If you own a free standing home in McLeans Ridges, NSW 2480, you've likely wondered whether you're paying a fair price for home insurance — or whether there's room to save. This article breaks down a real home and contents insurance quote for a four-bedroom property in the area, compares it against state and national benchmarks, and offers practical tips to help you get the best value cover.

---

Is This Quote Fair?

The quote we're analysing comes in at $1,893 per year (or $193/month) for combined home and contents cover, with a building sum insured of $1,102,000 and contents valued at $50,000. The building excess is $4,000 and the contents excess is $1,000.

Our price rating for this quote is CHEAP — below average — which is excellent news for the homeowner. To put that in perspective:

- The NSW state average premium sits at $9,528/year, and the median is $3,770/year

- The national average is $5,347/year, with a national median of $2,764/year

- The Ballina LGA average — which covers McLeans Ridges — is a striking $23,241/year

At $1,893/year, this quote is less than half the national median and a fraction of what many Ballina LGA homeowners are paying. That's a genuinely competitive outcome, and one worth taking seriously when renewal time rolls around.

It's worth noting that excess levels play a role here. A $4,000 building excess is on the higher side, which typically reduces the annual premium. Homeowners should weigh up whether the lower ongoing cost justifies a larger out-of-pocket expense in the event of a claim.

---

How McLeans Ridges Compares

McLeans Ridges is a semi-rural locality in the Ballina LGA, situated in the Northern Rivers region of NSW. While it's a picturesque and relatively quiet area, the broader Ballina LGA carries some of the highest average home insurance premiums in the country — largely driven by flood risk, storm exposure, and the region's history of significant weather events, including the devastating 2022 floods.

There is currently no suburb-level pricing data available specifically for McLeans Ridges, so we're drawing on NSW state-wide statistics and national benchmarks for context. You can also explore McLeans Ridges-specific insurance data as more quotes come through for the area.

Here's a quick snapshot of how this quote stacks up:

| Benchmark | Annual Premium |

|---|---|

| This quote | $1,893 |

| National median | $2,764 |

| National average | $5,347 |

| NSW median | $3,770 |

| NSW average | $9,528 |

| Ballina LGA average | $23,241 |

The gap between this quote and the Ballina LGA average is remarkable. While individual circumstances vary widely, it highlights just how much premiums can differ based on the specific insurer, property characteristics, and risk profile — even within the same LGA.

---

Property Features That Affect Your Premium

Several characteristics of this property likely contribute to its competitive premium. Let's unpack the key ones:

