Menai is a well-established residential suburb in Sydney's Sutherland Shire, known for its leafy streets, family-friendly atmosphere, and solid brick homes built across several decades. If you own a free standing home in this part of southern Sydney, understanding what you should be paying for home and contents insurance — and why — can make a real difference to your household budget.

This article breaks down a real home insurance quote for a four-bedroom, two-bathroom free standing home in Menai (postcode 2234), compares it against local, state, and national benchmarks, and offers practical tips to help you get the best value cover.

---

Is This Quote Fair?

The quote in question comes in at $2,689 per year (or $258 per month) for combined home and contents insurance, covering a building sum insured of $718,000 and contents valued at $50,000. Both the building and contents excess are set at $1,000.

Our price rating for this quote is FAIR — Around Average, and the data backs that up. The suburb average premium for Menai sits at $3,041 per year, while the median is $2,957. At $2,689, this quote lands below both figures, placing it comfortably within the lower half of what Menai homeowners typically pay. It's above the suburb's 25th percentile of $2,465 but well under the 75th percentile of $3,335 — meaning roughly half of comparable quotes in the area cost more.

In short, this is a reasonable premium. It's not a bargain-basement price, but it's also not inflated. For a property of this size, age, and specification, sitting below the local average is a solid outcome.

---

How Menai Compares

To put this quote in proper context, it helps to look beyond the suburb. You can explore the full breakdown on the Menai suburb stats page.

| Benchmark | Annual Premium |

|---|---|

| This quote | $2,689 |

| Menai suburb average | $3,041 |

| Menai suburb median | $2,957 |

| NSW average | $9,528 |

| NSW median | $3,770 |

| National average | $5,347 |

| National median | $2,764 |

The NSW state average of $9,528 looks startling at first glance, but it's heavily skewed by high-risk and high-value properties across the state — particularly flood-prone regions and areas with elevated bushfire exposure. The NSW median of $3,770 is a more representative figure, and this quote sits comfortably beneath it.

Compared to the national average of $5,347, Menai homeowners are generally paying less — a reflection of the suburb's relatively low natural hazard risk profile. The national median of $2,764 is actually slightly above this quote, which again reinforces the "fair" rating.

It's also worth noting that the Sutherland LGA average of $23,423 is an extreme outlier likely driven by a small number of very high-value or high-risk properties, and shouldn't be used as a meaningful comparison point for a typical Menai home.

Note: Suburb comparisons are based on a sample of 16 quotes, so treat these figures as a useful guide rather than a definitive benchmark.

---

Property Features That Affect Your Premium

Every insurer assesses risk differently, but certain property characteristics consistently influence what you'll pay. Here's how the features of this particular home factor in:

Brick Veneer Walls Brick veneer is one of the most common construction types in Sydney's southern suburbs, and insurers generally view it favourably. It offers good fire resistance and structural durability, which can help keep premiums moderate compared to weatherboard or fibre cement properties.

Tiled Roof Terracotta or concrete tiles are considered a low-to-moderate risk roofing material. They're durable, fire-resistant, and widely used in the area. A roof from a 1975-era home may be approaching the age where insurers start to factor in maintenance risk, so keeping it in good condition is worthwhile.

Slab Foundation A concrete slab foundation is standard for homes of this era in the Sutherland Shire. It's generally considered stable and low-risk, though it's worth being aware that slab homes can be more susceptible to certain types of water damage if drainage isn't well managed.

