McGraths Hill is a quiet residential suburb in the Hawkesbury region of New South Wales, sitting roughly 55 kilometres north-west of the Sydney CBD. It's a popular choice for families seeking space and a semi-rural lifestyle without straying too far from urban amenities. For owners of a free standing home in this area, understanding what drives home insurance costs — and whether a quoted premium is reasonable — can make a meaningful difference to the household budget.

This article breaks down a recent Home and Contents insurance quote for a five-bedroom, two-bathroom free standing home in McGraths Hill (postcode 2756), and puts it in context against local, state, and national benchmarks.

---

Is This Quote Fair?

The quoted annual premium for this property is $4,770 per year (or $450 per month), covering a building sum insured of $1,153,000 and contents valued at $50,000, each with a $1,000 excess.

Based on CoverClub's pricing data, this quote is rated Expensive — above average for the area. Here's what that means in practice:

- The suburb median for McGraths Hill is $3,088/yr, meaning this quote is roughly 54% above the local midpoint.

- The suburb average sits at $5,579/yr, so while this quote falls below the local average, it still clears the median by a significant margin.

- The 75th percentile for the suburb is $3,484/yr — this quote exceeds even that upper band.

In short, while you could argue this premium isn't the most expensive quote in the suburb, the majority of comparable properties in McGraths Hill are being insured for considerably less. That's worth paying attention to.

It's also important to note that the sample size for this suburb is relatively small (13 quotes), so the averages may shift as more data comes in. You can explore the latest figures on the McGraths Hill insurance stats page.

---

How McGraths Hill Compares

Putting this quote in a broader context helps clarify where McGraths Hill sits in the insurance landscape.

| Benchmark | Average Premium | Median Premium |

|---|---|---|

| McGraths Hill (suburb) | $5,579/yr | $3,088/yr |

| New South Wales (state) | $9,528/yr | $3,770/yr |

| Australia (national) | $5,347/yr | $2,764/yr |

A few things stand out here:

- NSW averages are high — the state average of $9,528/yr reflects the significant weight of high-risk and high-value properties across the state, particularly in flood-prone, bushfire-affected, and coastal areas. The median of $3,770/yr is a more grounded figure for typical NSW homeowners.

- McGraths Hill's median ($3,088) is below both the NSW and national medians, suggesting that, broadly speaking, the suburb is not considered a particularly high-risk postcode by insurers.

- The national median of $2,764/yr is the lowest benchmark here, reflecting that many parts of Australia — particularly inland and lower-risk regions — attract more competitive premiums.

For more detail on how NSW compares to the rest of the country, visit the NSW insurance statistics page or the national home insurance stats overview.

---

Property Features That Affect Your Premium

Several characteristics of this particular property are likely influencing the quoted premium — both upward and downward.

