and several of them do push the premium upward.

---

How Maryborough Compares

Maryborough sits in an interesting position when you zoom out to Queensland-wide insurance data and national benchmarks.

| Benchmark | Average Premium | Median Premium |

|---|---|---|

| Maryborough (4650) | $13,564/yr | $3,515/yr |

| Gympie LGA | $5,581/yr | — |

| Queensland | $9,129/yr | $3,903/yr |

| National | $5,347/yr | $2,764/yr |

A few things stand out here. The Maryborough suburb average of $13,564 is dramatically higher than both the Queensland and national averages — but the median tells a very different story. At $3,515, the suburb median is actually below the Queensland median of $3,903 and just above the national median of $2,764. This wide gap between average and median is a classic sign of a skewed distribution: most homeowners are paying moderate premiums, but a subset of properties attract extremely high quotes that pull the average up sharply.

The Gympie LGA average of $5,581 provides a useful middle-ground reference. This quote at $6,138 sits modestly above the LGA average, which is consistent with the property's specific risk profile (more on that below).

Queensland as a whole is one of Australia's most expensive states for home insurance, driven by flood, storm, and cyclone exposure across much of the state. Even though Maryborough is not classified as a cyclone risk area, it does sit in a region with significant weather event history, which keeps baseline premiums elevated compared to southern states.

---

Property Features That Affect Your Premium

Several characteristics of this property have a direct bearing on the premium, both positively and negatively.

