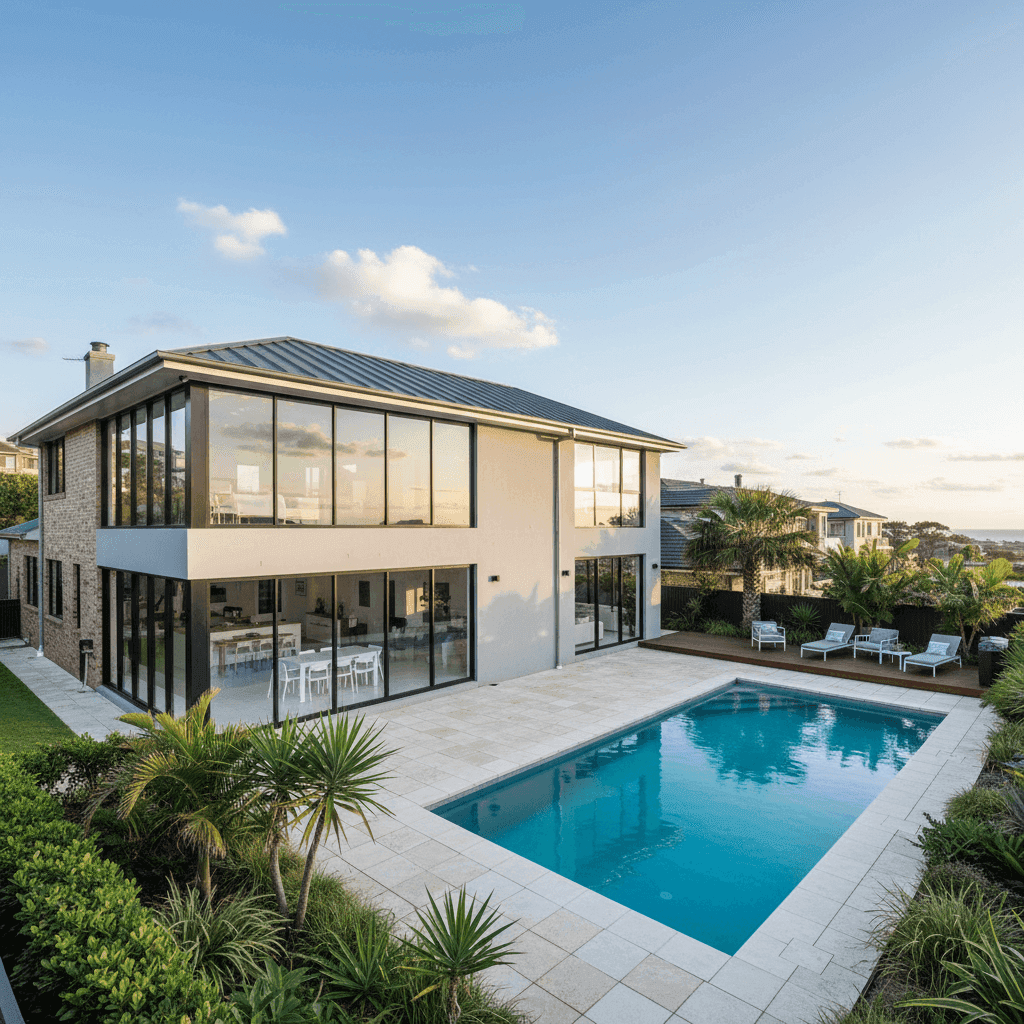

Merewether is one of Newcastle's most desirable coastal suburbs — a leafy, relaxed neighbourhood known for its ocean baths, surf beach, and a strong mix of established and newer family homes. For owners of a substantial free-standing home in this area, protecting that investment with the right home and contents insurance is essential. This article breaks down a real insurance quote for a five-bedroom, three-bathroom property in Merewether, compares it against local and national benchmarks, and offers practical guidance for getting the best value cover.

---

Is This Quote Fair?

The quoted annual premium for this property is $10,303 per year (or $981/month), covering both building (sum insured: $1,486,000) and contents ($249,000), each with a $1,000 excess.

Our price rating for this quote is FAIR — Around Average, and the data backs that up. While $10,303 sits noticeably above the suburb average of $7,105 and well above the national average of $5,347, it's important to look at the full picture. This is a large, high-value property — 286 sqm of living space, above-average fittings, a pool, and ducted climate control all contribute meaningfully to the sum insured and, by extension, the premium.

When you factor in the building replacement value of nearly $1.5 million and contents cover approaching $250,000, the effective premium rate as a percentage of total cover is actually quite reasonable. A "fair" rating here reflects that the price is broadly in line with what comparable high-value homes in the area attract, rather than being a bargain or an overcharge.