Factors that may be pushing the premium higher

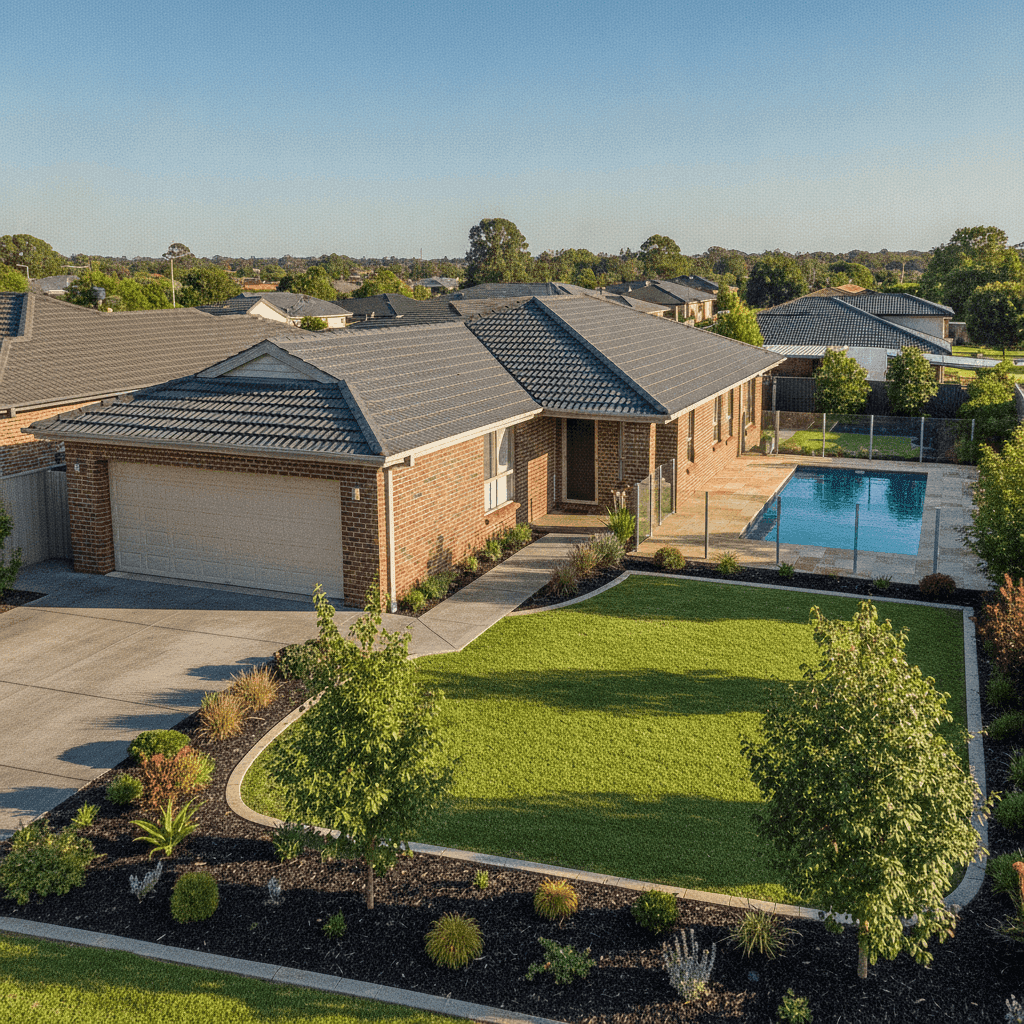

- Building size (305 sqm): This is a large home. A higher sum insured of $1,153,000 directly increases the cost to rebuild, which is one of the most significant drivers of premium cost. Larger homes simply cost more to cover.

- Swimming pool: The presence of a pool adds liability exposure and can increase the overall contents and property risk profile in the eyes of insurers.

- Ducted climate control: Ducted systems are expensive to repair or replace and are factored into the building sum insured, contributing to a higher rebuild cost.

- Construction year (1985): Homes built in the mid-1980s may have older plumbing, electrical systems, or roofing materials that increase the likelihood of a claim. Insurers often apply age-related loading to properties of this vintage.

Factors that may be moderating the premium

- Brick veneer construction: Brick veneer is generally viewed favourably by insurers — it's more fire-resistant than timber weatherboard and structurally sound, which can help keep premiums in check.

- Tiled roof: Terracotta or concrete tiles are durable and perform well in most weather conditions, which insurers tend to reward with more competitive pricing compared to older metal or fibrous cement roofing.

- Slab foundation: Concrete slab foundations are considered low-risk for subsidence and movement, particularly in stable soil areas.

- No cyclone risk: McGraths Hill is not in a designated cyclone risk zone, which removes a significant premium loading that affects properties in northern Queensland and parts of WA.

- Standard fittings: Standard-quality internal fittings (rather than high-end or custom finishes) keep the contents and building replacement cost more predictable and lower than luxury-fitted homes.

---

Tips for Homeowners in McGraths Hill

If you're looking to get better value on your home insurance, here are four practical steps worth considering:

- Review your sum insured carefully. A building sum insured of $1,153,000 for a 305 sqm home works out to roughly $3,780 per square metre — on the higher end of typical rebuild costs in regional NSW. Use an independent building cost calculator to verify this figure is accurate rather than over-inflated, as over-insuring directly increases your premium.

- Shop around and compare quotes. The gap between the suburb's 25th percentile ($2,853/yr) and 75th percentile ($3,484/yr) shows there's meaningful variation in what insurers charge for similar properties in McGraths Hill. Getting multiple quotes through a comparison platform like CoverClub takes minutes and could save hundreds of dollars annually.

- Consider a higher excess. Both the building and contents excesses on this policy are set at $1,000. Opting for a higher voluntary excess — say $2,000 — can reduce your annual premium noticeably, particularly if you have a good claims history and are comfortable absorbing a slightly larger out-of-pocket cost in the event of a claim.

- Bundle strategically, but verify the savings. Many insurers offer discounts for combining home and contents cover under a single policy. This quote already bundles both, which is a sensible approach — just make sure the contents sum insured of $50,000 accurately reflects the value of your belongings. Under-insuring contents is a common mistake that can leave you significantly out of pocket after a major loss.

---

Ready to Find a Better Deal?

Whether you're renewing your policy or shopping for the first time, comparing quotes is the single most effective way to avoid overpaying. CoverClub makes it easy to see what multiple insurers would charge for your specific property — in minutes, with no obligation.

Get a home insurance quote for your McGraths Hill property →