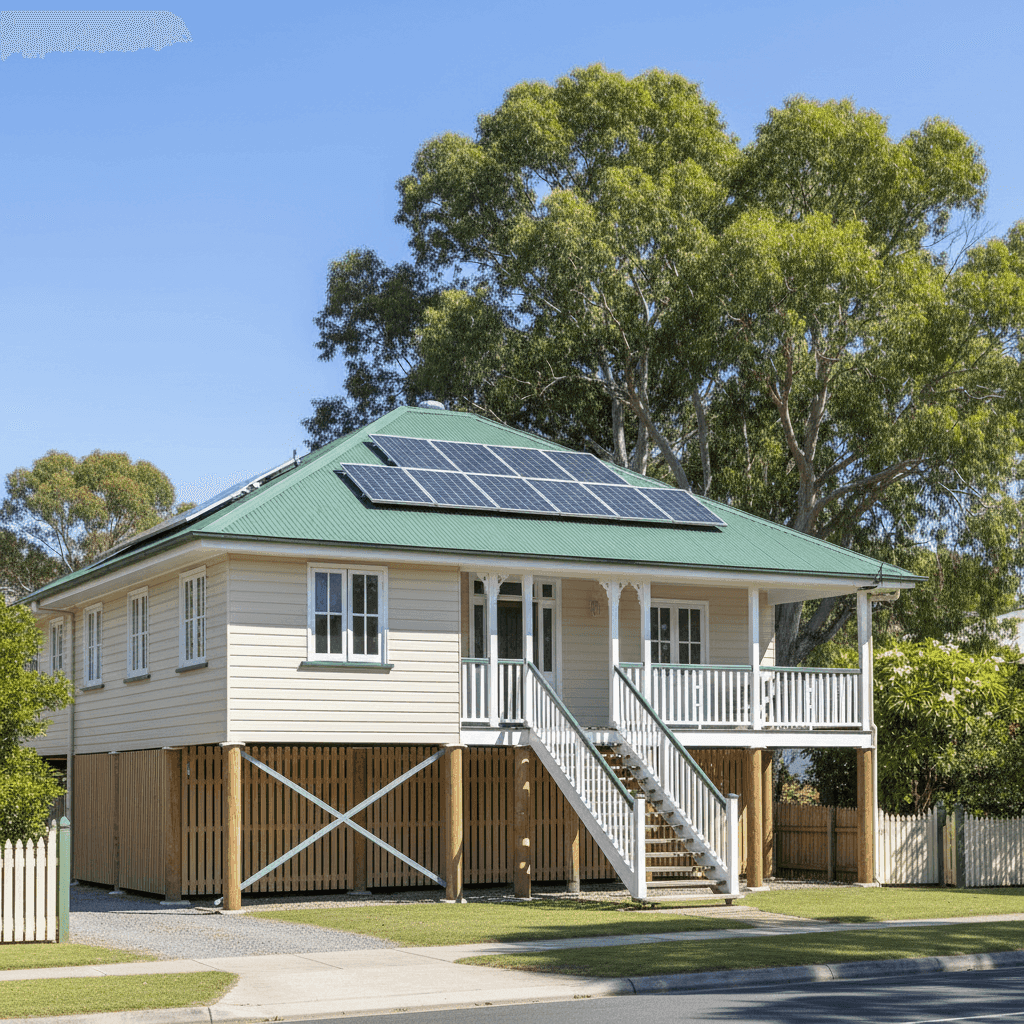

Weatherboard timber walls and timber flooring are among the most significant premium drivers for older Queensland homes. Timber is more susceptible to fire, termite damage, and storm impact than brick or rendered masonry, and insurers price this risk accordingly. Combined with a 1960 construction year, this property falls into an age bracket where wiring, plumbing, and structural integrity can be harder to assess — another factor that nudges premiums higher.

Elevated on stumps by at least 1 metre is a double-edged feature. On one hand, elevation offers meaningful protection against flood inundation, which is a genuine concern in the Fraser Coast region. On the other hand, stump foundations introduce their own risks — subfloor exposure, stump deterioration, and greater vulnerability to wind uplift — which some insurers treat cautiously.

The Colorbond steel roof is a relative positive. Steel roofing is durable, low-maintenance, and performs well in storm conditions compared to terracotta or concrete tiles, which can crack or dislodge. This likely provides a modest downward pressure on the premium.

Solar panels add replacement value to the building sum insured and can introduce specific risks (fire from inverter faults, panel damage from hail), so they contribute modestly to the overall cost. Similarly, ducted climate control adds to the insured value of fixtures and fittings within the home.

At 130 sqm, this is a modest-sized home, and the standard fittings quality means there are no luxury finishes inflating the rebuild cost beyond what the sum insured covers.

---

Tips for Homeowners in Maryborough

1. Review your building sum insured carefully. A sum insured of $535,000 for a 130 sqm weatherboard home built in 1960 may seem high, but rebuild costs in regional Queensland — factoring in demolition, materials, labour, and compliance with current building codes — can be substantial. Underinsurance is a significant risk; use a building cost calculator or speak to a quantity surveyor if you're unsure.

2. Shop around at renewal time. The spread of premiums in Maryborough is wide — from $2,360 at the 25th percentile to $6,579 at the 75th percentile. That range suggests different insurers are pricing this suburb's risk profile very differently. Comparing at least three to four quotes before renewing could save you hundreds of dollars annually.

3. Ask about flood and storm excess options. In regional Queensland, flood and storm damage excesses are often where the real cost lies. Some policies offer lower base premiums but carry hefty specific-event excesses. Make sure you understand exactly what your $1,000 building excess applies to — and whether separate flood or storm excesses apply on top.

4. Maintain your home proactively. Older weatherboard homes benefit enormously from regular upkeep — repainting to prevent moisture ingress, checking stump condition, keeping gutters clear, and ensuring the roof is free of rust or loose panels. Some insurers offer discounts for well-maintained properties, and documented maintenance can also support claims if damage does occur.

---

Compare Your Quote with CoverClub

Whether you're renewing an existing policy or insuring a new purchase, it pays to know where your premium sits relative to your neighbours. CoverClub makes it easy to compare home and contents insurance quotes for properties across Queensland and beyond, with real suburb-level data to help you make an informed decision. Enter your address today and see what the market looks like for your home.