If you own a free standing home in Maudsland, QLD 4210, you're likely no stranger to the question every homeowner eventually asks: am I paying too much for home insurance? Nestled in the Gold Coast hinterland, Maudsland is a sought-after suburb known for its spacious properties, acreage lifestyle, and proximity to the Gold Coast's urban amenities. But with larger homes and lifestyle features like pools and solar panels, insurance premiums can climb quickly. Let's break down what a recent quote looks like for a five-bedroom home in this postcode — and whether it represents fair value.

---

Is This Quote Fair?

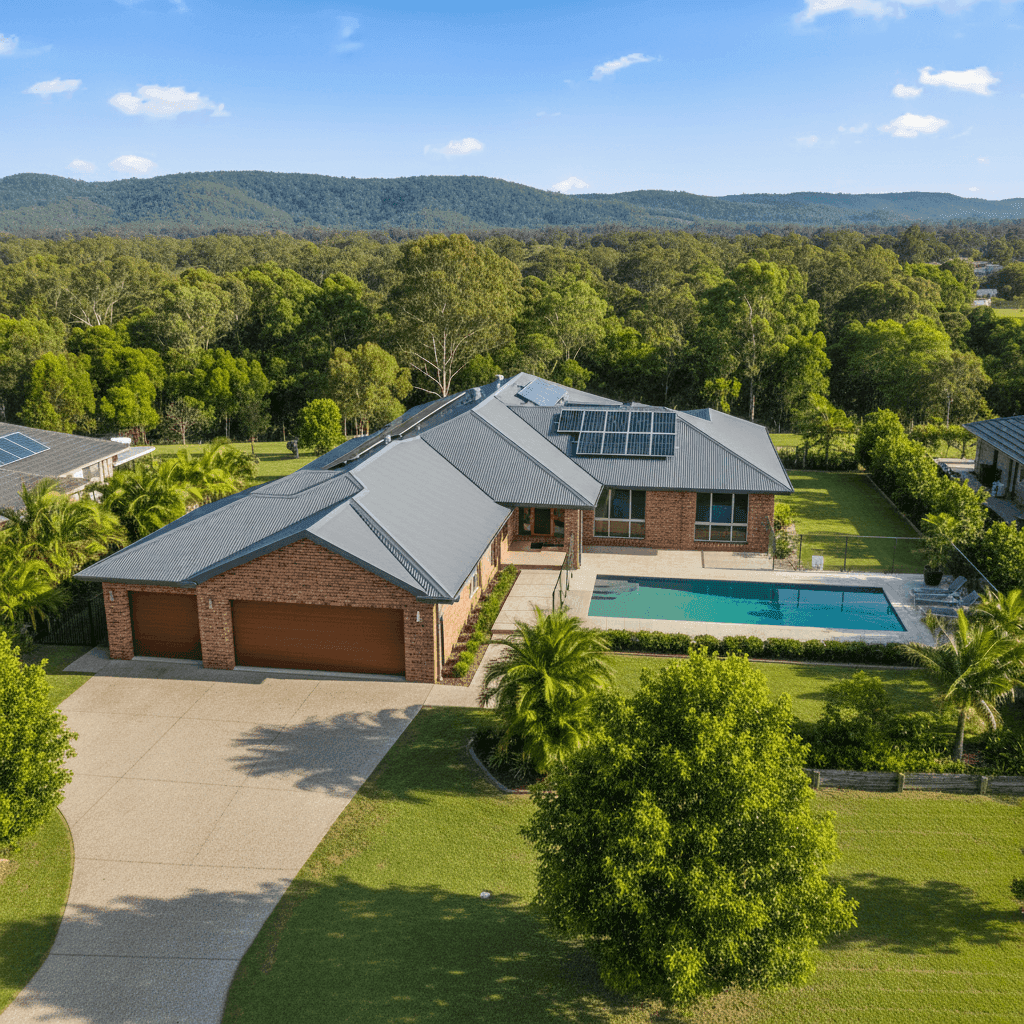

The quote in question covers a five-bedroom, three-bathroom free standing home with a building sum insured of $1,498,000 and contents valued at $77,000, returning an annual premium of $3,969 (or $374 per month). Both the building and contents excess sit at $5,000.

Our price rating for this quote is Expensive — above average for the Maudsland area.

To put that in context: the suburb average annual premium sits at $2,918, and the median is even lower at $2,479. This quote comes in roughly 36% above the suburb average and about 60% above the suburb median. It does fall within the upper quartile range (the 75th percentile for Maudsland is $3,686), but it exceeds even that benchmark — meaning this premium is higher than what roughly three-quarters of comparable quotes in the area are returning.

