If you own a free standing home in Meadows, SA 5201, you're probably curious about what a fair home insurance premium looks like — and whether the quote sitting in your inbox is worth accepting. This article breaks down a real home and contents insurance quote for a three-bedroom brick veneer property in Meadows, compares it against local, state, and national benchmarks, and offers practical tips to help you get the best value cover.

---

Is This Quote Fair?

The annual premium for this property came in at $1,339 per year (or roughly $128 per month), covering both building (sum insured: $453,000) and contents ($50,000), each with a $1,000 excess.

Our independent price rating for this quote is FAIR — Around Average.

That might sound underwhelming, but in the context of the broader insurance market, "around average" is actually a reasonable outcome. It means the premium isn't suspiciously cheap (which can signal inadequate cover) nor is it inflated well beyond what comparable properties attract. For a 1985-built home on stumps with solar panels and ducted climate control, insurers have several risk factors to price in — and this quote appears to reflect those without significant loading.

That said, "fair" doesn't mean you can't do better. It simply means this quote is a reasonable starting point for comparison.

---

How Meadows Compares

Understanding where your premium sits relative to others is one of the most useful tools a homeowner has. Here's how this $1,339 quote stacks up:

| Benchmark | Premium |

|---|---|

| This quote | $1,339/yr |

| Meadows suburb average | $1,885/yr |

| Meadows suburb median | $1,854/yr |

| Meadows 25th percentile | $1,154/yr |

| Meadows 75th percentile | $2,356/yr |

| LGA (Onkaparinga) average | $1,431/yr |

| SA state average | $2,433/yr |

| SA state median | $1,679/yr |

| National average | $5,347/yr |

| National median | $2,764/yr |

Based on suburb-level data for Meadows SA 5201, this quote sits below both the suburb average ($1,885) and median ($1,854), placing it comfortably in the lower half of the local pricing range. It's also notably below the SA state average of $2,433, and well under the national average of $5,347 — though that national figure is heavily influenced by high-risk regions such as Far North Queensland and flood-prone areas of NSW.

The Onkaparinga LGA average of $1,431 is the closest comparable benchmark, and this quote comes in $92 below that — a modest but meaningful saving. All up, this is a quote that performs well against its peers, even if there's still room to explore whether a lower premium is achievable without sacrificing cover quality.

---

Property Features That Affect Your Premium

Insurers don't price every home the same way — the physical characteristics of a property play a significant role in determining risk and, ultimately, cost. Here's how this home's features factor in:

