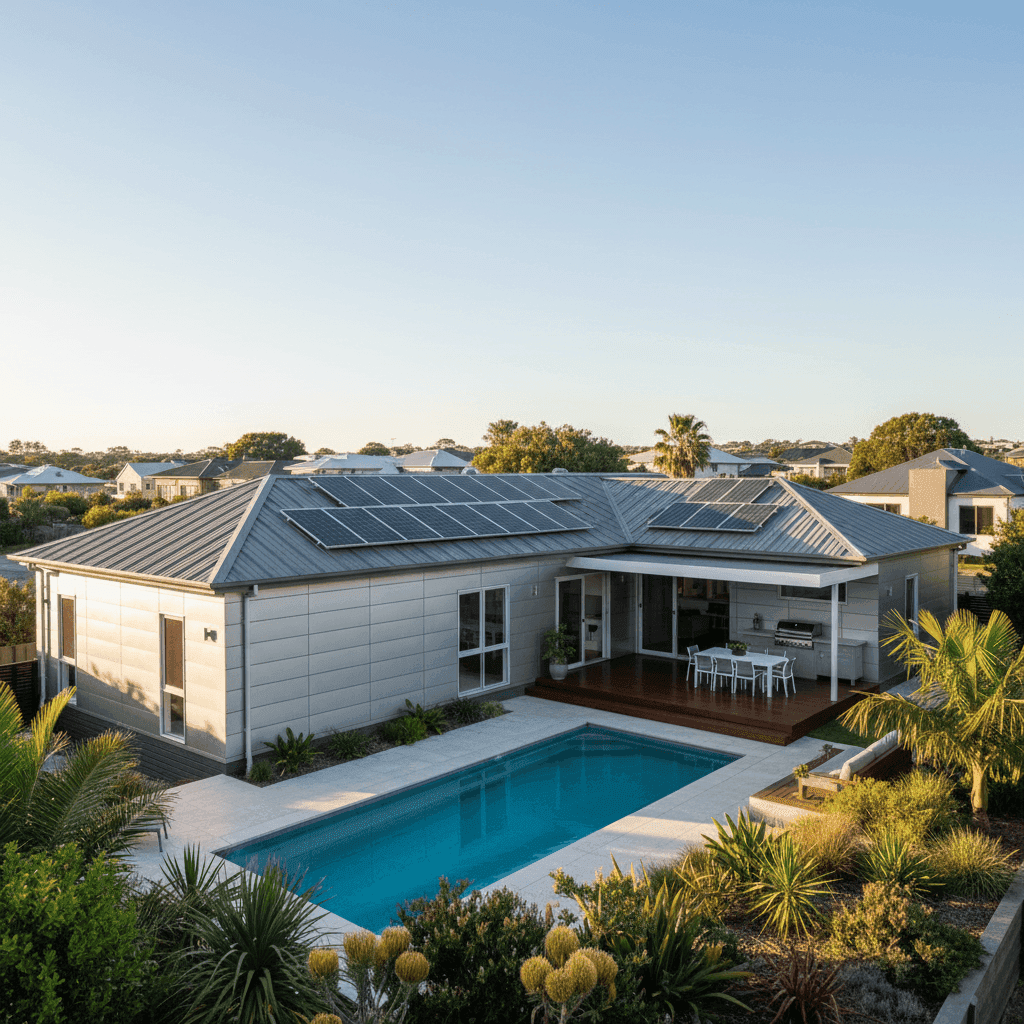

Merewether is one of Newcastle's most sought-after coastal suburbs — a place where relaxed beach culture meets well-established residential streets. For owners of a free standing home in this area, protecting a significant asset with the right home and contents insurance is essential. This article breaks down a recent home and contents insurance quote for a four-bedroom, two-bathroom property in Merewether (NSW 2291), examines how it stacks up against local and national benchmarks, and offers practical guidance for homeowners looking to get the best value from their cover.

---

Is This Quote Fair?

The quoted annual premium for this property came in at $7,741 per year (or $742 per month), covering both building and contents. The building is insured for $1,700,000 and contents for $296,000, with a $2,000 excess applying to both.

Our price rating for this quote is FAIR — Around Average.

That assessment holds up when you look at the numbers in context. The suburb average premium for Merewether sits at $7,105 per year, meaning this quote is only about 9% above the local average — a modest difference given the property's size (235 sqm), the inclusion of a pool, solar panels, and ducted climate control, all of which add to the insured value and risk profile.