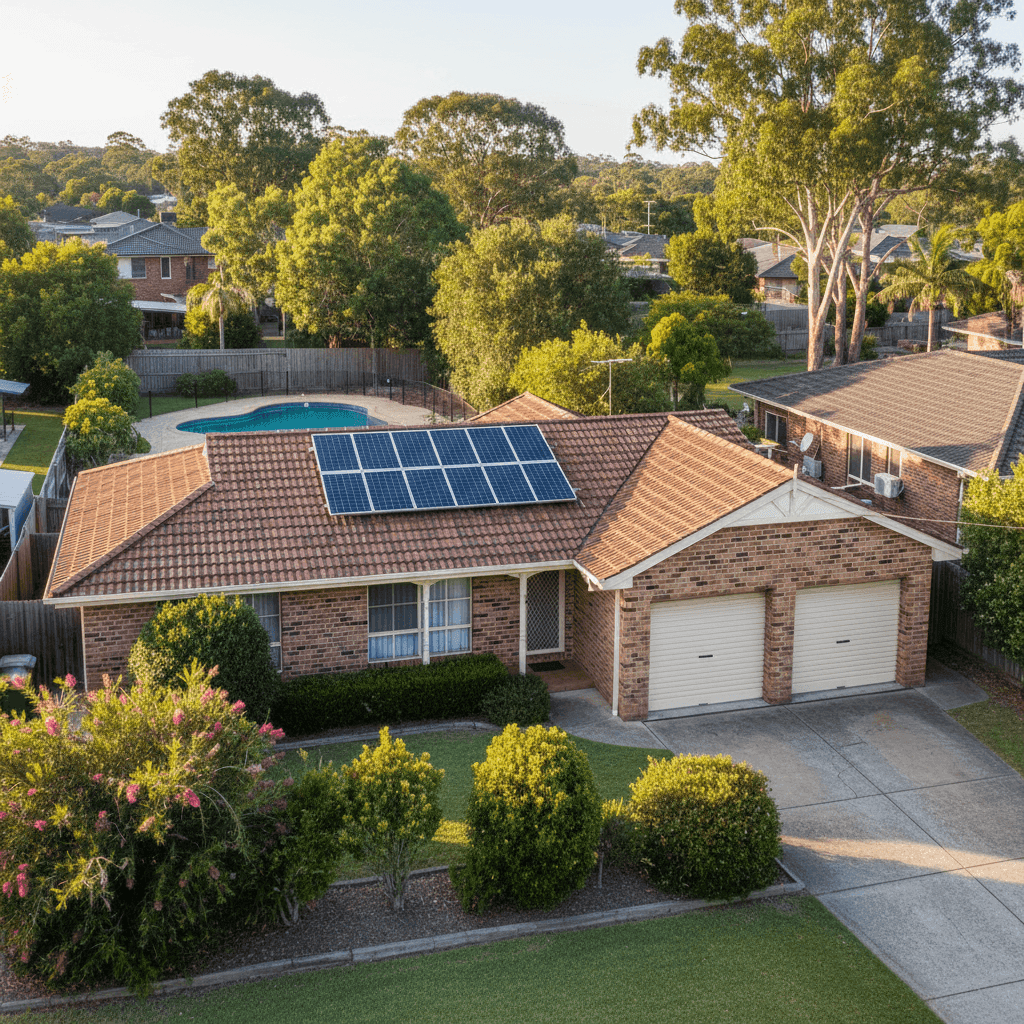

Construction Year: 1975 At roughly 50 years old, this home sits in a bracket where insurers may apply a modest age loading. Older homes can carry higher replacement costs due to the need for period-appropriate materials or compliance upgrades. A building sum insured of $718,000 for a 214 sqm home reflects this reality.

Pool, Solar Panels & Ducted Climate Control These three features each add value — and complexity — to the property. A swimming pool increases liability exposure and can push premiums slightly higher. Solar panels add to the replacement cost of the building and may require specific coverage confirmation with your insurer. Ducted climate control systems are costly to replace and should be explicitly covered under your building policy. It's worth confirming all three are adequately addressed in your policy terms.

Flooring: Tiles Tiled flooring is relatively straightforward from an insurance perspective — it's durable and less susceptible to water damage than carpet or timber. This is a minor positive factor in the overall risk assessment.

---

Tips for Homeowners in Menai

1. Review your building sum insured regularly Construction costs have risen significantly in recent years. A 214 sqm brick veneer home built in 1975 may cost substantially more to rebuild today than it did even three years ago. Underinsurance is a genuine risk — make sure your $718,000 figure reflects current labour and materials costs in the Sydney market. Tools like the Cordell Sum Sure calculator can help you sense-check this figure.

2. Confirm your pool and solar panels are explicitly covered Not all standard home insurance policies automatically extend full cover to in-ground pools or rooftop solar systems. Check your Product Disclosure Statement (PDS) carefully, and ask your insurer directly if you're unsure. Some policies treat solar panels as a separate item requiring endorsement.

3. Consider your excess strategically Both the building and contents excess on this policy are set at $1,000. Opting for a higher voluntary excess (say, $2,000 or $2,500) can reduce your annual premium, sometimes meaningfully. This strategy works best if you have the financial buffer to cover a larger out-of-pocket cost in the event of a claim.

4. Shop around at renewal time Even a "fair" quote can be beaten. Insurers regularly reprice their books, and loyalty doesn't always pay. Comparing quotes annually — especially as your property ages or its features change — is one of the simplest ways to avoid overpaying. Use a comparison platform to see multiple options side by side without the legwork.

---

Compare Your Options with CoverClub

Whether you're reviewing your existing policy or shopping for the first time, it pays to see what the market has to offer. CoverClub makes it easy to compare home and contents insurance quotes for properties across Menai and the wider Sutherland Shire. Get a quote today and find out if you could be paying less — or getting more cover for what you already spend.