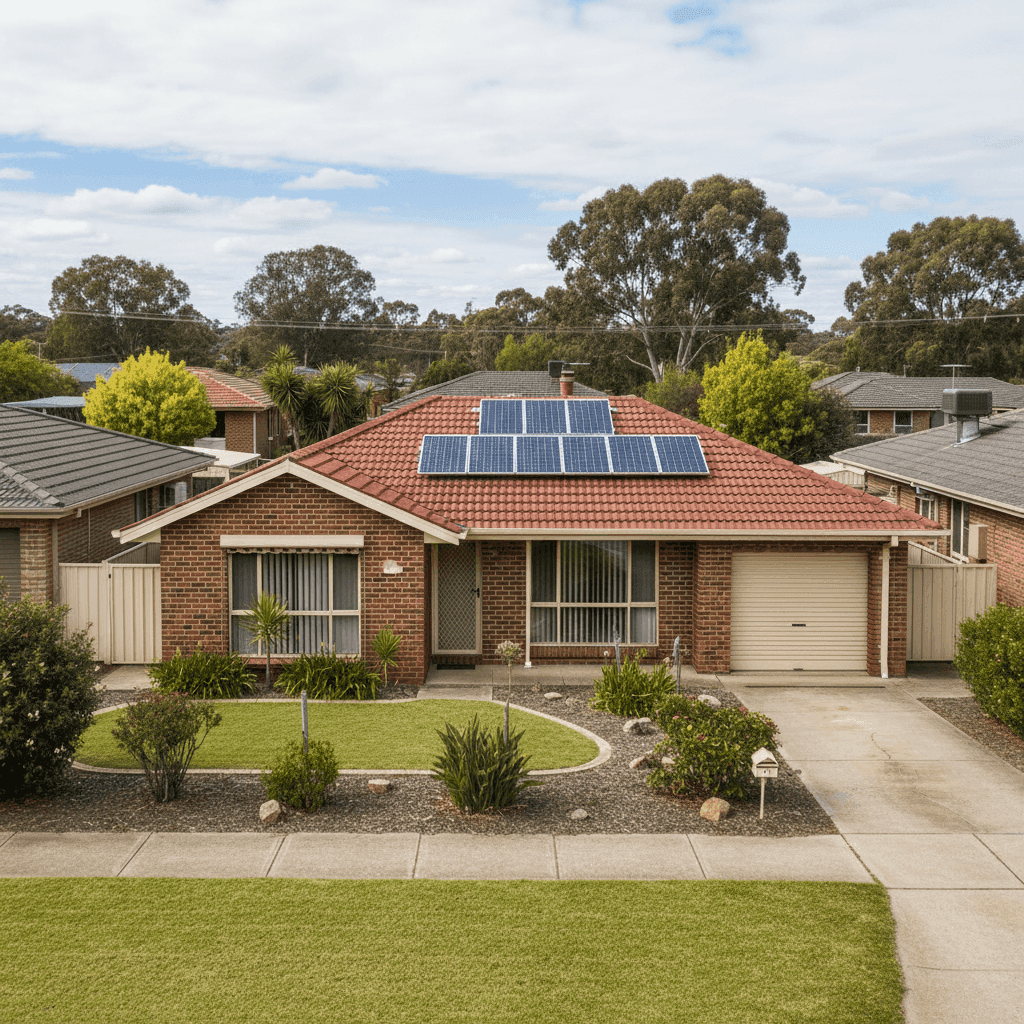

Brick Veneer Walls & Tiled Roof Brick veneer is generally viewed favourably by insurers. It's durable, fire-resistant, and widely understood by assessors. Combined with a tiled roof, this construction profile is considered mid-range in terms of risk — more resilient than timber weatherboard, though not quite as robust as full double-brick. Both materials are well-suited to South Australia's climate.

Stump Foundation & Timber/Laminate Flooring Homes on stumps introduce a slightly different risk profile compared to slab-on-ground construction. Subfloor access can be a maintenance consideration, and timber flooring — while attractive — can be vulnerable to moisture ingress or pest damage over time. Insurers may factor this in, particularly for a home built in 1985 when construction standards differed from today.

Construction Year: 1985 At around 40 years old, this home predates some modern building codes. Older homes can carry higher replacement costs due to non-standard materials or the need to bring structures up to current standards during a rebuild. The $453,000 building sum insured reflects this consideration and appears appropriate for a 214 sqm home in regional South Australia.

Solar Panels Solar panels are now a standard feature on many Australian homes, but they do add to the insured value of the property. Most insurers include panels as part of the building cover, so it's worth confirming this is the case in your policy — particularly given the cost of replacement systems.

Ducted Climate Control Ducted systems are a fixed building asset and typically covered under building insurance rather than contents. At replacement costs often exceeding $10,000–$15,000, having adequate building sum insured is important for homeowners with this feature.

No Pool, No Cyclone Risk Zone The absence of a swimming pool removes a common liability and maintenance risk factor. Meadows is also outside designated cyclone risk areas, which keeps the premium profile lower than properties in northern Australia.

---

Tips for Homeowners in Meadows

1. Review your building sum insured regularly Construction costs have risen sharply in recent years. A sum insured set several years ago may no longer reflect the true cost of rebuilding your home — especially a 214 sqm brick veneer property with ducted climate control and solar. Underinsurance is one of the most common and costly mistakes Australian homeowners make. Consider using a building cost calculator or speaking with a quantity surveyor to validate your figure.

2. Compare at least three quotes before renewing Insurance loyalty rarely pays off in Australia. Premiums can vary significantly between providers for identical cover, and the market in Meadows — with a 25th-to-75th percentile range of $1,154 to $2,356 — shows just how wide that spread can be. Use CoverClub to compare quotes and see whether you can improve on your current rate.

3. Check your solar panel and ducted system coverage Confirm with your insurer exactly how solar panels and ducted climate control are treated under your policy. Are they included in the building sum insured? Are there any exclusions for mechanical breakdown or storm damage to panels? These are worth clarifying in writing before you need to make a claim.

4. Consider your excess carefully This quote carries a $1,000 excess on both building and contents. Opting for a higher excess — say $2,000 — can reduce your annual premium, but only makes sense if you have the financial buffer to cover it in the event of a claim. Conversely, if cash flow is tight, a lower excess may provide more practical protection even at a slightly higher premium.

---

Ready to Find a Better Deal?

Whether you're happy with this quote or keen to see what else is out there, comparing your options is always worthwhile. CoverClub makes it easy to get home and contents insurance quotes tailored to your property in Meadows. Start your comparison today at CoverClub and see how much you could save — or simply gain the confidence that you're already getting a fair deal.