It's worth noting that the suburb median premium is considerably lower at $5,034 per year, which reflects the wide spread of premiums in the area. This quote lands between the suburb's 75th percentile ($11,981/yr) and the median, suggesting it's on the higher side for the suburb but far from the most expensive policies being written here. With a sample of 21 quotes in Merewether's suburb data, there's a meaningful range of outcomes depending on property characteristics and insurer choice.

---

How Merewether Compares

Understanding where your premium sits relative to broader benchmarks helps put things in perspective.

| Benchmark | Average Premium | Median Premium |

|---|---|---|

| Merewether (2291) | $7,105/yr | $5,034/yr |

| Newcastle LGA | $3,835/yr | — |

| New South Wales | $9,528/yr | $3,770/yr |

| National | $5,347/yr | $2,764/yr |

A few things stand out here. First, the NSW state average of $9,528 per year is actually higher than this quote — so relative to the broader state, this premium looks competitive. NSW tends to attract higher premiums due to a combination of storm exposure, bushfire risk in many regions, and elevated property values, particularly in coastal areas.

Second, the national average of $5,347 per year is notably lower, but that figure is pulled down by lower-cost regions across regional and rural Australia where property values and risk profiles differ significantly from a coastal Newcastle suburb.

The Newcastle LGA average of $3,835 per year is considerably lower than the Merewether suburb average — a reminder that Merewether's coastal location and higher property values push premiums above the broader LGA norm. Beachside suburbs typically carry greater exposure to wind, salt air corrosion, and storm surge risk, all of which factor into insurer pricing.

---

Property Features That Affect Your Premium

Several characteristics of this particular property have a meaningful influence on the premium calculated.

Aluminium cladding and Colorbond roof — Aluminium external walls are generally considered a moderate-risk construction material; they're durable but can be more costly to repair or replace than brick veneer. The steel Colorbond roof, on the other hand, is widely regarded as a resilient and low-maintenance option that many insurers view favourably in storm-prone coastal areas.

Slab foundation, slightly elevated — The property sits on a concrete slab with an elevation of less than one metre. While not a full raised foundation, this modest elevation can offer some protection against minor surface water ingress — a relevant consideration given Merewether's proximity to the coast and its exposure to east coast low weather events.

Pool, solar panels, and ducted climate control — These three features all contribute to a higher sum insured and, by extension, a higher premium. A pool adds liability exposure and replacement cost. Solar panel systems (particularly larger rooftop arrays) are increasingly common in insurance calculations. Ducted climate control represents a significant fixed asset within the home that must be covered under the building sum insured.

High building sum insured ($1,700,000) — For a 235 sqm home, this reflects both the quality of the property and the elevated rebuilding costs in coastal NSW. Construction costs have risen sharply in recent years, and insurers are pricing accordingly. Ensuring your sum insured accurately reflects current rebuild costs — not market value — is critical to avoiding underinsurance.

Tile flooring and standard fittings — Tiled floors are durable and generally straightforward to replace, which can have a modest moderating effect on contents and building repair costs compared to hardwood or high-end finishes.

---

Tips for Homeowners in Merewether

1. Review your sum insured annually Building costs in coastal NSW have increased significantly. Use a building cost calculator or speak with a quantity surveyor to confirm your $1,700,000 sum insured still reflects the true cost to rebuild — not just the market value of the land and home combined.

2. Consider your excess strategically Both the building and contents excess on this policy sit at $2,000. Opting for a higher excess (say, $2,500 or $3,000) can reduce your annual premium meaningfully. If you have sufficient savings to cover a larger out-of-pocket cost in the event of a claim, this trade-off can make financial sense.

3. Maintain your pool and solar system documentation Insurers may require evidence of regular servicing for pools and solar panel systems when processing claims. Keep records of inspections, maintenance, and installation certificates — this can smooth the claims process considerably.

4. Compare quotes at renewal time A "fair" rating means this quote is competitive, but it doesn't mean it's the lowest available for equivalent cover. Insurers adjust their pricing models regularly, and the gap between the cheapest and most expensive quotes in Merewether is substantial (from $3,231 at the 25th percentile to $11,981 at the 75th percentile). Shopping around at renewal could yield real savings without sacrificing cover quality.

---

Ready to Compare?

Whether you're renewing your existing policy or insuring a new property, comparing quotes is one of the simplest ways to ensure you're not overpaying. Get a home insurance quote at CoverClub and see how your premium stacks up against real data from your suburb, your state, and across Australia.