Nestled in the foothills of the Victorian Alps, Merriang (postcode 3737) is a quiet rural locality in the Wangaratta local government area. If you own a free standing home here, you'll know that insuring a property in regional Victoria comes with its own set of considerations — from ageing construction styles to the unique features that make rural homes both charming and complex to underwrite. This article takes a close look at a real home and contents insurance quote for a 3-bedroom, 2-bathroom property in Merriang and unpacks whether the price stacks up.

---

Is This Quote Fair?

The quote in question comes in at $4,052 per year (or $381/month), covering both building and contents for a property with a building sum insured of $603,000 and contents valued at $50,000. Both the building and contents excess are set at $2,000.

Our price rating for this quote is Expensive — above average for the area.

To put that in perspective: the suburb average premium in Merriang sits at around $2,710/year, and the suburb median is $2,703/year. This quote is roughly 49% above the local average — a meaningful gap that's worth understanding before simply accepting the price.

That said, "expensive" doesn't automatically mean "wrong." Insurers price premiums based on a combination of property-specific risk factors, and several features of this particular home may be pushing the cost upward. We'll explore those shortly.

---

How Merriang Compares

To get a fuller picture, it helps to look at how Merriang sits within the broader insurance landscape. You can explore the full data on the Merriang suburb stats page.

| Benchmark | Annual Premium |

|---|---|

| This quote | $4,052 |

| Merriang suburb average | $2,710 |

| Merriang suburb median | $2,703 |

| Merriang 25th percentile | $2,234 |

| Merriang 75th percentile | $2,704 |

| Wangaratta LGA average | $3,113 |

| VIC state average | $3,000 |

| VIC state median | $2,718 |

| National average | $5,347 |

| National median | $2,764 |

Note: Suburb sample size is 5 quotes, so local figures should be interpreted with some caution.

A few things stand out here. First, this quote exceeds not just the suburb average but also the Victorian state average of $3,000/year — sitting about 35% above it. However, it remains well below the national average of $5,347/year, which is heavily influenced by high-risk coastal and cyclone-prone areas in Queensland and Western Australia.

The Wangaratta LGA average of $3,113/year is also instructive — it shows that properties across the broader region do attract premiums above the state median, likely reflecting the rural location, bushfire risk proximity, and older housing stock common to the area.

---

Property Features That Affect Your Premium

Several characteristics of this property are likely contributing to a higher-than-average premium. Here's what insurers are probably weighing up:

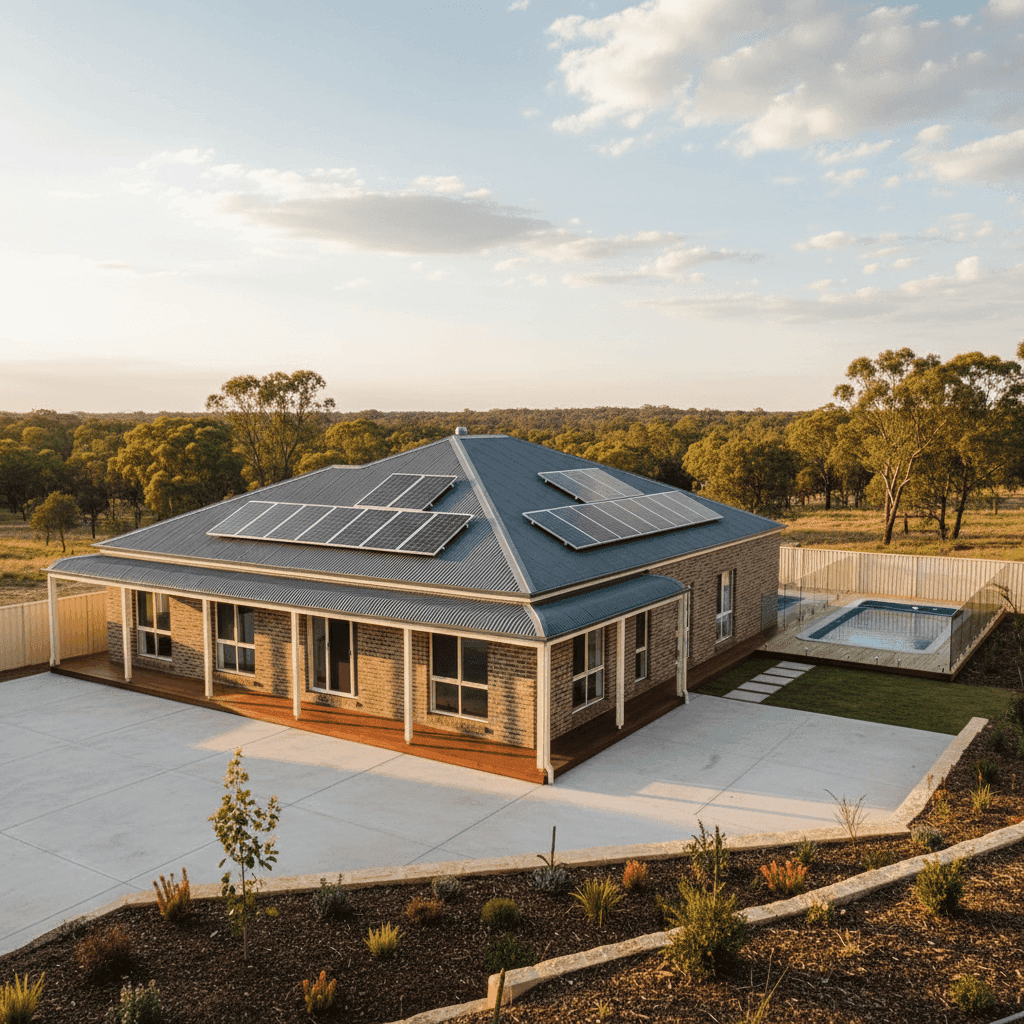

Age of Construction (1960)

Built in 1960, this home is over 60 years old. Older properties often carry higher premiums because ageing electrical wiring, plumbing, and structural elements can increase the likelihood of a claim. Insurers may also apply a loading to reflect the cost of restoring period-appropriate materials if damage occurs.

Foundation: Stumps

Homes on stump foundations are common in regional Victoria, but they can be flagged by insurers as a potential risk — particularly for subsidence, pest damage, and structural movement over time. This foundation type may attract a modest premium loading compared to a concrete slab.

Timber/Laminate Flooring

Timber floors, while beautiful, are more susceptible to water damage and fire than concrete or tile alternatives. This can influence how an insurer calculates risk, especially in a home of this age.

Swimming Pool

A pool adds both value and liability to a property. Insurers factor in the cost of pool-related damage (such as structural failure or storm damage to fencing and equipment) as well as any public liability considerations.

Solar Panels

Solar panels increase the replacement value of a home and can complicate roof repairs after a storm or hail event. While they're a great investment for energy savings, they do add to the insured value and, in turn, the premium.

Ducted Climate Control

Ducted systems are expensive to repair or replace and are often included in the building sum insured. Their presence can nudge premiums slightly higher.

Brick Veneer Walls & Colorbond Roof

On the positive side, brick veneer construction and a steel Colorbond roof are generally viewed favourably by insurers. Colorbond in particular is durable, fire-resistant, and low-maintenance — factors that can help moderate premiums compared to older tile or timber roofing.

---

Tips for Homeowners in Merriang

If you're looking to get better value on your home and contents insurance, here are some practical steps worth considering:

1. Shop Around and Compare Quotes

With only 5 quotes in our local sample, there's meaningful variation in what insurers will offer for a property like this. Use a comparison tool like CoverClub to see multiple quotes side by side — you could find a significantly lower premium for equivalent cover.

2. Review Your Sum Insured

A building sum insured of $603,000 is substantial. Make sure this figure reflects the actual cost to rebuild your home (not its market value), as over-insuring is a common reason premiums run high. A quantity surveyor or online rebuild calculator can help you land on a more accurate figure.

3. Consider a Higher Excess

Both the building and contents excess on this policy are set at $2,000. If you have the financial buffer to absorb a larger out-of-pocket cost in the event of a claim, opting for a higher excess (say, $2,500 or $3,000) can reduce your annual premium noticeably.

4. Maintain Your Property

For older homes especially, insurers reward proactive maintenance. Keeping your electrical system updated, ensuring stumps are in good condition, and maintaining your pool and solar panel systems can reduce the likelihood of a claim — and may improve your risk profile when renewing or switching insurers.

---

Ready to Find a Better Deal?

Whether you're renewing your policy or insuring a property for the first time, it always pays to compare. CoverClub makes it easy to see what multiple insurers would charge for your specific home — so you're never paying more than you need to. Get a quote today and see how much you could save.