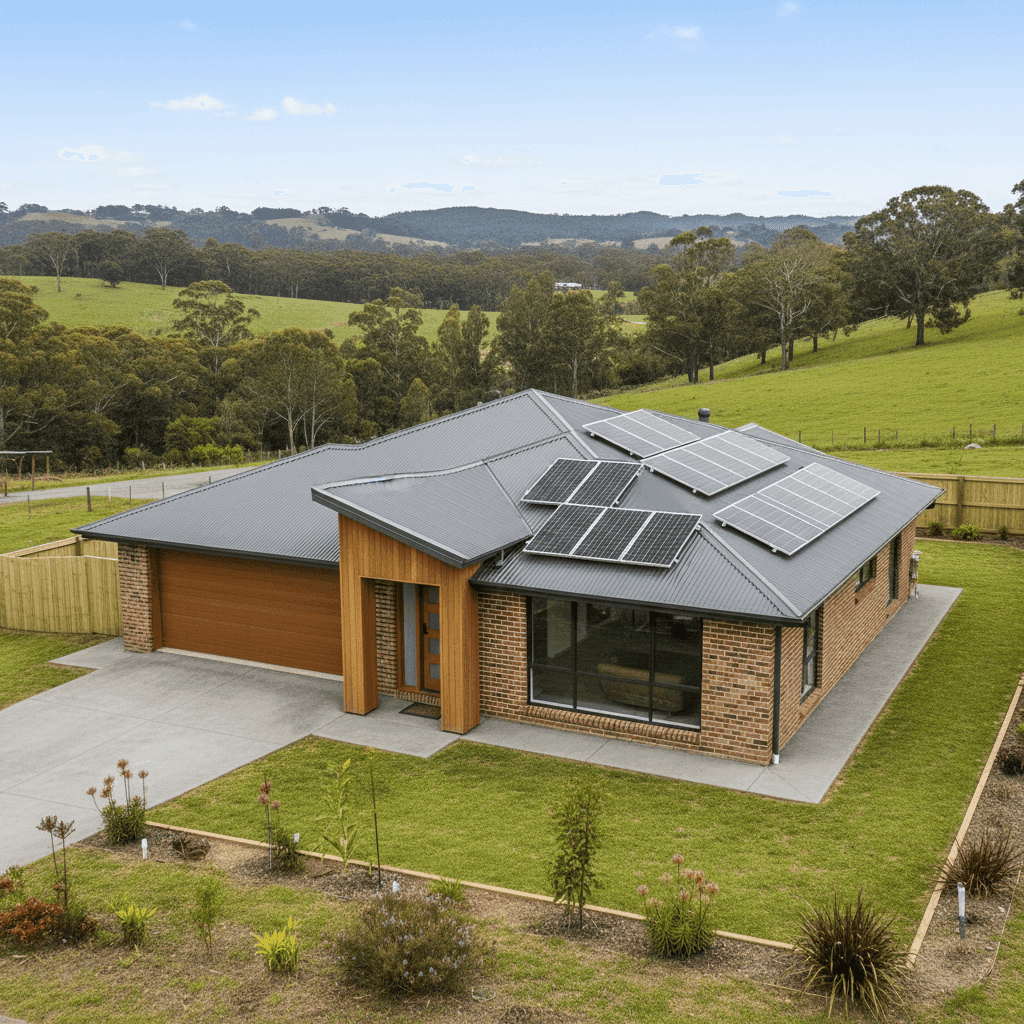

Construction year (2022): A newly built home is a significant advantage when it comes to insurance pricing. Modern builds must comply with current Australian Standards and the National Construction Code, meaning they're generally more resilient to weather events, fire, and structural issues. Insurers reward this with lower risk assessments.

Brick veneer walls and Colorbond roof: Brick veneer is one of the most insurer-friendly wall materials available — it's durable, fire-resistant, and widely understood by underwriters. Paired with a steel Colorbond roof, which handles wind and rain exceptionally well, this combination is considered low-risk by most insurers.

Slab foundation: A concrete slab foundation is structurally sound and less susceptible to movement or moisture ingress compared to older stumped or pier-and-beam homes. This reduces the likelihood of costly structural claims.

Not in a cyclone risk area: Properties outside designated cyclone zones avoid the significant premium loading that applies in northern Queensland and parts of WA. For a Northern Rivers property, this is a meaningful saving.

Solar panels and ducted climate control: These are listed as inclusions under the building sum insured. Solar panels in particular can be a source of claims (hail, fire, storm damage), so it's important they're explicitly covered. Confirming their inclusion in your policy schedule is a smart move.

Slightly elevated (less than 1m): The property is noted as elevated by less than one metre. In a region with known flood history, even a modest elevation above natural ground level can make a difference to flood risk assessments — though homeowners should always check whether flood cover is explicitly included in their policy.

Vinyl flooring and standard fittings: These contribute to a more modest contents and building replacement cost relative to properties with premium finishes, which helps keep the sum insured — and therefore the premium — reasonable.

---

Tips for Homeowners in McLeans Ridges

1. Confirm flood cover is included Given the Northern Rivers region's exposure to flooding — most recently and severely in 2022 — it's critical to verify that your policy explicitly includes flood cover, not just storm or rainwater damage. These are legally distinct definitions in Australia, and some policies exclude flood entirely or charge a significant additional premium for it.

2. Review your sum insured annually With a building sum insured of $1,102,000 on a 214 sqm home built in 2022, the rebuild cost estimate appears reasonable — but construction costs have risen sharply in recent years. Use a building cost calculator or speak with a quantity surveyor to ensure you're not underinsured, particularly as labour and materials costs continue to fluctuate.

3. Reassess your excess strategy The $4,000 building excess is high. While it's helping keep the premium down, it means you'd need to cover the first $4,000 of any building claim yourself. Consider whether you'd be comfortable with that outlay in the event of storm damage or a burst pipe, and compare quotes with a lower excess to find the right balance.

4. Compare at renewal — don't auto-renew The insurance market in the Northern Rivers is volatile. Premiums can shift significantly year to year as insurers update their risk models for the region. Rather than accepting your renewal offer, use a comparison service like CoverClub to benchmark your premium each year and ensure you're still getting a competitive deal.

---

Ready to Compare Your Own Quote?

Whether you're a first-time buyer or a long-term McLeans Ridges resident, it pays to shop around. Home insurance premiums in the Ballina LGA can vary enormously between providers, and the difference between the cheapest and most expensive quotes can run into thousands of dollars annually.

Get a home insurance quote at CoverClub and see how your current premium stacks up against real market data — in minutes, for free.