That said, it's worth remembering that this is a substantial property. A building sum insured of nearly $1.5 million is well above what many homes in the suburb would carry, and the combination of premium features — more on those shortly — does justify some loading above the local average.

---

How Maudsland Compares

Understanding where Maudsland sits in the broader insurance landscape helps put individual quotes in perspective. Here's a snapshot:

| Benchmark | Average Premium | Median Premium |

|---|---|---|

| Maudsland (4210) | $2,918/yr | $2,479/yr |

| Queensland | $9,129/yr | $3,903/yr |

| National | $5,347/yr | $2,764/yr |

| Gold Coast LGA | $8,161/yr | — |

A few things stand out here. Queensland's average premium of $9,129 is extraordinarily high — driven largely by Far North Queensland postcodes with severe cyclone exposure. Maudsland is not a designated cyclone risk area, which is a significant factor keeping local premiums lower than the state average. The Gold Coast LGA average of $8,161 similarly reflects the broader coastal and flood-risk exposure across the region, even if Maudsland itself sits in a more favourable risk category.

Compared to the national average of $5,347, this quote of $3,969 is actually below average — which is a useful reminder that "expensive for the suburb" doesn't necessarily mean expensive in absolute terms. Nationally, home and contents insurance has been rising sharply, and Maudsland homeowners are still faring better than many parts of the country.

You can explore full pricing data for this postcode at the Maudsland insurance stats page, compare it against Queensland-wide data, or view national benchmarks to see how your suburb stacks up.

---

Property Features That Affect Your Premium

Several characteristics of this particular home are likely contributing to a higher-than-average premium. Understanding these factors can help you have a more informed conversation with insurers.

High Building Sum Insured

At $1,498,000, the building cover is substantial. Rebuild costs in Queensland have risen significantly in recent years due to labour shortages and elevated material costs. For a 235 sqm home with quality fittings, this figure isn't unreasonable — but it is a primary driver of premium cost. Overinsuring, however, can be just as costly as underinsuring, so it's worth reviewing your sum insured with a quantity surveyor periodically.

Stump Foundation

Homes built on stumps are common in Queensland, particularly in areas with reactive soils or flood-prone land. Insurers may apply additional loading for stump foundations due to the increased risk of subsidence, movement, or damage from moisture and pests beneath the floor.

Timber and Laminate Flooring

Timber and laminate floors are more susceptible to water damage than tiles, which can influence how insurers price water-related claims risk. Given the Queensland climate, this is a factor worth noting.

Swimming Pool

A pool adds value to the property but also adds liability exposure and increases the cost of full replacement. Pool equipment, fencing, and surrounds all contribute to the overall insured value.

Solar Panels

Solar panel systems are now commonly included in building cover, but they represent a meaningful replacement cost — particularly for larger systems. Insurers factor this into building premiums, especially given hail risk in South East Queensland.

Ducted Climate Control

Ducted air conditioning systems are expensive to replace and repair. Their inclusion in the building's fixtures and fittings adds to the overall replacement cost calculation.

Brick Veneer Walls and Colorbond Roof

Brick veneer is generally viewed favourably by insurers — it's durable and fire-resistant. A steel Colorbond roof is also well-regarded for its resilience, particularly in storm-prone regions. These construction types typically attract more competitive premiums compared to timber weatherboard or tile roofs.

---

Tips for Homeowners in Maudsland

If your premium is coming in above the suburb average, there are several strategies worth exploring:

1. Review Your Sum Insured

The building sum insured is the single biggest lever on your premium. If you haven't had a professional building valuation recently, it's worth commissioning one. You may find your sum insured is higher than necessary — or, importantly, that it's actually too low, which carries its own risks at claim time.

2. Compare Multiple Insurers

Insurers price risk differently, and the variance between quotes for the same property can be significant. Using a comparison platform like CoverClub makes it easy to see multiple options side by side without hours of form-filling.

3. Consider a Higher Excess

This quote carries a $5,000 excess for both building and contents — already on the higher end. If you're comfortable absorbing a larger out-of-pocket cost in the event of a claim, increasing your excess further can reduce your annual premium. Just ensure the saving is meaningful relative to the additional risk you're taking on.

4. Bundle Building and Contents

Home and contents policies are often priced more competitively when bundled together with the same insurer. This quote already combines both, which is a good starting point — but it's worth confirming you're getting a multi-policy discount and that it's actually the best combined deal available.

---

Ready to Find a Better Rate?

Whether you're renewing your policy or shopping for the first time, comparing quotes is the most effective way to ensure you're not overpaying. CoverClub makes it simple to benchmark your premium against real data from your suburb and find competitive options tailored to your property. Get a quote today and see what Maudsland homeowners are actually paying.