---

How Merewether Compares

Understanding where a quote sits relative to the broader market is one of the most useful tools a homeowner has. Here's how this premium stacks up across different reference points:

| Benchmark | Premium |

|---|---|

| This Quote | $10,303/yr |

| Merewether Suburb Average | $7,105/yr |

| Merewether Suburb Median | $5,034/yr |

| Merewether 75th Percentile | $11,981/yr |

| NSW State Average | $9,528/yr |

| NSW State Median | $3,770/yr |

| National Average | $5,347/yr |

| National Median | $2,764/yr |

| Newcastle LGA Average | $3,835/yr |

(Based on 21 quotes sampled for the Merewether suburb.)

At first glance, $10,303 looks high against the suburb median of $5,034 — but medians can be misleading when there's a wide spread of property sizes and values in a suburb. This quote sits just below the suburb's 75th percentile of $11,981, meaning roughly three-quarters of comparable quotes in Merewether come in cheaper, but a meaningful portion are actually more expensive.

Compared to the NSW state average of $9,528, this quote is only modestly above average — a gap of around $775 per year. Given the property's size and value, that gap is easily explained by the above-average sum insured alone.

Explore the full breakdown of home insurance statistics for Merewether (NSW 2291), compare it against all NSW suburbs, or check out national home insurance averages to put your own situation in perspective.

---

Property Features That Affect Your Premium

Several characteristics of this property have a direct bearing on the premium quoted. Understanding these can help you make sense of the cost — and identify any levers you might be able to pull.

Double Brick Construction

Double brick is widely regarded as one of the most durable and fire-resistant external wall materials available. Insurers generally view it favourably, as it reduces the risk of certain types of damage. However, double brick homes can also be more expensive to rebuild per square metre than lightweight timber-frame construction, which can push the building sum insured — and the premium — upward.

Colorbond Steel Roof

Steel roofing is durable, low-maintenance, and performs well in coastal conditions where salt air can degrade other materials. Insurers typically price Colorbond roofs competitively. It's a sensible choice for a coastal suburb like Merewether.

Slab Foundation

A concrete slab foundation is standard for homes of this era and is generally considered low-risk from an insurance perspective, particularly in areas not prone to significant soil movement or flooding.

Swimming Pool

A pool adds to the replacement cost of the property and is included in the building sum insured. Beyond rebuild cost, pools can introduce liability considerations depending on your policy's terms. Make sure your policy clearly covers pool structures and associated equipment.

Ducted Climate Control

Ducted air conditioning systems are expensive to repair or replace and are factored into the building sum insured. At above-average fittings quality, the fit-out of this home — including the climate control system — justifiably contributes to a higher insured value.

Above-Average Fittings Quality

From premium kitchen appliances and stone benchtops to high-end bathroom fixtures, above-average fittings significantly increase the cost to rebuild or restore a home to its original standard. Underinsuring a property with quality fittings is a common and costly mistake.

Building Size: 286 sqm

At 286 sqm, this is a large family home. Rebuild costs scale with floor area, and in a coastal Newcastle suburb, per-square-metre construction costs are not insignificant. Getting an accurate building sum insured is critical — both over- and under-insurance carry real risks.

---

Tips for Homeowners in Merewether

1. Review Your Building Sum Insured Regularly

Construction costs have risen sharply in recent years. A sum insured that was accurate two years ago may no longer reflect the true cost to rebuild your home today. Consider using a professional quantity surveyor or an online building calculator annually to keep your figure current. Underinsurance is one of the most common — and avoidable — problems at claim time.

2. Compare Quotes Before Renewal

Insurers don't always reward loyalty with competitive pricing. The market for a high-value property in Merewether can vary significantly between providers — as the spread between the suburb's 25th percentile ($3,231) and 75th percentile ($11,981) clearly demonstrates. Running a fresh comparison at renewal time takes minutes and could save you hundreds.

3. Consider Your Excess Carefully

Both the building and contents excess on this policy are set at $1,000. Opting for a higher voluntary excess — say, $2,000 or $2,500 — can meaningfully reduce your annual premium. If you have the financial buffer to cover a larger out-of-pocket cost in the event of a claim, this is often a smart trade-off for a low-claims household.

4. Check Your Contents Cover Reflects Reality

With $249,000 in contents cover, this policy accounts for a well-furnished home. But it's worth doing a room-by-room audit periodically. High-value items such as jewellery, artwork, musical instruments, or electronics may need to be separately listed (scheduled) on your policy to be fully covered. Don't assume a general contents limit covers everything automatically.

---

Ready to Compare?

Whether you're renewing your existing policy or insuring a property for the first time, comparing quotes is the single most effective way to ensure you're getting fair value. CoverClub makes it easy to see what insurers are offering for your specific property in Merewether and across NSW. Get a personalised home insurance quote today and see how your premium stacks up.